Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss FrancThe Euro has fallen by 0.11% to 1.0852 CHF. |

EUR/CHF - Euro Swiss Franc, June 08(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesToday has an anti-climactic feel to it. Yesterday’s leak of what is purported to be the ECB staff forecasts point to small downward revisions to inflation forecasts and an ever small upward tweak to growth. This would be in line with only mild changes in the forward guidance language. The clear indication is that inflation is still not the conditions of a self-sustaining path toward the target. What follows from that assessment is that it is premature to retreat from any of the unorthodox measures. The asset purchases run through the end of the year. The September ECB meeting is seen as a likely venue to announce the continuation of asset purchases beyond the end of the year albeit at a slower pace. |

FX Daily Rates, June 08 - Click to enlarge |

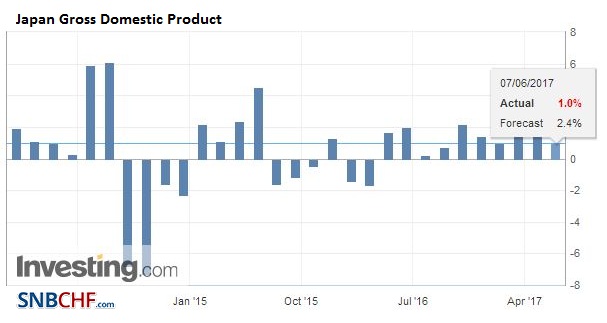

| The Japanese yen is the weakest of the majors, losing about 0.25% against the dollar. The greenback has resurfaced above JPY110 after spending yesterday entirely below there. The dollar has recouped a big figure after finding bids ahead of JPY109 yesterday. Firmer US yields helped. Today Japan reported an unexpected cut in the Q1 GDP estimate to 0.3% from 0.5%. Public investment and consumption were revised lower, and oil inventories also fell. The dollar may encounter resistance in the JPY110.50-JPY110.75 band.

The point to bear in mind is that because of the output gap, growth alone is necessary but insufficient to change the ECB’s stance. Prices have to rise. Meanwhile, the euro remains near its recent highs. Buying yesterday’s pullback seems to point to the path of least resistance. There was a brief attempt yesterday to shake out the weak longs, but it failed as new buying emerged ahead of $1.12. |

FX Performance, June 08 - Click to enlarge |

EurozoneTwo economic data today support the eurozone growth story. Growth in Q1 was revised up to 0.6% from 0.5%. This lifts the year-over-year rate to 1.9% from 1.7%. It appears the revision was aided by capital investment. Household consumption was revised slightly lower, and government expenditures were unchanged. |

Eurozone Gross Domestic Product (GDP) YoY, Q1 2017(see more posts on Eurozone Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

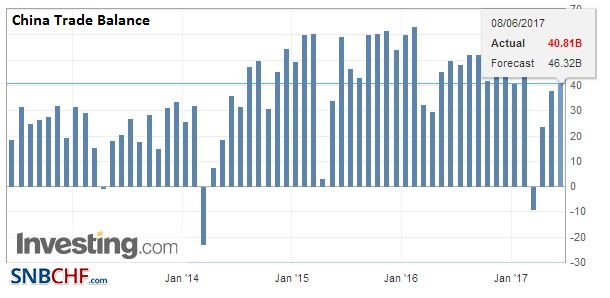

ChinaChina also reported its May trade balance. It rose to $40.8 bln from $38.3 bln in April. Exports rose 8.7% year-over-year. It is the third consecutive increase in exports. Recall last year they fell at an average pace of about 6%. Imports rose 14.8% after an 11.9% pace in April. |

China Trade Balance, May 2017(see more posts on China Trade Balance, ) Source: Investing.com - Click to enlarge |

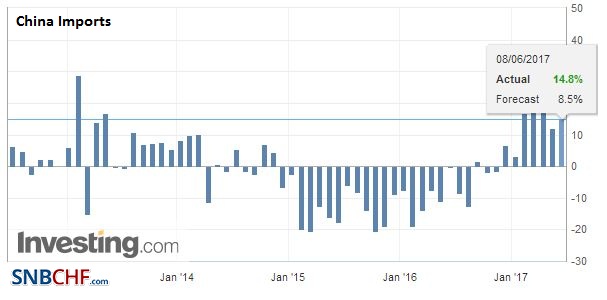

| Imports were stronger than expected and that explains why the trade surplus was smaller than expected. Imports of iron ore rose by nearly 8% in volume terms year-over-year and nearly 68% in value terms so far this year. Coal imports rose 133% in value and crude oil nearly 65%. |

China Imports YoY, May 2017(see more posts on China Imports, ) Source: Investing.com - Click to enlarge |

| News that China’s imports from the US rose 27% in May from a year ago will likely be embraced as a success of the US trade policy. China’s exports to the US have risen 11.5% from a year earlier. After appreciating sharply (for the yuan) at the end of May, it has reverted to narrower ranges and small moves. Consolidation appears to be the theme. |

China Exports YoY, May 2017(see more posts on China Exports, ) Source: Investing.com - Click to enlarge |

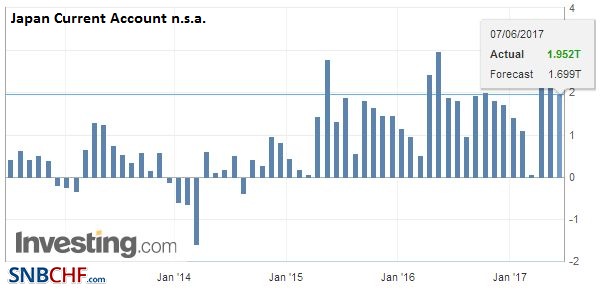

JapanSeparately, Japan reported a larger than expected April current account surplus. Remember Japan’s current account balance is not driven by the trade surplus (~JPY553.6 bln in April), but the primary investment income (e.g. coupons and dividends, profits on foreign investment) accounts for the bulk of the remainder of the JPY1.95 trillion surplus. |

Japan Current Account n.s.a., April 2017(see more posts on Japan Current Account n.s.a., ) Source: Investing.com - Click to enlarge |

Japan Gross Domestic Product (GDP) YoY, Q1 2017(see more posts on Japan Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

|

United States |

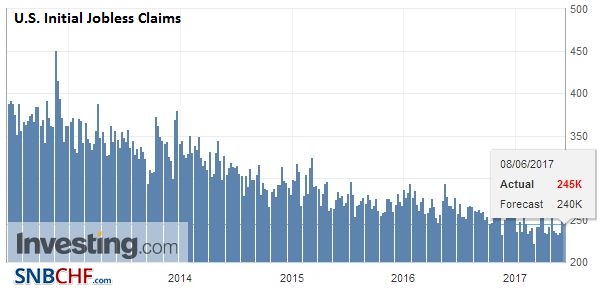

U.S. Initial Jobless Claims, May 2017(see more posts on U.S. Initial Jobless Claims, ) Source: Investing.com - Click to enlarge |

Former FBI Director Comey’s prepared remarks were released ahead of his testimony today. There is much attention drawn to today’s hearing, and it will be televised live. It may make for good theater, but it is unlikely to be the kind of thing that moves the capital markets. It seems widely recognized that Comey’s “revelations” may not be very flattering for the President, but they do not rise to the level of illegality. Keep in mind that this is one hearing of one of the two investigations being conducted by Congress, and the FBI is conducting its own investigation. These are early days.

Lastly, we note that oil prices are stabilizing after yesterday’s 5% tumble. The drop was sparked by US inventory data. It not only showed the first increase in US crude oil stocks, but across the carbon products, the inventories rose by 15.5 mln barrels, the largest weekly increase in nine years. The US 10-year yields, which the dollar seems to be particularly sensitive to, firmed yesterday despite the sharp drop in oil. The yield is up a couple more basis points today at 2.20%, the highest this week and eight basis point advance from Tuesday’s low print.

Germany

The prospects for Q2 look solid, given the PMI readings. Today German reported stronger than expected April industrial output figures, after disappointing orders data yesterday. Output rose 0.8% compared to the Bloomberg median estimate of 0.5%, and the March decline was revised to 0.1% from -0.4%.

United Kingdom

The outcome of the UK election is the known unknown of the day. The voting end at 10:00 BST (5:00 pm ET) and exit polls will be reported shortly after that. The results will likely be known within a few hours before many North Americans retire for the evening. Sterling is little changed today. It was little changed last week too, but it is little changed higher for the last four sessions coming into today and in seven of the past eight sessions.

If and as much as the outcome deviates from the Tory majority government, the worse sterling and UK assets will likely do on first blush. At the same time, keep in mind that developments that support a softer Brexit have elicited positive responses by investors. For sterling, the top side had been blocked by the $1.3055 technical level. On the downside, we suspect the bulls will allow for some choppiness, but a break of $1.2830-$1.2850 may be a little worrisome.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: $JPY,China Exports,China Imports,China Trade Balance,EUR/CHF,Eurozone Gross Domestic Product,FX Daily,Japan Current Account n.s.a.,Japan Gross Domestic Product,newslettersent,U.S. Initial Jobless Claims