Stock MarketsEM FX has started the week mixed. Some relief was seen as US rates stalled out last week, but this Friday’s jobs number could be key for the next leg of this dollar rally. On Wednesday, the Fed releases its Beige book for the upcoming June 13 FOMC meeting, where a 25 bp hike is widely expected. We believe EM FX remains vulnerable to further losses. |

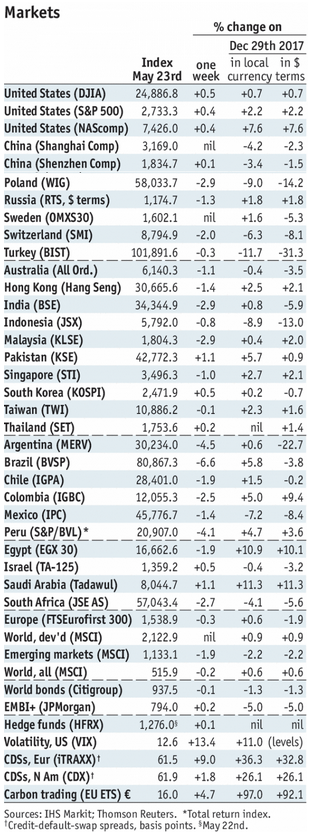

Stock Markets Emerging Markets, May 23 Source: economist.com - Click to enlarge |

BrazilBrazil reports April central government budget data Tuesday, where a BRL3 bln primary surplus is expected. Consolidated budget data will be reported Wednesday, along with Q1 GDP. Growth is expected to slow to 0.9% y/y from 2.1% in Q4. The decision to freeze diesel prices and offer subsidies to Petrobras is not good for the fiscal accounts. It also highlights how weak the Temer government is as it ends its term. South AfricaSouth Africa reports April budget, money and private sector credit data Wednesday. April trade will be reported Thursday, where a ZAR5 bln surplus is expected. SARB just left rates steady last week and seemed to lean dovish. PolandPoland reports May CPI Wednesday, which is expected to rise 1.9% y/y vs. 1.6% in April. If so, it would be the highest since January but still in the bottom half of the 1.5-3.5% target range. For now, the central bank is sticking with its pledge of steady rates through 2019. Next policy meeting is June 6, no change expected then. It releases minutes Friday. MexicoBanco de Mexico releases its quarterly inflation report Wednesday. It releases its minutes Thursday. The exchange rate will be the major determinant for monetary policy in the coming months. Next policy meeting is June 21, and much will depend on how markets are behaving ahead of the July elections. KoreaKorea reports April IP Thursday, which is expected at -1.4% y/y vs. -4.3% in March. It then reports May CPI and trade Friday. Inflation is expected to tick up to 1.7% y/y from 1.6% in April, while exports and imports are expected to grow 10.5% y/y and 10.0% y/y, respectively. Next BOK meeting is July 12, no change expected then.

|

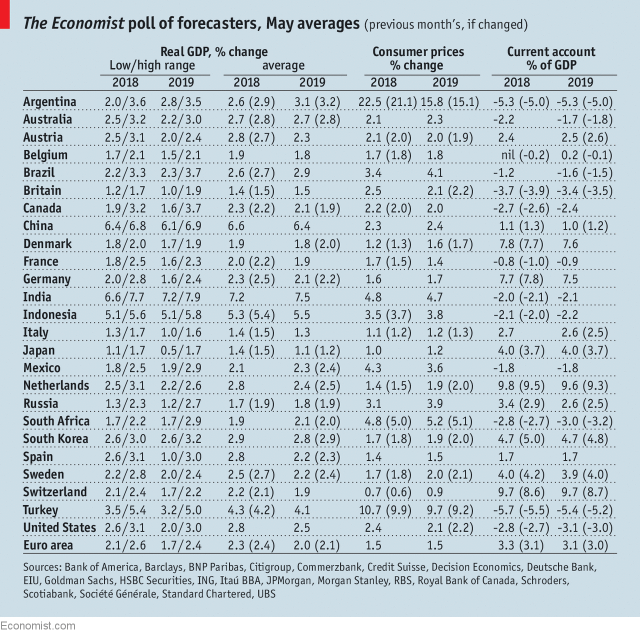

GDP, Consumer Inflation and Current Accounts The Economist poll of forecasters, May 2018 Source: economist.com - Click to enlarge |

China

China reports official May manufacturing PMI Thursday, which is expected to remain steady at 51.4. Caixin reports its China PMI Friday, which is expected to rise a tick to 51.2. For now, markets are comfortable with the stable economic outlook in China.

Turkey

Turkey reports April trade Thursday, which is expected at -$6.7 bln. If so, the 12-month total would rise to -$86.7 bln, the highest since June 2014. The external accounts are widening even as it is getting harder to finance them. Despite the decision to simplify the central bank’s policy rate, we expect downward pressure on the lira to continue.

India

India reports Q1 GDP Thursday, with growth expected at 7.3% y/y vs. 7.2% in Q4. The economy remains strong, while price pressures are picking up. Next RBI meeting is June 6. While no change is expected then, chances of a hawkish surprise have risen.

Chile

Chile reports April IP Thursday. April retail sales will be reported Friday. The economy is picking up nicely, while inflation remains low. Next policy meeting is June 13, no change expected then.

Thailand

Thailand reports May CPI Friday, which is expected to rise 1.3% y/y vs. 1.1% in April. If so, this would still be near the bottom of the 1-4% target range. Bank of Thailand has signaled that it’s in no hurry to hike rates. Next policy meeting is June 20, no change expected then.

Peru

Peru reports May CPI Friday. Inflation remains well below the 1-3% target range, and so the bank is likely to continue easing. Next policy meeting is June 7, and another 25 bp cut is possible.

Full story here Are you the author?

Tags: Brazil,Chile,China,Emerging Markets,India,Korea,Mexico,newslettersent,Peru,Poland,South Africa,Thailand,Turkey,win-thin