Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

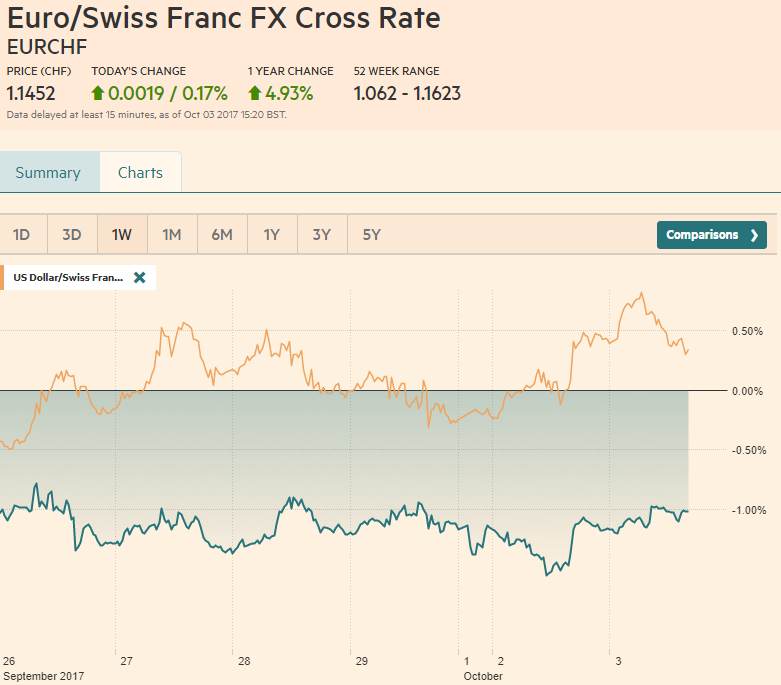

Swiss FrancThe Euro has risen by 0.17% to 1.1452 CHF |

EUR/CHF and USD/CHF, October 03(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesFirm US interest rates and a strong manufacturing ISM yesterday help support the greenback, while disappointing construction PMI in the UK weighs on sterling. The euro briefly slipped below $1.17 in Asia for the first time in six weeks. It has recovered toward the highs seen in North America yesterday (~$1.1760). There are several euro option strikes that may be in play today. In the euro, between $1.1750 and $1.1775, there are nearly 2.9 bln euros in options that expire today. And there are another nearly 900 mln euros struck at $1.18. Back-to-back weekend political developments in Europe have helped take the shine off the euro, alongside the greater confidence of a December Fed hike. The CDU won in Germany, as widely anticipated, but rather than a new Grand Coalition with the SPD, and now coalition with the FDP and Greens appears necessary. It may take the rest of the year to put into place. At the same time, the cost of the FDP participation, as well as the exposed right-flank of the CSU in Bavaria, could make for a Germany less inclined to push ahead with new post-Brexit, post-financial crisis integration, which Macron as proposed. |

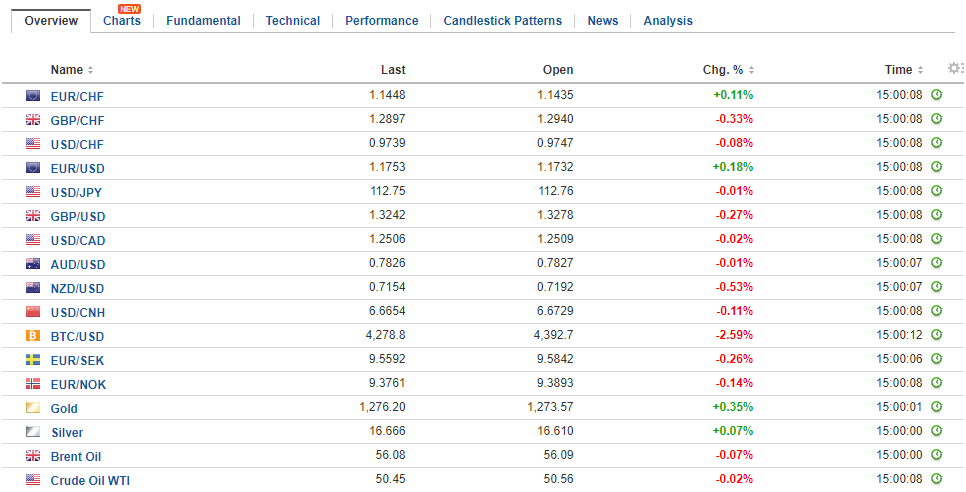

FX Daily Rates, October 03 - Click to enlarge |

| The service PMI that will be released tomorrow covers the largest part of the economy. Another disappointing report could see sterling move toward the 6.18% retracement, which is found near $1.3110. Meanwhile, the Tory Party Conference continues, and so far there haven’t been any fireworks. However, Johnson appears to be trying to separate himself from May, but each time he is called out, he returns to the fold, until the next time. Still, at this juncture, if Johnson resigns or is dismissed, sterling would likely to react positively. To be sure, this is not a prediction of Johnson’s departure, but rather simply the conclusion of thinking through the scenario.

The Reserve Bank of Australia’s meeting came and went without much fanfare. There was little change in the assessment or guidance. The central bank is on hold. The Aussie made a marginal new low (~$0.7785–low since mid-July) but rebounded back through $0.7800. Resistance is seen in the $0.7830 area. Ahead of the ADP report on Wednesday, and the storm-marred national jobs report before the weekend, the US reports September auto sales. A strong recovery is expected after a three-year low of 16.03 mln (SAAR) was reported for August. We caution that the storms’ impact will distort a broad range of data. We suspect that, in part, this explains the over-the-top strength seen in the manufacturing ISM (and not picked up by the Markit PMI), and it could help bolster the auto sales report. On the other hand, it is expected to depress the non-farm payroll report, with the Bloomberg estimate nearly half the year’s average. There are no Fed official speeches today, but several speak tomorrow, including Yellen and Powell, the later has moved up in the betting markets a candidate for the Chair. |

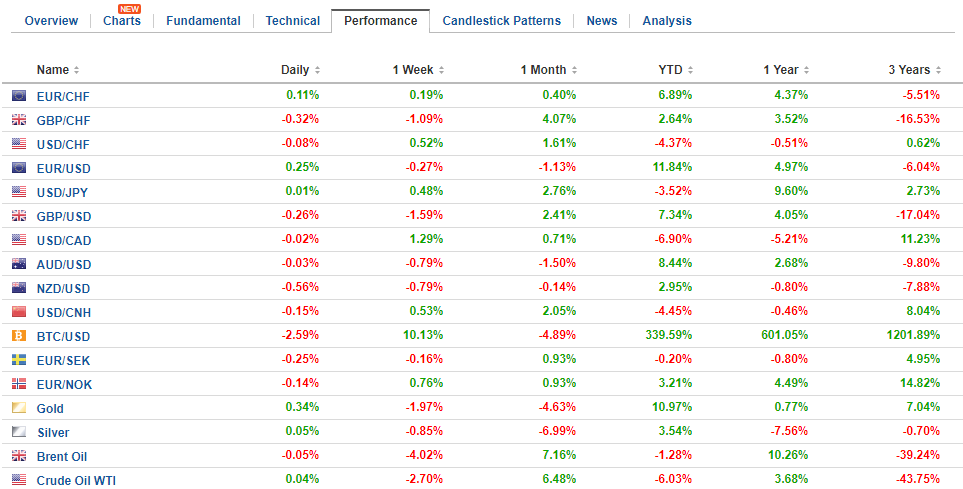

FX Performance, October 03 - Click to enlarge |

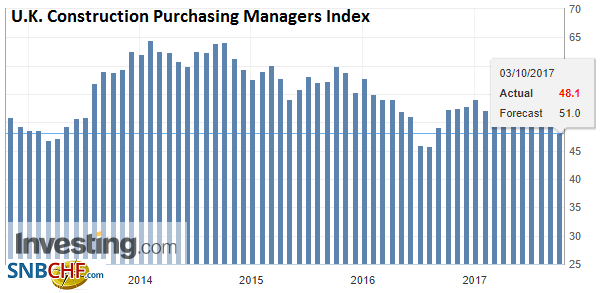

United KingdomThe UK’s manufacturing PMI disappointed yesterday (55.9 vs. 56.9 in August). Today it was the construction PMI. The 48.1 reading (from 51.1) is the lowest since last July and below the 50 boom/bust level. Sterling was sold on the news. It is lower for the third session and seven of the past eight. It broke through the 38.2% retracement of the advance since the late August low near $1.2775 yesterday (~$1.3320) and approached the 50% retracement (~$!.3215) today. The five-day moving average is breaking below the 20-day average for the first time in a little more than a month. |

U.K. Construction Purchasing Managers Index (PMI), Sep 2017(see more posts on U.K. Construction PMI, ) Source: Investing.com - Click to enlarge |

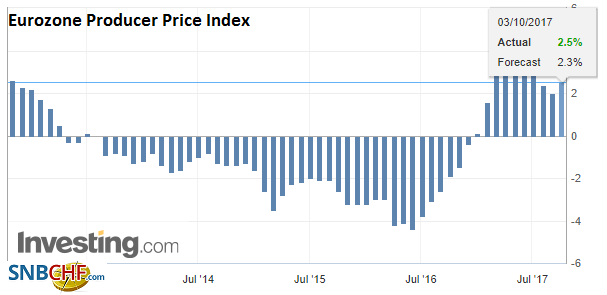

Eurozone |

Eurozone Producer Price Index (PPI) YoY, Aug 2017(see more posts on Eurozone Producer Price Index, ) Source: Investing.com - Click to enlarge |

This past weekend, Spain’s Catalonia region went ahead with a secessionist referendum that was ruled illegal by the Supreme Court. The low-level efforts of Madrid to hamper the referendum, and enforce the law, such as confiscating ballots, escalated to outright physical force to disrupt. The risk is now either a government crisis, where Rajoy, who leads a minority government, is forced to retreat or resign or a constitutional crisis.

Reports suggest Rajoy is considering invoking a 1978 constitutional article that lets Madrid revoke Catalonia’s regional status. Rajoy’s coalition partner, the newly-formed center-right Ciudadanos, supports such action, while the opposition Socialists favor talks with the secessionists, but not taking the more provocative step. Meanwhile, the Catalonia still seems to be pushing ahead with their independence. Things may come to a head on October 6, which is the anniversary of the execution by Franco of a leader of the Catalonia’s independence movement.

Investors remain fairly calm Spanish assets did underperform yesterday but are holding their today. The 10-year yield is up 1.2 bp today, but that is less than Italy and the core markets, including German Bunds. Over the past week, Spain’s premium over Germany has widened a single basis point. It is at the shorter-end of the curve that the pressure is evident. The 2-year yield is up nearly four basis points today, while Italy’s yield is slightly lower and the core yields are up less than two basis points. In the equity market, Spanish shares are slightly lower, off 0.15%. Over the past five sessions, it is up 0.5%.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?

Tags: #GBP,$AUD,$EUR,$JPY,EUR/CHF,Eurozone Producer Price Index,newslettersent,Spain,U.K. Construction PMI,USD/CHF