Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

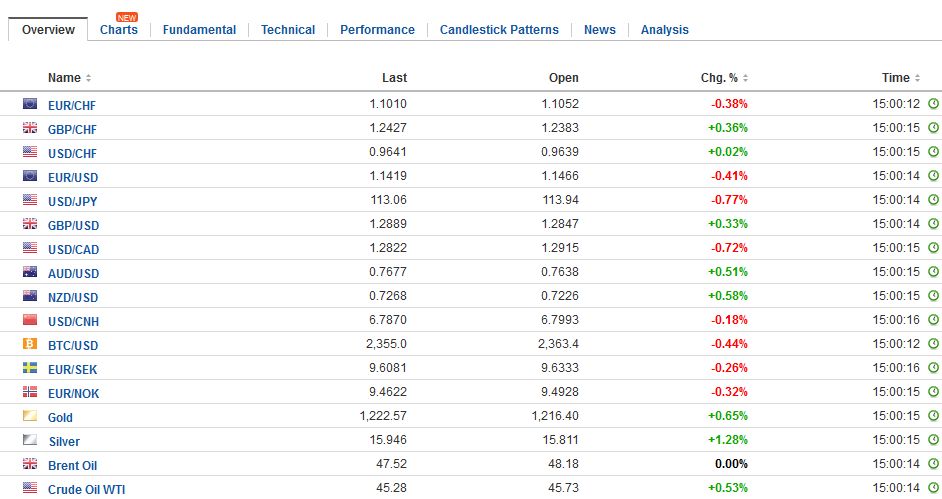

Swiss FrancThe Euro has fallen by 0.37% to 1.1011 CHF. |

EUR/CHF - Euro Swiss Franc, July 12(see more posts on EUR/CHF, ) - Click to enlarge |

GBP/CHFhe Pound has fallen vs the Swiss Franc after two of the members of the Monetary Policy Committee spoke yesterday. Ben Broadbent has stated that he’s ‘not ready’ to raise interest rates just yet and after the 5-3 split in the announcement earlier this month the markets were expecting both him and Andy Haldane to be hawkish in their tone. The reverse happened and combined with Kristin Forbes who has left since the vote and voted for a rate hike the appetite for a rate hike looks to be diminishing very fast. This news has caused the Pound to fall to its lowest level in a month to buy Swiss Francs and I think we’ve got further falls ahead for GBPCHF exchange rates coming. Later this morning UK unemployment is set for release and although we are close to the lowest level since the 1970s the real issue for the UK economy is that Average Earnings which are not keeping up with inflation. Inflation levels are currently at 2.9% with Average Earnings set to hit 1.9% so the disparity between the two figures is causing concern for the British economy. Effectively it means wages are not keeping up with inflation which means the cost of living is going up which is not a good sign and therefore this is being reflected in the value of the Pound against all major currencies including vs the Swiss Franc. Indeed, the Pound is now at its lowest level vs the Euro since November last year. With the Swiss Franc often used as a safe haven currency this is another reason why the Swiss Franc has been strengthening vs the Pound over the last few weeks. |

GBP/CHF - British Pound Swiss Franc, July 21(see more posts on GBP/CHF, ) - Click to enlarge |

FX RatesThe US dollar and sterling have stabilized after being sold off yesterday. The yen, which had begun recovering from a four-month low, is the strongest of the major currencies today, gaining around 0.5% against the dollar (@~JPY113.40). Global bond yields are softer. The BOJ stepped up its purchases of three-five year bonds to JPY330 bln from JPY300 bln, though kept its other purchases unchanged. The market responded accordingly and took Japanese rates lower. With a backdrop of softer global rates, it may not be a clean test of the market’s reaction function. The price action reinforces the importance of the 2.40%-2.42% threshold for the US 10-year Treasury yield. Sterling recovered fully from its earlier losses in response to the employment data. The earlier losses had knocked sterling to almost $1.2810, extending yesterday’s drop. Although the BOE’s Deputy Governor Broadbent did not address his monetary policy views directly in yesterday’s speech, in a newspaper interview, he did. He was clear. He is not ready to endorse a rate hike, though recognizes pressures may be building. Broadbent seemed particularly sensitive to the high degree of uncertainty or what he called “imponderables.” |

FX Daily Rates, July 12 - Click to enlarge |

| The euro made a new high for the year against sterling today near GBP0.8950 but has reversed course and is returned to GBP0.8900 in late European morning turnover. Given yesterday’s big outside day and the follow through gains earlier, we suspect participants will be more inclined to buy the euro on dips. A move to GBP0.8860-GBP0.8880 may be seen as such a dip.

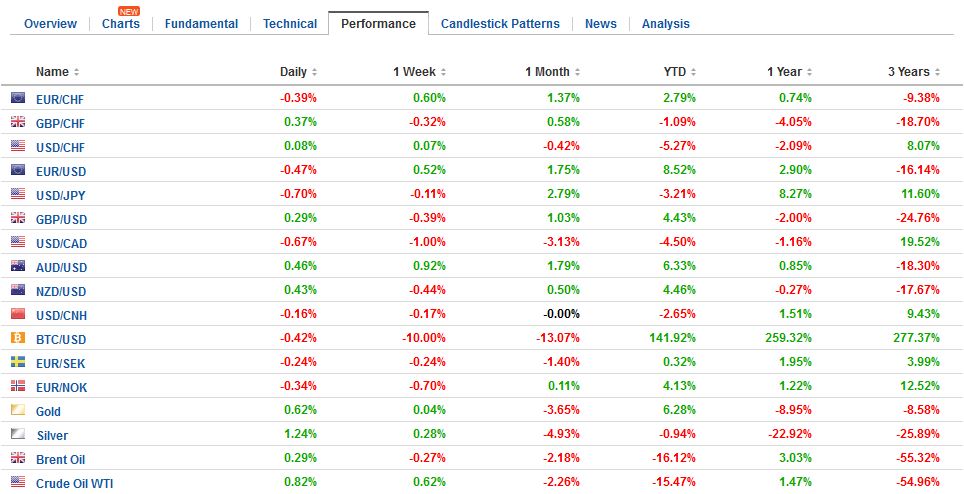

After posting strong gains at the end of last week after the employment data removed the last potential obstacle (some thought) to today’s rate hike, the Canadian dollar has been sold a bit so far this week and is off about 0.4%. That makes it the second worst major performer this week behind the New Zealand dollar, which is off 0.65%. We also note that speculators in the futures market are net short Canadian dollars but net long the Australian and New Zealand dollars. That said, the Canadian dollar has come a long way over the past two months (~6.5%), and the technical indicators warn that while there may be another test higher, the risk is for a deeper correction that lifts the greenback the CAD1.3000-CAD1.3020 area. We see many considerations pushing in the same direction, including a judgment that the risks emanating from the US had appeared to lessen. US growth was not as poor in Q1 as it had initially appeared, and the rhetoric and threat of a trade war also seemed to diminish. Also, there does appear to be a synchronous expansion underway, reducing the global risks. And all this in a backdrop of stronger Canadian economic data and the likelihood that the output gap is closed sooner than previously projected. |

FX Performance, July 12 - Click to enlarge |

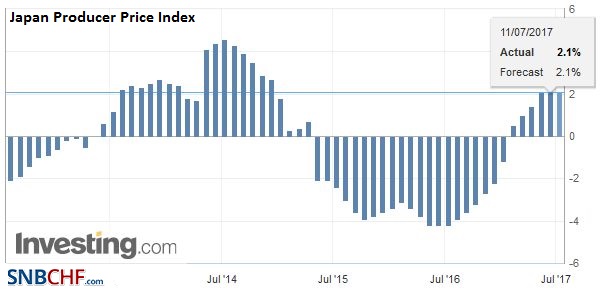

Japan |

Japan Producer Price Index (PPI) YoY, June 2017(see more posts on Japan Producer Price Index, ) Source: Investing.com - Click to enlarge |

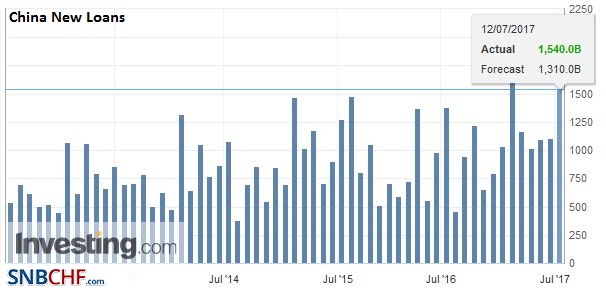

China |

China New Loans, June 2017(see more posts on China New Loans, ) Source: Investing.com - Click to enlarge |

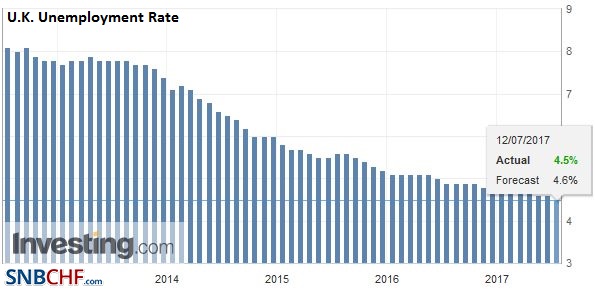

United KingdomThe UK’s labor report had something for everyone. The unemployment rate ticked down to a new generational low of 4.5% from 4.6%. The three-month change in employment rose to 175k. The median forecast was for the 120k increase. The claimant count increased by 6k after a 7.5k increase in May. |

U.K. Unemployment Rate, May 2017(see more posts on U.K. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

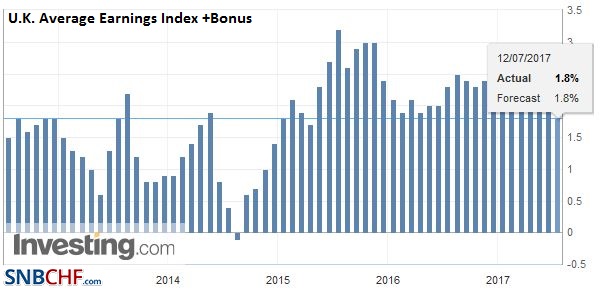

| Even earnings were mixed. At the headline level, they rose 1.8% in the three-months year-over-year period, down from 2.1% in April and in line with expectations. |

U.K. Average Earnings Index +Bonus, May 2017(see more posts on U.K. Average Earnings Index, ) Source: Investing.com - Click to enlarge |

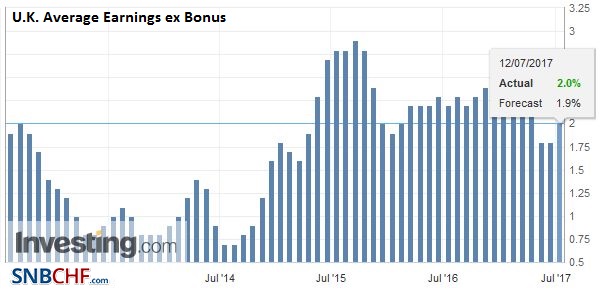

| Excluding bonuses, the pace was a bit stronger than expected at 2.0%, up from a revised 1.8% in April (from 1.7%). |

U.K. Average Earnings ex Bonus, May 2017(see more posts on U.K. Average Earnings, ) Source: Investing.com - Click to enlarge |

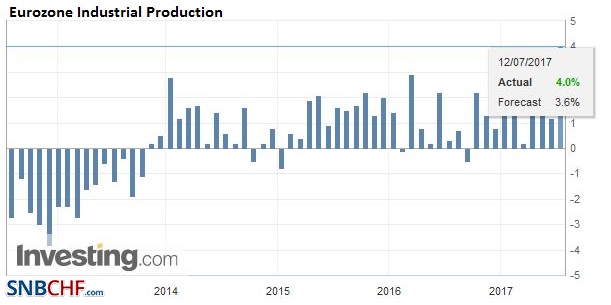

EurozoneThe eurozone reported a strong aggregate rise in industrial output in May. The four largest economies had already reported national figures, so what appears to be an overshoot may be less than meets the eye. It rose 1.3% on the month; the April rise was shaved to 0.3% from 0.5%. Nevertheless, the year-over-year pace rose to 4.0% from a revised 1.2%, which is the fastest since 2011. The ECB meets next week. We expect a small tweak in the forward guidance to remove the risk that asset purchases can be increased if necessary. |

Eurozone Industrial Production YoY, May 2017(see more posts on Eurozone Industrial Production, ) Source: Investing.com - Click to enlarge |

United States |

U.S. Crude Oil Inventories, June 2017(see more posts on Wholesale Inventories, ) Source: Investing.com - Click to enlarge |

Most accounts appear to be giving the email’s of US President Trump’s son central role to yesterday’s dollar slide that saw the euro rise to new highs for the year. While there could be broad medium term political implications but perhaps the most important considerations was the obvious distraction to the economic agenda. At the same time, there are a couple of other factors at work as well.

The Federal Reserve Board of Governors has four of the seven seats filled. Brainard’s cautious stance must be taken seriously. At the same time, her willingness to begin allowing the balance sheet to shrink illustrates a point we continue to make. A consensus on reducing the balance sheet appears to have been achieved, while a consensus on the next rate hike has not crystallized.

Yellen’s testimony beginning today is one of the highlights of the week. However, it may be too much to expect her to break new ground. Not much new is known since the mid-June press conference. At most, she will put more flesh on the bones, and explain to the representatives, who are not economic or financial experts the trajectory of policy and the nuances of the balance sheet, and Phillip’s Curve.

Also, the Senate is making a new attempt on health care. The new measure no longer repeals two taxes on high income earners, worth about $230 bln over a decade. The funds can be used to finance other parts of the reform that will address some of the previous objections. The bill is reportedly going to go to the CBO for scoring. The Senate leadership will then present the bill tomorrow, according to press reports. A procedural vote could happen as early as next week. There has also been a two-week delay in the summer recess, which now won’t begin until mid-August.

Canada

The Bank of Canada is widely expected to raise rates by 25 bp today. Senior officials appear to have engaged in a month-long campaign to prepare the market. Many observers are trying to assess what changed for officials that they have been aggressive in pushing from easing rise at the beginning of the year to neutral at the start of Q2 to a sense of urgency now.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$CAD,$EUR,$JPY,China New Loans,EUR/CHF,Eurozone Industrial Production,FX Daily,gbp-chf,Japan Producer Price Index,newslettersent,U.K. Average Earnings,U.K. Average Earnings Index,U.K. Unemployment Rate,U.S. Crude Oil Inventories,Wholesale Inventories