Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Fears that the UK could leave the EU in a little over six months without an agreement continues to drag sterling lower. Recall that over the weekend, the UK’s International Trade Minister Fox suggested there was a 60% chance of a no-deal Brexit. A few days earlier BOE Carney said that although it was not the most likely scenario, the risks such a departure were “higher than comfort.” Sterling is lower for a fifth session and is testing the $1.29 area, which corresponds to a 61.8% retracement of sterling’s rally since January 2017 and ignoring the flash crash low from the previous October. The next technical target would be in the $1.2775-$1.2800 area.

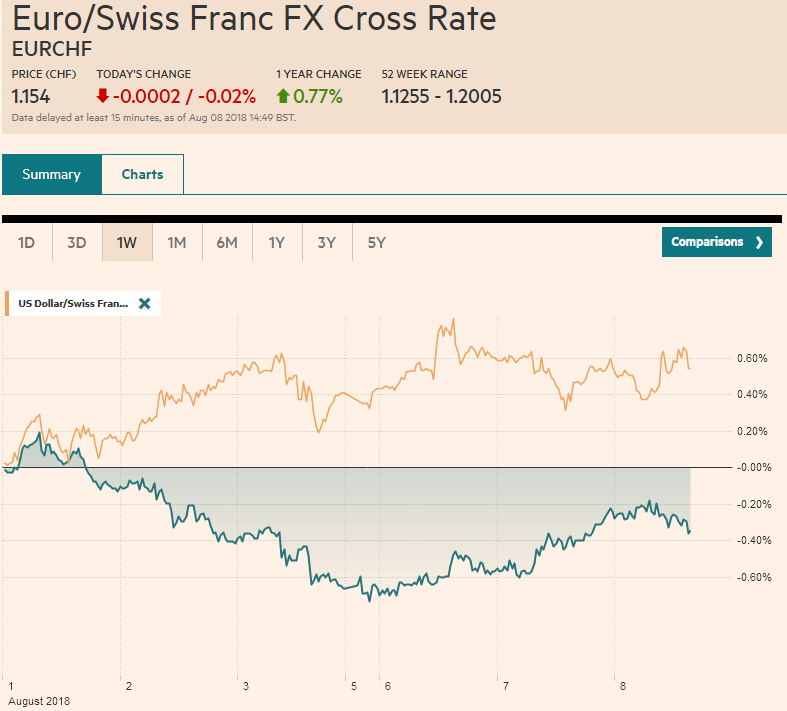

Swiss FrancThe Euro has fallen by 0.02% to 1.154 CHF. |

EUR/CHF and USD/CHF, August 08(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

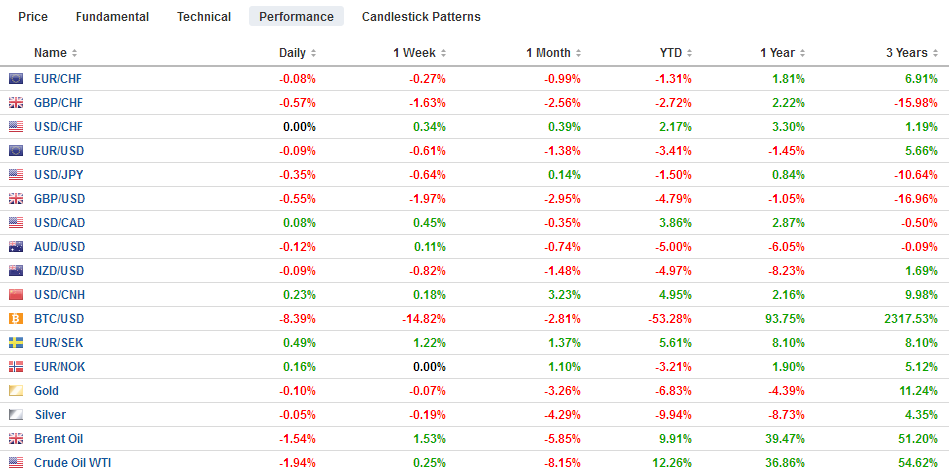

FX RatesSterling is also slumping against the euro, which itself has been able to maintain a toehold above $1.16. Still, the single currency is at its best level against sterling (~GBP0.8980) since last November. It has closed only once above GBP0.9000 since last September, despite several intra-day violations. Sterling is stealing part of the spotlight that is on the Asia-Pacific today. Early in the session, the USD announced that the 25% tariff on $16 bln of Chinese goods, as the second part of the $50 bln targeted goods in retaliation for the intellectual property rights violations, as of August 23. The goods are largely plastics, electronics, and chemicals, but also include motorcycles and railway cars. The yen is the strongest of the major currencies, gaining 0.4% against the dollar. The greenback has been pushed below JPY111 but is holding above last week’s low near JPY110.75. It has not traded below JPY110.60 in over a month. The intraday charts suggest that if the dollar’s low is not in place yet today against the yen, it is nearly so. The euro’s gains seen yesterday were initially extended in Asia to almost $1.1630. It was sold down to $1.1585 by early Europe before finding a bid. The intraday technical indicators do not rule out another run higher. There are several technical targets in the $1.1640-$1.1665 band. Last week, China identified $60 bln of US goods it would slap with a range of tariffs in retaliation if the US goes forward with the threat of the second round of tariffs on $200 bln of Chinese goods. This threat by the US was in response to China’s retaliatory tariffs for initial action on intellectual property rights. The Trump Administration’s actions against China appears to enjoy widespread domestic support. Our concern is about the effectiveness. We are skeptical that it will change China’s behavior or reduce the US trade deficit. In fact, in the first six months of the year, the US trade deficit grew by a little more than 7%, while China’s trade surplus fell by almost 25%. |

FX Performance, August 08 - Click to enlarge |

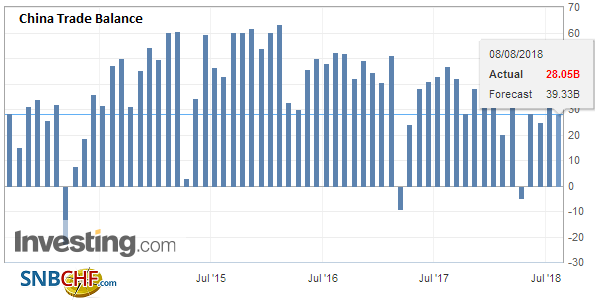

ChinaChina reported its July trade figures today. The surplus fell more than expected. It stood at $28.05 bln down from a revised $41.46 bln in June. The Bloomberg survey found a median forecast for almost $39 bln surplus. Exports rose a strong 12.2% year-over-year, up from 11.2% in June. Imports, on the other hand, surged 27.3%, fueled by energy, and industrial goods like coal and iron ore. Exports to the US were $41.5 bln, according to the Chinese figures and account for 19.3% of their exports. The surplus with the US stood at $28.1 bln, meaning that in July, China trade was roughly in balance with the world ex-US. China’s report suggests Australia, Russia, South Korea and Japan likely experienced strong exports in July. |

China Trade Balance, July 2018(see more posts on China Trade Balance, ) Source: Investing.com - Click to enlarge |

Meanwhile, the PBOC fixed the yuan higher for the second sessions, but the market pushed it back down. Dollar demand is evident near CNY6.80. Three-month SHIBOR continues to ease, falling five basis points and is off 16 bp already this week. Yet the lower rates are not giving the equity market much support. The Shanghai Composite lost 1.3%, unable to build on yesterday’s gains, which was only the second daily advance since July 24. More broadly, the MSCI Asia Pacific Index rose nearly 0.35% and is the first back-to-back gain since July 27.

The benchmark 10-year JGB yield was slightly lower, back below 10 bp, and the generic 10-year yield is slightly higher. The interest today was in the long-end and it sold-off. The 40-year yield edged back above 1.0% for the first time since early this year. The steepening of the JGB curve may be spurring a change in allocation and investment decisions and draw some funds back into Japan. At the same time, newswire report suggesting that the BOJ had contemplated hiking rates twice this year may also have injected a new note of uncertainty. However, what is said to have deterred it is what continues to be the key fact: the economic data does not require it.

The RBNZ’s two-year inflation survey for Q3 rose to 2.04% from 2.01% in Q2. It stood at 2.11% in Q1 and averaged 2.05% last year. It is widely anticipated to remain on hold today, and the announcement is expected shortly after the close of US markets. The New Zealand dollar is in a little more than a 15 tick range on either side of $0.6745.

While Samsung’s $160 bln investment plan may have helped lift Asian shares, disappointing earnings from Novo Nordisk and Glencore may be a drag in Europe, where the Dow Jones Stoxx 600 is lower on the day, giving back almost half of yesterday’s 0.5% gain. European bond yields are mostly lower, and Italy is again leading with a nearly three basis point decline in the 10-year yield. Spain’s bonds are underperforming, despite the weaker than expected June industrial output report. It fell 0.6% instead of easing 0.2% as expected and the May gain was shaved to 0.8% from 0.9%. The seasonally adjusted year-over-year pace slowed to match the 2017 low of 0.5%.

The US and Canadian economic calendars are light. The Richmond Fed President Barkin speaks early in the session. The US is in the middle of the quarterly refunding and today’s $26 bln of 10-year notes for sale will be monitored closely after yesterday’s tepid reception to the three-year note sale. The US oil inventory report may also attract attention. The API estimates that inventories fell overall and at Cushing. The government’s estimate today is expected to report a 2.1 mln barrel draw. Canada reports building permits, which are not a big market mover. The US dollar posted a potential key reversal higher against the Canadian dollar yesterday, and there have been some follow through gains today. Initial resistance is seen near CAD1.3100. It had made a nearly two-month low yesterday near CAD1.2960.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$CNY,$EUR,$JPY,China Trade Balance,EUR/CHF,newslettersent,NZD,USD/CHF