Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has risen by 0.18% to 1.1532 CHF. |

EUR/CHF and USD/CHF, August 07(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is pulling back today after yesterday’s advance. All the major currencies are higher and even the Turkish lira, which plunged nearly 5% yesterday to cap a six-day slide, is trading firmer today ([email protected]). The dollar’s losses are modest and appear corrective in nature. The euro, which spent yesterday’s entire session below $1.16 is knocking on the door again in the European morning. There is scope for some additional gains in the early North American session, but the $1.1615-$1.1625 area may be enough to exhaust it. A close below $1.16 should be seen as a bearish signal. The dollar is trading insides yesterday’s range against the yen, which was inside last Friday’s range. Here too, there is scope for additional albeit limited pressure on the dollar. Support is seen ahead of JPY111.00. Sterling is firm but is running into offers around $1.2970 throughout the European morning. Additional resistance is seen near $1.30. The Australian dollar is the strongest of the majors, gaining 0.65% against the US dollar (~$0.7435) to a five-day high. The $0.7440-$0.7460 area offers the nearby cap. Helped by the biggest rally in Chinese shares in two years (Shanghai Composite +2.75%) and a 0.75% rise in the Topix, the MSCI Asia Pacific Index rose 0.9% and broke a three-day slide. European markets are higher, with the Dow Jones Stoxx 600 up 0.6% near midday, led by energy and material. Real estate is the only sector nursing losses. Oil prices are firmer as are industrial and precious metals. The 10-year JGB yield crept higher and finished a little above 10 bp. Italian bonds, which were under strong pressure last week, continue to recover. The nearly 4 bp decline is the most in Europe, where core yields, like US Treasury yields, are slightly firmer. The US quarterly refunding kicks off today with the $34 bln sale of three-year notes. The Treasury will also sell $70 bln of four-week bills. |

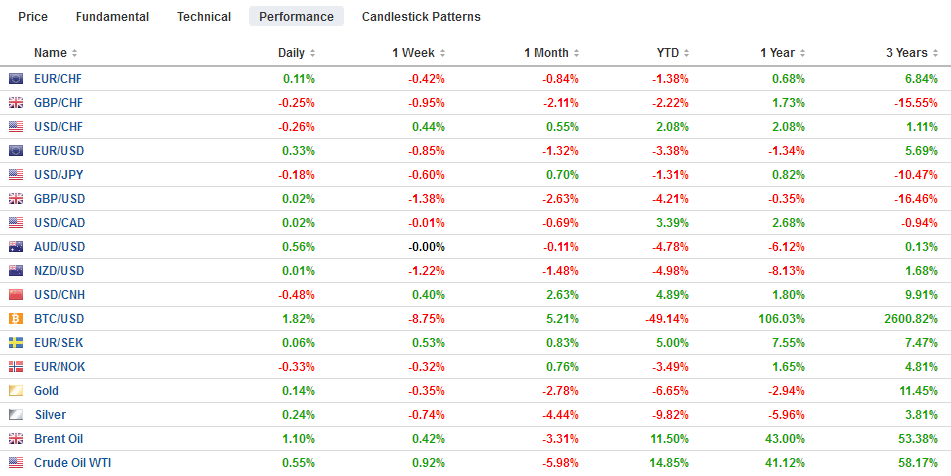

FX Performance, August 07 - Click to enlarge |

The news steam is light, but there few developments to note. First, the Reserve bank of Australia kept rates on hold as widely expected. It shaved this year’s CPI forecast, which may have been seen as dovish in other circumstances, but revised the higher next year’s projection. It also identified the slowing of China as a risk.

Japan

Second, Japan reported two data series. The first is labor cash and real earnings. As we have noted previously, labor cash earnings are rising strongly in Japan. They are up 3.6% in June year-over-year, the most since the late 1990s. In June 2017, they were up 0.4% year-over-year and 0.9% at the end of the year. Adjusted for inflation, real cash earnings are up 2.8% in the past year. It is also the most in around 20 years. Where we depart from many some economists who recognize this trend, is that we do not see as strong of a link with consumption. And to our point, household spending was reported earlier today to have fallen 1.2% in June from a year ago. To be sure, it is less steep of a decline than the 3.9% drop in May, which was the largest fall in two years. In June 2017, household spending was up 2.3% year-over-year.

China

Third, unexpectedly, China reported that the dollar value of its reserves rose by about $5.8 bln in July to $3.118 trillion. In July, the dollar rose almost 3% against the yuan, but the Shanghai Composite rose 1%, The dollar was little changed against most of the other reserve currencies in July. The euro was virtually flat. The yen was off 1% and sterling off 0.6%. US and German bond yields were higher.

Germany

Fourth, Germany followed up yesterday’s whopping 4% drop in June factory orders with a 0.9% drop in industrial output (the market had expected a decline half the size). The May gain was shaved to 2.4% from 2.6%. Separately, but not totally unrelated, Germany reported a slightly larger than expected trade surplus (21.8 bln euros vs. 19.7 bln in May and expectations for around 21 bln). It came as a result of a 1.2% increase in imports and flat exports, which had been expected fall 0.3%). The trade surplus fueled the 26.2 bln current account surplus, which typically swells in June (without fail since 2004).

United States

Even though many observers still insist that the US trade angst is directed at China, we demur and see it as part of the larger attempt to make sense of a world that need not be divided on ideological grounds. The large German external surplus is unlikely to go unnoticed, and to be fair, the US is not the only one who has complained. The EC formally has, and some have several individual members.

The US releases the latest JOLTS report on job openings and late in the session, June consumer credit. These typically are not market-moving. Canada’s IVEY PMI will be released. The takeaway from the recent Canadian data is a firm economy (stronger than expected May GDP) and one that is weathering the trade tensions with the US as well as could be expected (small than expected trade deficit). Although Saudi Arabia appears to be escalating the diplomatic dispute over human rights into a full-blown crisis by reportedly recalling students, the Canadian dollar has recovered fully from the initial losses and edged above last week’s highs. Still, the US dollar may find a good bid ahead of CAD1.2960.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,newslettersent,USD/CHF