Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

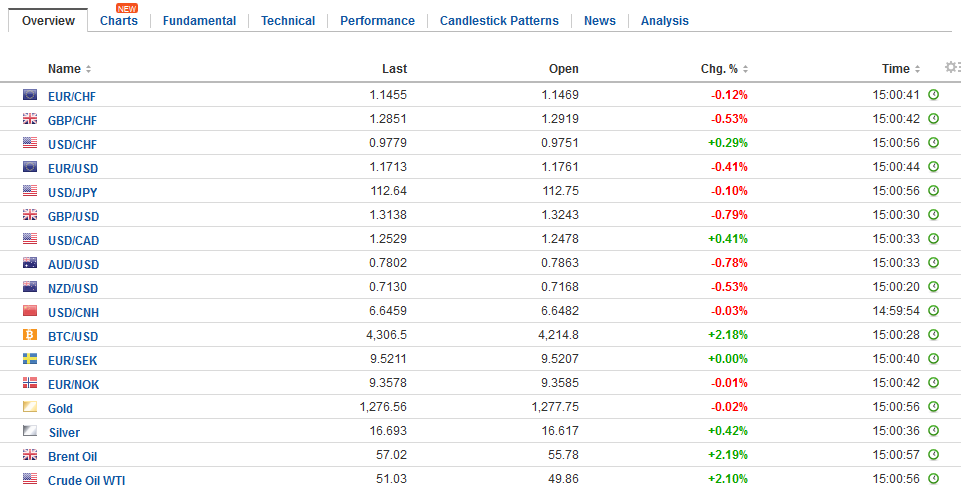

Swiss FrancThe Euro has fallen by 0.03% to 1.1461 CHF. |

EUR/CHF and USD/CHF, October 05(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesThe US dollar is mostly little changed as the broad consolidation that has emerged this week continues. The two powerful forces that have emerged–expectation of a Fed hike at the end of the year and European political challenges–appear to have reached a tentative equilibrium. Meanwhile, US President Trump’s comments about “wiping out” Puerto Rico’s $74 bln of debt remind investors of the unorthodox and unpredictable impulses from the US. Two currencies, sterling, and the Australian dollar are exceptions to the general calm of the foreign exchange market today. Sterling’s story is mostly about politics, it appears, while the Aussie’s weakness is in response to unexpected weakness in retail sales. UK Prime Minister May stole some thunder from the opposition by proposing the cap household energy prices, and boost social housing. Utility share prices did what one would expect in the face of a price cap and retreated. It was the hardest hit sector in the FTSE 250 on Wednesday, losing 0.7%, while the index as a whole slipped 0.3%. Her overall performance appeared to have failed to reset her administration. Sterling was slightly firmer before the Prime Minister spoke, helped by the stronger than expected service PMI. However, sterling trended lower and recorded the session lows late in North American turnover. The main factor that has slowed sterling’s descent in the face of the weak political backdrop and the poor technical condition is the anticipation that BOE will raise rates next month. While sterling has nearly returned to levels against the dollar last seen at the last BOE meeting’s hawkish forward guidance, the implied yield of short-sterling futures strip and the OIS remains high (implying around an 80% chance of a hike), and, of note, higher than the odds of Fed hike before the end of the year. |

FX Daily Rates, October 05 - Click to enlarge |

| Sterling traded sideways in Asia today, but as soon as European traders entered the fray, perhaps seeing how the British press reacted to May’s speech, sterling was sold. It has been pushed below $1.32 for the first time since the BOE meeting. The low on that day was about $1.3155. Sterling has also met the 50% retracement objective of the rally since late August. The 61.8% retracement is found near $1.3110.

The euro has carved what appears to be a rounded bottom against sterling over the past several weeks. The move above GBP0.8880 today opens the door to GBP0.8960-GBP0.9025. We note that sterling’s weakness continues in the face of little change in expectations for a BOE hike. Some observers are suggesting that the rate hike that so many are convinced will take place will be simply taking back the post-referendum rate cut and not the start of even a mini-tightening cycle. The cross-demand for the single currency is helping keep the euro firm against the dollar. The euro is trading inside yesterday’s range. The $1.1800 area continues to provide the near-term ceiling. The Catalonia-Madrid standoff continues, but the lack of fresh escalation has seen Spanish assets stabilize. Its two-year yield is up less than a basis point, and the Italian yield is up a little more than that. The 10-year yield is also little changed. This is more impressive than it may sound as the Spanish government went ahead with its scheduled bond sales, where the new supply, including some inflation-linked bonds, were easily absorbed. |

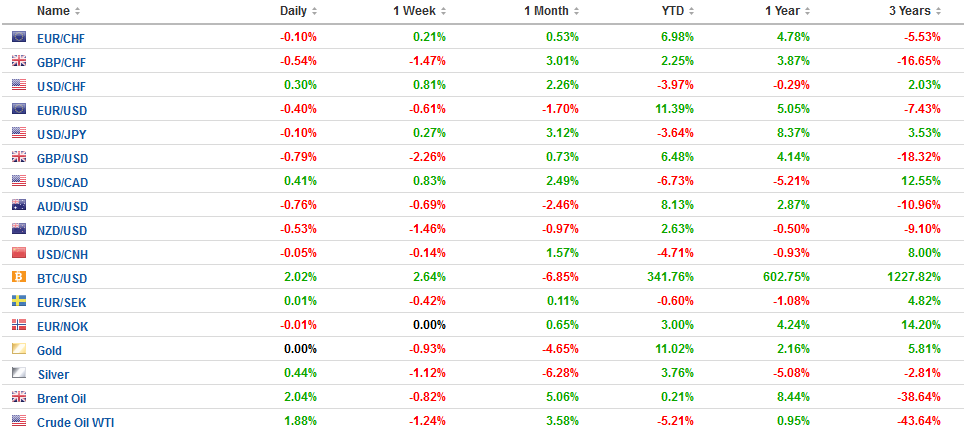

FX Performance, October 05 - Click to enlarge |

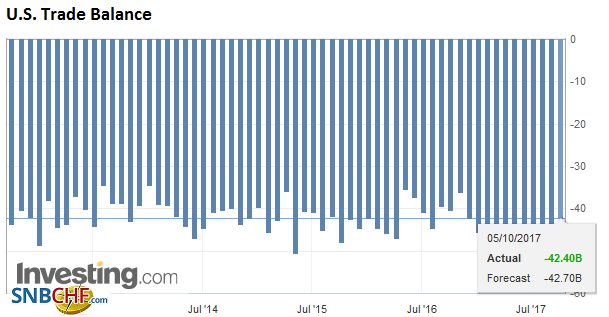

United StatesUS output is rising, and inventories are falling. The missing piece is exports. They have surged over the past couple of weeks, with last week’s exports reaching almost two mln barrels a day. Last year crude exports averaged about 600k a day. |

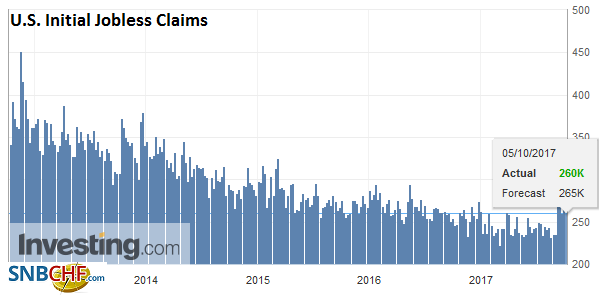

U.S. Initial Jobless Claims, 5 October 2017(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

| The combined exports of crude and refined products have reduced the US net imports to a record low. The US still imports oil. The latest data puts the important at around 7.2 mln barrels a day. The storms did skew the data, and it may not have entirely worked its ways through, but the widest spread between Brent and WTI in two-years ($6.0) is also encouraging US exports. The two-week surge in US exports is also made possible by the weaker demand from refineries as they continue to recover from the storm. |

U.S. Trade Balance, Aug 2017(see more posts on U.S. Trade Balance, ) Source: Investing.com - Click to enlarge |

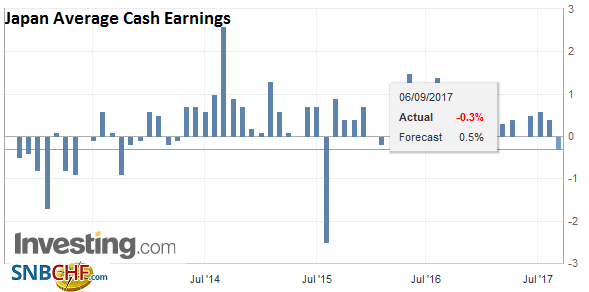

Japan |

Japan Average Cash Earnings YoY, October 2017(see more posts on Japan Average Cash Earnings, ) Source: Investing.com - Click to enlarge |

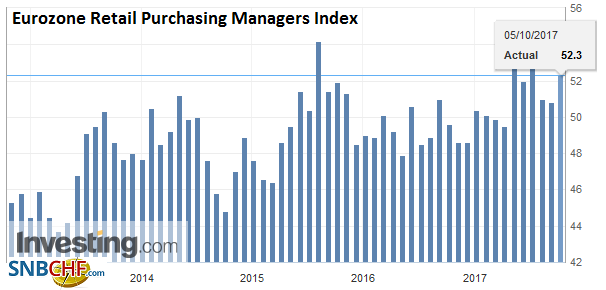

Eurozone |

Eurozone Retail Purchasing Managers Index (PMI), September 2017(see more posts on Eurozone Retail PMI, ) Source: Investing.com - Click to enlarge |

Spanish equities are up about 0.75%. The gains are broad, with only two sectors real estate and materials, trading lower. Today’s gains pare the week’s loss to about 3.3%, which would be the worst in about six weeks. It is best performing major bourse in Europe today as the Dow Jones Stoxx 600 is nursing a small loss for the second day.

Economists had expected Australian retail sales to have grown by around 0.3% after a flat report in July. Instead, retail sales fell by 0.6% in August, and, adding insult to injury, revised the July report to show a 0.2% decline. It is the first back-to-back decline in five years. News that the July trade surplus was near twice the initial estimate (now ~A$808 mln) and the August surplus was a bit larger than expected (~A$989 mln) was not sufficient to offset, and indeed may have made possible by the compression of domestic demand.

The Australian dollar is finding some support near $0.7820 after reached a one-week high yesterday near $0.7875. The week’s low, which a two and a half month low, was recorded near $0.7785. There do not appear to be large options strike near the money expiring today, but there is an A$1.1 bln option that will be cut tomorrow struck at $0.7800.

The November light sweet crude oil futures contract recorded a five-month high in late September near $52.85. It closed below $50 yesterday for the first time in 2 1/2 weeks. At $49.50 it would have retraced half the gains it has recorded since the late August low around $46.15. The next retracement objective is near $48.70. The five-day average is moving below the 20-day average for the first time in a month. Prices are steady today, but both Brent and WTI are off 2.7% and 3.2% on the week, which would be the largest losses in two months.

The recent rally which carried Brent to almost $60 and WTI to almost has also spurred some hedge-related sales, according to reports. And this reveals a contradiction in the OPEC strategy. If they succeed in drive the price of Brent higher, then this will see the US producers boost output and exports, and increasingly competing in third markets in Asia and Europe with OPEC.

The North American session features speeches by four Fed officials, including Powell, who has emerged as a candidate to replace Yellen as chair. The views of the regional presidents that speak today (Harker, George, and Williams) are well known. In the US, there are several economic reports today, including August factory orders (and the final durable goods orders) and trade balance. Barring a significant surprise, investors have already largely taken on-board that the US growth is acceptably near trend with some distortions to high frequency data due to the impact of the powerful storms. Weekly initial jobless claims, like the ADP yesterday, and likely reflected in tomorrow ‘s non-farm payroll report, have been adversely impacted, while the surge in auto sales and some strength seen in the PMIs are also storm-related.

Canada also reports August (merchandise) trade today. Perhaps the most important component will be non-oil exports, which have been soft. The implied yield on the December BA futures has eased to the lowest level in a month as the market take the cues by BOC officials that sought to ease rate hike speculation after two hikes at the last two meetings as the 2015 cuts are unwound in the face of strong growth. The US dollar was consolidating its recovery from about CAD1.2060 in early September to almost CAD1.2540 two days ago.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,EUR/CHF,Eurozone Retail PMI,Japan Average Cash Earnings,newslettersent,OIL,U.S. Initial Jobless Claims,U.S. Trade Balance,USD/CHF