Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

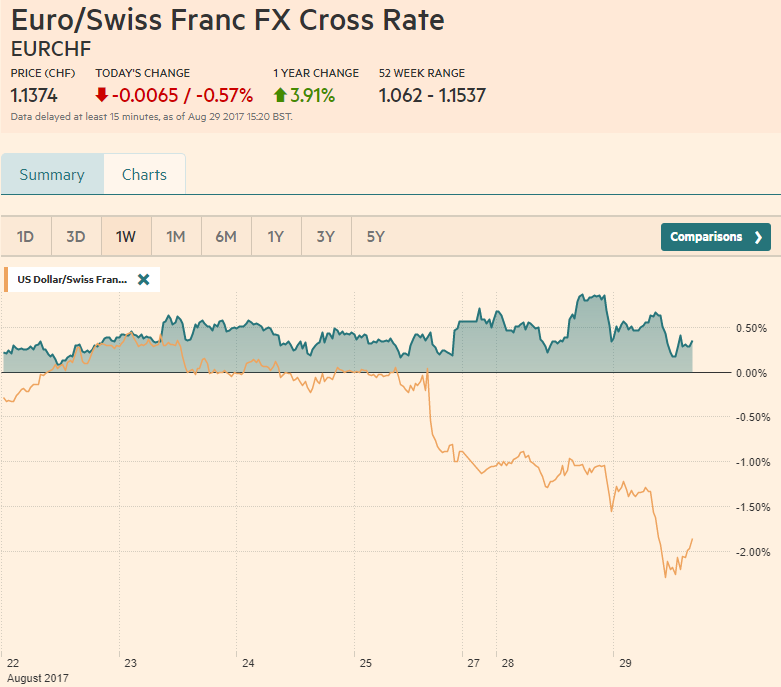

Swiss FrancThe Euro has fallen by 0.57% to 1.1374 CHF. |

EUR/CHF and USD/CHF, August 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesA brief period of quiet, which some may have confused with a change in posture, North Korea followed up the weekend’s test of three ballistic missiles with what appears to have been an intermediate missile that flew over Japan. South Korea responded with its own symbolic display of force by dropping bombs by the DMZ. In recent notes, we have explained that the US-South Korea annual military exercises antagonize North Korea. Last year, during these exercises it launched a missile from a submarine, which in military signaling, show second strike capability. That means that the first strike on North Korea risks a retaliatory strike. If a military option is not practical, it does not appear that pressure or sanctions work either. Japan condemned the North Korean action and calling for an emergency UN Security Council meeting. The US response is awaited. |

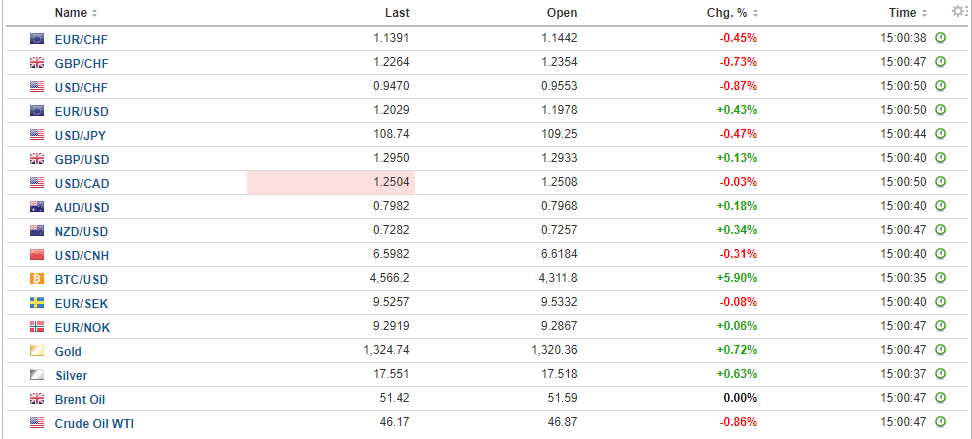

FX Daily Rates, August 29 - Click to enlarge |

| The US dollar’s sell-off that began before the weekend continued yesterday and is accelerating today. North Korea’s provocations have added to fuel to the fire that was already burning. Coming out of Jackson Hole, the consensus scenario of ECB tapering and Fed allowing its balance sheet to begin shrinking, and fading prospects of tax reform and an infrastructure initiative in the US, the greenback was vulnerable. In our assessment both fundamental and technical conditions had aligned that warned that the dollar’s recent consolidation was over and a new leg lower had begun.

The US dollar has been sold across the board. The Swiss franc, rather than the yen, is the strongest currency against the dollar, gaining a little more than 1% (~CHF0.9450). The yen is up about 0.6%. The dollar approached the year’s low (April 17 ~JPY108.10)., but caught a bid near JPY108.30 in the European morning. Resistance is seen in the JPY109.00-JPY109.20 band. The euro surge continued with the single currency reached $1.2070, its highest level since 2015. Recall that the $1.2170 area corresponds to a 50% retracement of the euro’s depreciation from mid-2014 until the start of this year. The weak dollar environment is allowing sterling to continue to recover. It had recorded two-month lows last week near $1.2775 and had strung together a four-day advance that carried it to nearly $1.2980. However, it is no match for the euro and other European currencies. The euro reached GBP0.9300 today. However, it is the dollar bloc that is underperforming today. The Australian dollar is the only major currency slipping lower on the day, and the New Zealand dollar is up 0.25%, which is the second weakest of the majors. The Canadian dollar began weakly but has come back bid, with the greenback posed to test the July low near CAD1.24. |

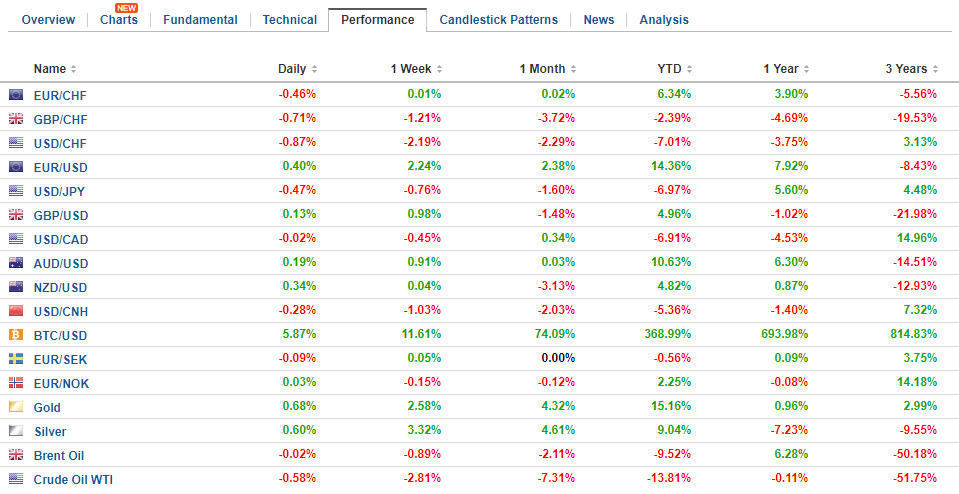

FX Performance, August 29 - Click to enlarge |

United StatesInterest rates remain at the center of our focus. The US 10- year yields are off more than six basis points to new lows for the year below 2.10%. Our concern has been that if the so-called Trump trade is being unwound, and the underlying trend growth of the US economy is not about to materially improve, the US 10-year yield may return to status quo ante, to where it was before the Trump trade, which we see as closer to 1.85%. |

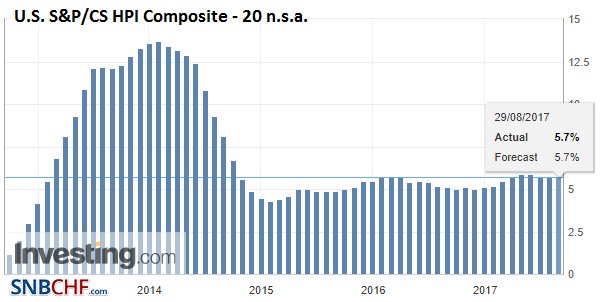

U.S. S&P/CS HPI Composite - 20 n.s.a. YoY, Jun 2017(see more posts on U.S. S&P/CS HPI Composite - 20 n.s.a., ) Source: Investing.com - Click to enlarge |

| Politically, we are concerned that Trump’s coalition is unraveling. The business wing is peeling off as more advisory boards face departures. A group of business leaders also wrote to Trump linking their support for the NAFTA renegotiation to preserving the trade tribunals, which the administration wants to jettison. Several links between the administration and the Republican Party have also been severed by personnel changes. The President has also come out swinging, critical of the Republican leadership in Congress. |

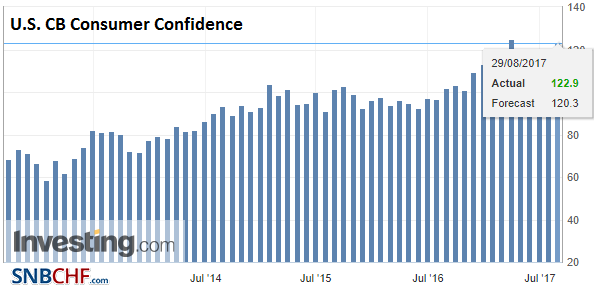

U.S. CB Consumer Confidence, Aug 2017(see more posts on U.S. CB Consumer Confidence, ) Source: Investing.com - Click to enlarge |

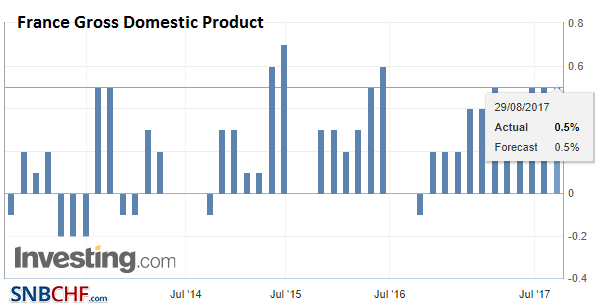

France |

France Gross Domestic Product (GDP) QoQ, Q2 2017(see more posts on France Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

Germany |

Germany GfK Consumer Climate, Sep 2017(see more posts on Germany GfK Consumer Climate, ) Source: Investing.com - Click to enlarge |

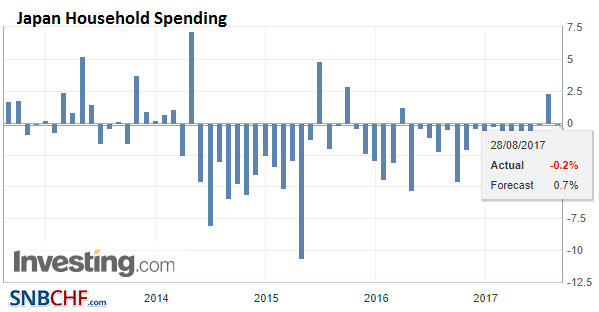

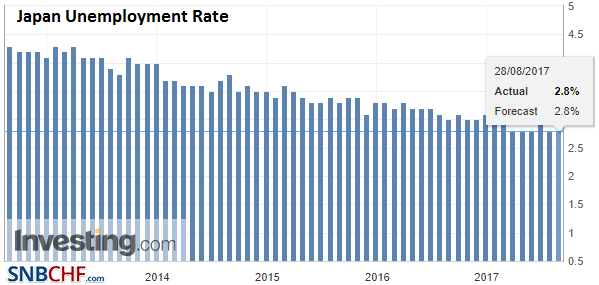

Japan |

Japan Household Spending YoY, Jul 2017(see more posts on Japan Household Spending, ) Source: Investing.com - Click to enlarge |

Japan Unemployment Rate, Jul 2017(see more posts on Japan Unemployment Rate, ) Source: Investing.com - Click to enlarge |

The debt ceiling and spending authorization also have to be resolved in the coming weeks. The uncertainty is also distorting the bill market. And look at the US CDS. It has fallen to 20bp at the end of July and now is near 26 bp. That means it costs 26k euros to insure 10 mln euros worth of Treasuries against default. To be sure this is still low in absolute terms, though the highest among the G5.

In addition to the tensions on the Korean peninsula and the poor dollar backdrop, there is another force at play. Over the last couple of week, the UK issued nearly a dozen position papers that laid out its emerging views on a range of issues that largely related to the post-Brexit relationship. As we looked through the topic and papers, it dawned on us that the UK was missing the EU’s point and, since in our understanding, once Article 50 was triggered, the initiative went to the EU, we thought this was significant. Yesterday’s the EU’s chief negotiator Barnier called the UK to the task, arguing that it had still not addressed the preliminary issues.

These preliminary issues which the EU insists on addressing first involve the terms of the separation, which given the organic growth over the last 40 years, and the complexity of the issue, we suggest is more like an amputation than a divorce. Juncker echoed these remarks. This is important because the EU Summit is about eight weeks away, and it is then that if there was sufficient progress on the preliminary issues that the next phase could begin, which involves the issues that are dear to the UK. While brinkmanship tactics can be expected, the chasm is still wide.

A Bloomberg reporter captured the UK’s exasperation: “The UK camp believes negotiations could progress if Barnier’s team did not follow its mandate to the letter.” If a fair assessment, it suggests a certain naivete and unpreparedness on the part of the UK. At the very least, one should expect one’s adversary to stick to the letter of the law in these matters. Of course, other scenarios may be considered, but isn’t the letter of the law the base case?

Global equities are lower. Asia markets recovered from steeper losses and the MSCI Asia Pacific Index managed to close only 0.15% lower. Korea’s Kospi was off 1.6% at its worst and closed only 0.2% lower. European shares are down for a third session and lose have accelerated. The Dow Jones Stoxx 600 is off 1.4%, led by telecoms, financials,and industrials. Bond markets have rallied. Core European yields are off 4-5 bp. Italian and Portuguese bonds are not participating in the rally. Japan’s 10-year benchmark yield is below zero for the first time since April.

Graphs and additional information on Swiss Franc by the snbchf team.

Are you the author?Tags: #GBP,$AUD,$CAD,$EUR,$JPY,$TLT,EUR/CHF,France Gross Domestic Product,Germany GfK Consumer Climate,Japan Household Spending,Japan Unemployment Rate,Korea,newslettersent,U.S. CB Consumer Confidence,U.S. S&P/CS HPI Composite - 20 n.s.a.,USD/CHF