Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Poor jobs growth won’t challenge June hike expectations but September and balance sheet.

Little positive in today’s report. Drop in unemployment explained by drop in participation rate.

Trade deficit was larger than expected, which may point to slower Q2 growth.

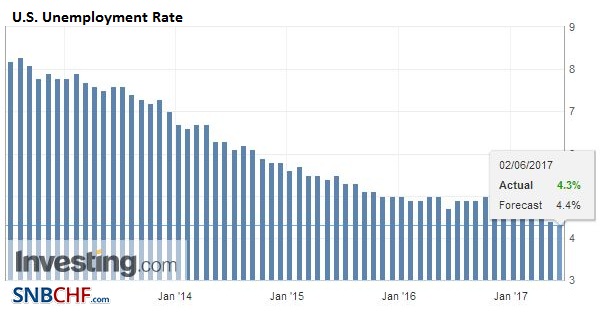

United StatesUnemployment RateThe US unemployment rate unexpectedly fell to 4.3%, a new multi-year low, but it is a misleading optic for what is a disappointing report. It is likely not weak enough to put much doubt into expectations for a Fed hike later this month, but it will reinforce the caution in the Beige Book and in recent comments from some Fed officials. Besides the decline in the unemployment rate, and a further decline in the under-employment rate (U-6) from 8.6% to 8.4%, there is little positive in today’s report |

U.S. Unemployment Rate, May 2017(see more posts on U.S. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

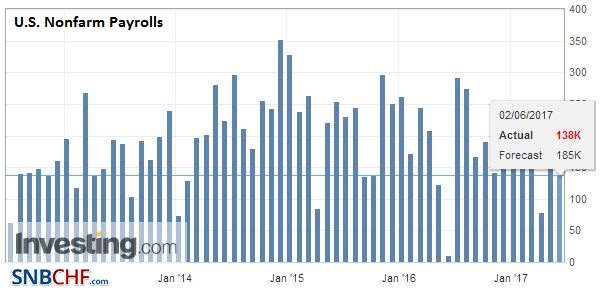

Nonfarm PayrollsNon-farm payroll growth fell to 138k, nearly 50k below median expectations, which like our own, had been bolstered by the weekly jobs claims, withholding tax, and the ISM. There is not a good month-to-month fit with the ADP report, but the strength of it yesterday, seemed to have precluded today’s downside surprise. Adding insult to injury, the back to months saw jobs growth revised 66k lower. |

U.S. Nonfarm Payrolls, May 2017(see more posts on U.S. Nonfarm Payrolls, ) Source: Investing.com - Click to enlarge |

Participation RateMoreover, the drop in the unemployment rate can largely be explained by the decline in the participation rate from 62.9% to 62.7%. This unwinds this year’s improvement in the participation rate, and bring it back to where it finished last year. |

U.S. Participation Rate, May 2017(see more posts on U.S. Participation Rate, ) Source: Investing.com - Click to enlarge |

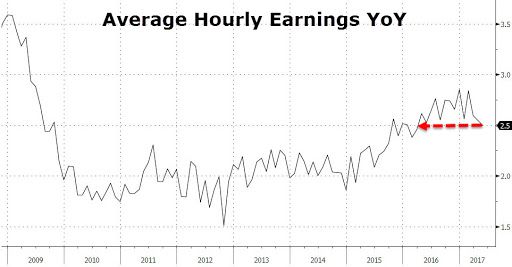

Average Hourly EarningsAverage hourly earnings rose 0.2%, which was in line with expectations. However, here the detail mars the constructive optic. The 0.3% rise reported in April was revised to 0.2%. This leaves means that the year-over-year rate is unchanged in May at 2.5%. |

U.S. Average Earnings, May 2017(see more posts on U.S. Average Earnings, ) Source: Zerohedge.com - Click to enlarge |

Although the euro has made a new high for year on the news, the Dollar Index has not made a new low (yet). The euro reached $1.13 in the immediate reaction to the US election last November. Options worth roughly 1.1 bln euros struck there expire today. US interest rates have fallen and the yield curve is flattening (2y-10y). Without higher US rates, it is difficult for the dollar to resume its uptrend. The market is also going to need evidence that the economy (and inflation) are recovering before becoming convinced that there will be a hike in September. It could also delay the timing of the Fed allowing some maturing issues to roll off in an attempt to shrink its balance sheet.

Separately, the US reported a larger than expected April trade deficit. This alone will encourage economists to revise down Q2 GDP forecasts. Exports fell 0.3% and imports rose 0.8%. If there is a silver lining, it may be that capital equipment imports rose to their highest level in two years. An increase in investment may be needed to boost productivity.

Full story here Are you the author?

Tags: #USD,$EUR,$JPY,jobs,newslettersent,U.S. Average Earnings,U.S. Nonfarm Payrolls,U.S. Participation Rate,U.S. Unemployment Rate