Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, May 02(see more posts on EUR/CHF, ) - Click to enlarge |

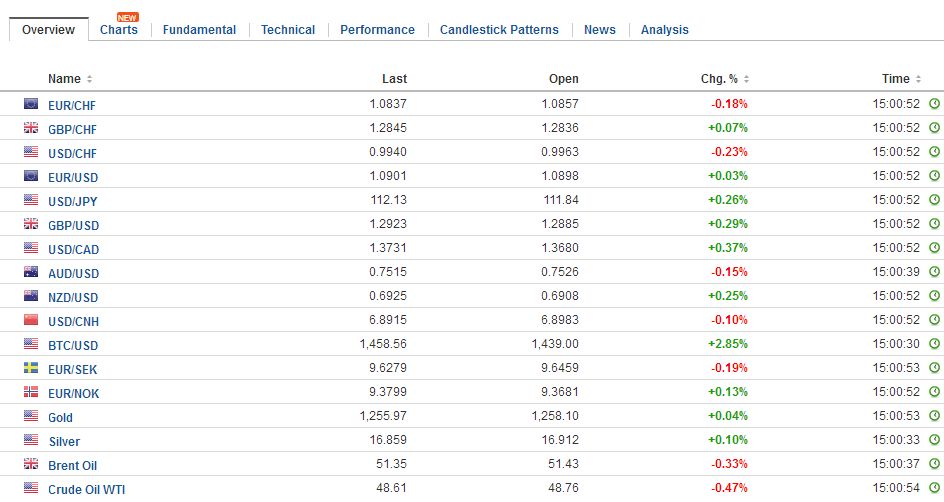

FX RatesThe US dollar is sporting a softer profile against most of the major and emerging market currencies. The Japanese yen is the main exception. The greenback is rising against the yen for the fourth session and the sixth of the past seven. The dollar’s gains against the yen coincide with the 10-12 bp recovery in the US 10-year yields over the past ten sessions. The latest uptick in US yields, with the 10-year yield trying to re-establish a foothold above 2.30%, may have been spurred by the strong reiteration by the US Treasury Secretary that extra-long maturity is being analyzed. Mnuchin has been saying this for some time, but yesterday’s comments seemed to be a strengthening of the likelihood that a 50-year bond will be issued. Reports have suggested that primary dealers are less enthusiastic and are concerned about liquidity and costs. Mnuchin is more interested in the appeal of locking in low rates longer. Other countries, including Canada, France, Switzerland, and the UK have issued 50-year bonds. The US did to fund the Panama Canal over a century ago. At the end of March, which also marked the end of Japan’s fiscal year, the US dollar reached a high of JPY112.20. Today it is edged through there. The JPY112.15 area also corresponds with the 38.2% retracement of the dollar’s decline since the high near JPY118.60 on January 3. The trend line connecting that January high and the March 10 high near JPY115.50 comes in now near JPY113.10. There is a large (~$1.1 bln) option struck that JPY111.80 that expires today. |

FX Daily Rates, May 02 - Click to enlarge |

| The euro continues to chop in the upper half of its $1.0850-$1.0950 range. A $1.10 strike, estimated at 1.4 bln euros, expires today and tomorrow the $1.0925 strike sees 1.0 bln euros roll-off. Our reading of the near-term technicals does not rule out a move to $1.10 or even a bit through it. However, the technical indicators are getting stretched.

Sterling recovered from a three-day low near $1.2865 on the news but is barely poked through $1.29. Resistance in the $1.3000-$1.3055 area is expected to be formidable and spurring some caution. Here too the technicals are getting stretched, but a marginal new high cannot be ruled out. The euro is recovering from a test on GBP0.8400 at the end of last week and yesterday and appeared to find offers as its approached GBP0.8500 and a downtrend line drawn from the end of March high. As widely expected the Reserve Bank of Australia kept policy unchanged. Many economists still think the RBA will have to ease monetary policy later this year. The RBA shows little sign of moving in that direction. Instead, it appears to be putting more hope on fiscal policy. An infrastructure plan will likely be unveiled at next week’s budget. It may include rail and road projects and a second airport. The Australian dollar initial extended yesterday’s gains but lost momentum around $0.7550. This area corresponds with the 38.2% retracement of the decline from the March 21 high near $0.7750. The $0.7600 area is the 50% retracement and the high from late April. |

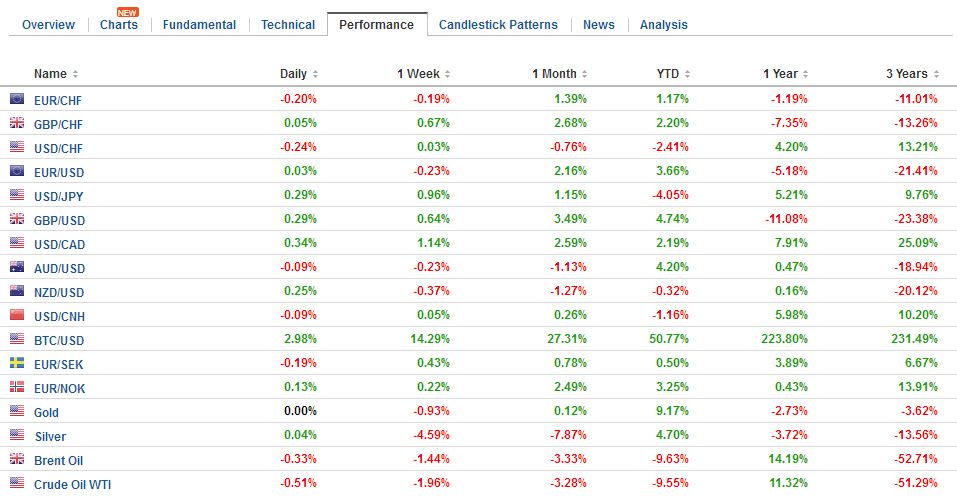

FX Performance, May 02 - Click to enlarge |

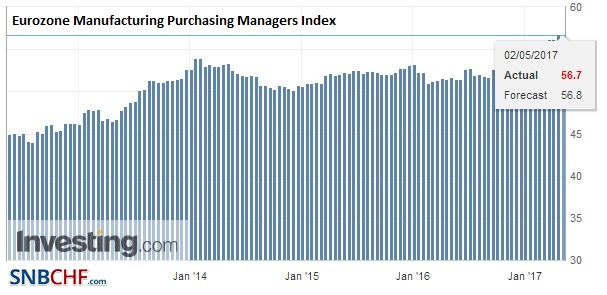

EurozoneThe eurozone manufacturing PMI ticked down to 56.7 from 56.8 flash reading and 56.2 in March. It is a new multi-year high, helped by employment and order backlog. |

Eurozone Manufacturing Purchasing Managers Index (PMI), April 2017(see more posts on Eurozone Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

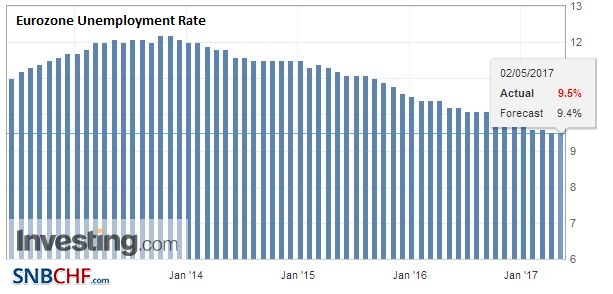

| However, the survey data has been running ahead of real sector performance. Last week, the US, UK, and France reported Q1 17 GDP estimates and each was below expectations. The eurozone reports its estimate tomorrow. The Bloomberg median calls for a 0.5% increase, which would leave the year-over-year pace steady at 1.7%. We note that the despite the increase in the employment sub-component to its best level in six years, the region’s overall unemployment rate in March disappointed by being unchanged at 9.5%. That said, a year ago it was at 10.2%. |

Eurozone Unemployment Rate, April 2017(see more posts on Eurozone Unemployment Rate, ) Source: Investing.com - Click to enlarge |

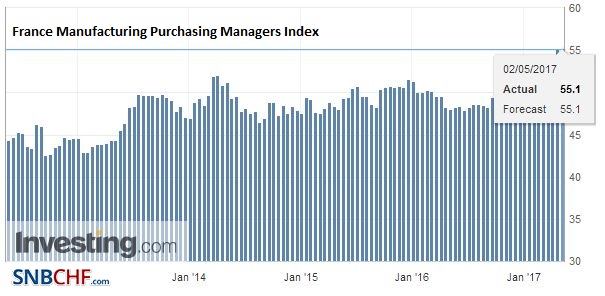

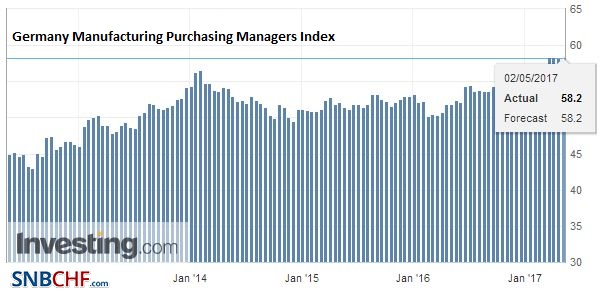

FranceThe French and German readings were unchanged from the flash estimate. It’s reading of 56.2 was a little above expectations and above March’s 55.7. It is also a new multi-year high. |

France Manufacturing Purchasing Managers Index (PMI), April 2017(see more posts on France Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Germany |

Germany Manufacturing Purchasing Managers Index (PMI), April 2017(see more posts on Germany Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

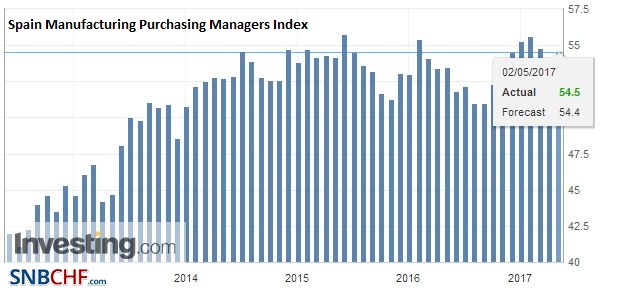

SpainSpain’s manufacturing PMI rose to 54.5 from 52.9. It snapped a two-month decline. |

Spain Manufacturing Purchasing Managers Index (PMI), April 2017(see more posts on Spain Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

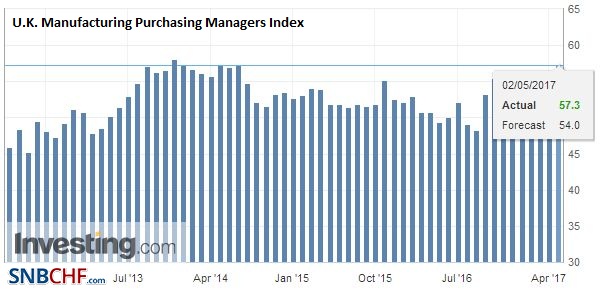

United KingdomThe UK surprised with an exceptionally strong manufacturing PMI. It rose to 57.3 from 54.2 and is the highest in three years. Most expected a slightly softer report. Forward-looking new orders rose to 60.7 from 56.1, which is its best showing since January 2014. The BOE meets next week, and it will likely put more emphasis on the services reading. Last week, the UK reported Q1 GDP of 0.3%, which disappointed. |

U.K. Manufacturing Purchasing Managers Index (PMI), April 2017(see more posts on U.K. Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

Greece

Lastly, we note that Greece and the official creditors appear to have reached a tentative agreement. Greece has to approve a few concessions, including another pension cut and increase in the tax-free threshold, and open more shops on Sunday in order to get another payment for which it turns over the bulk of which to the official creditors. Again, we are struck by who is really being bailed out, and without debt relief, it is the creditors, not debtors. And as if to drive the point home, Markit noted that all the EMU countries it surveys for the PMI showed an increase in manufacturing but Greece. The IMF still is not participating with fresh funds, though the German and Dutch parliaments seemed to have its participation as key criteria.

United States

The US reports auto sales figures today. A strong recovery from the weather-depressed March pace (16.53 mln) is expected, with domestic producers gaining market share. The FOMC meets tomorrow, and it is expected to be uneventful. The ADP jobs estimate will also be reported tomorrow. It was off by a mile last month, and this may dampen interest in tomorrow’s report.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,$JPY,EUR/CHF,Eurozone Manufacturing PMI,Eurozone Unemployment Rate,France Manufacturing PMI,FX Daily,Germany Manufacturing PMI,newslettersent,Spain Manufacturing PMI,U.K. Manufacturing PMI