Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Jonathan Watson

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitter

Swiss Franc |

EUR/CHF - Euro Swiss Franc, April 28(see more posts on EUR/CHF, ) - Click to enlarge |

GBP/CHFThe pound to Swiss Franc rate could hit 1.30 very soon as the market gets closer to this important level of resistance that could easily break through in the coming weeks. The overall expectations for the pound to strengthen on the back of a strong UK election for the Conservatives remain, the Franc should weaken as we get some news of who is the next French President. I personally doubt that Marine Le Pen will win but we might see some problems and weakness from the situation that could strengthen the Franc. The uncertainty around the French election is seeing a stronger Franc which is not helping Swissie buyers! Overall expectations for the pound to slide have not manifested too much today even with UK GDP coming in lower. Overall expectations for the Franc are for the pound to continue to rise particularly if Theresa May wins. I, therefore, believe that the next few weeks could see a volatile period for GBPCHF exchange rates as we get the results of the UK and French election. More than likely a deal over 1.30 is possible in the coming weeks as we get closer to certainty for the UK and also a relief rally on the Franc. The Swiss Franc will weaken once a French election finishes if Macron wins as it a risk negative event. Macron is seen as the safe candidate for European politics and as the Swissie is a safe haven currency, the currency would weaken as we learn that for now, Europe is safe from the more nationalistic tendencies that have sprouted in recent years, that threaten the European ideals to their core. Most commentators believe that the pound will rally after the UK election so if you need to buy sterling with Francs, moving sooner rather later. |

GBP/CHF - British Pound Swiss Franc, April 28(see more posts on GBP/CHF, ) - Click to enlarge |

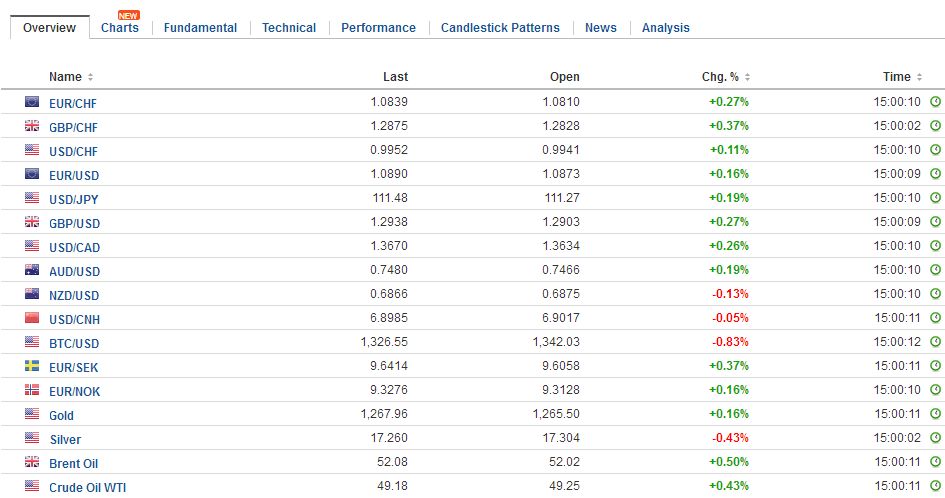

FX RatesEquity markets are stalling into the end of the month. MSCI Asia-Pacific Index is snapping a six-day advance, and the week’s gain was sufficient to extend the advancing streak for the fourth consecutive month. The Dow Jones Stoxx 600 is trading off for the second consecutive session, after rallying for six consecutive sessions. Its 2.4% rally this week ensures a higher close for the month. This European benchmark has risen for three consecutive months and five of the past six. The S&P 500 has gained 1.1% so far this month, coming into today’s session. Last month the S&P 500 slipped 0.4%, which broke a three-month advance. Bonds also rallied this month. The US 10-year yield is off 12 bp, with Gilts off 10 bp, and the Bund yield down six bp. On the month, French premium narrowed about four basis points. The 10-year JGB yield slipped almost five basis points to almost zero. Italy is the only major bond market to see rising yields. Fitch downgraded Italy last week (to BBB). Note that the PD has an open primary this weekend. Renzi is expected to win, after the left-wing and some old guard broke away from the PD. The dollar is consolidating in narrow ranges against the Japanese yen. Today’s range is about a third of a yen above JPY111.00, and inside yesterday’s range, which was inside Wednesday’s range. The dollar has been resilient even though US 10-year Treasury yields are struggling to re-establish a foothold above 2.30%. Yen sales against sterling and the euro may have bolstered the greenback’s resilience. |

FX Daily Rates, April 28 - Click to enlarge |

| The US dollar is mixed on the day. On the month, the dollar has risen against most currencies except, sterling and the euro (and the Danish krone). The dollar-bloc currencies fell out of favor this month, and are off around 2%. Sterling is the best performer, with the surprise election announcement a major prop.

The euro rallied toward the week’s high, but since the sharply higher opening on Monday, after the first round of the French elections, the euro has chopped around same cent range of $1.0850-$1.0950. Recall the $1.0935 area corresponds to the 61.8% retracement of the euro’s decline since the US election last November. And $1.0980 is the 50% retracement objective of the decline from last year’s high near $1.1615. Large option strikes at $1.09 (1.8 bln euros) and $1.0950 (2.4 bln euros) roll-off later today. Canada reports February GDP (expected to have risen by 0.1%). The weekend sees the EU summit on Brexit. Reports suggest the EU may press for considering a united Ireland within the EU. Merkel’s speech earlier this week underscores the EU’s interest in first agreeing to the terms of exit before a new, even if temporary, arrangement, can be made. Also, ASEAN countries hold a summit as well. Sterling shrugged off the news and is making new highs since early last October. It approached $1.2960. The $1.30 area is of psychological importance, but chart-based resistance is seen in the $1.3050-$1.3070 area. It may require a break of $1.2860 on the downside to stymie the bulls. |

FX Performance, April 28 - Click to enlarge |

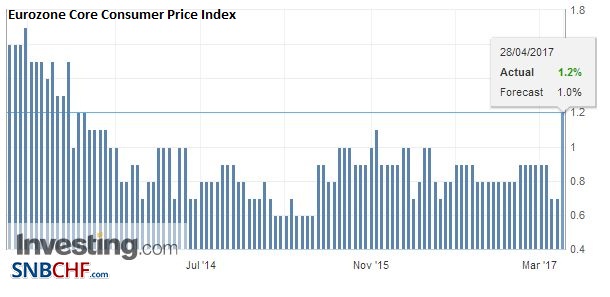

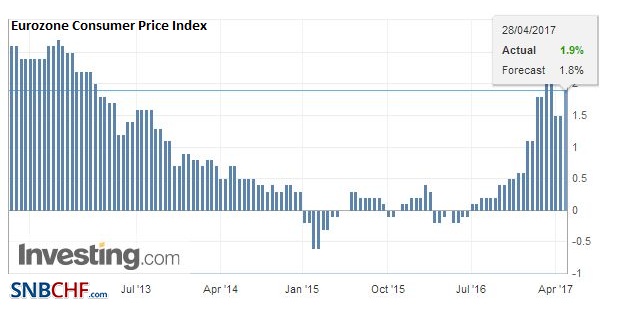

EurozoneThe main exception to this generalization is the eurozone preliminary April CPI. It was much stronger than expected. The headline rose to 1.9% from 1.5%, and the core rate jumped to 1.2% from 0.7%. Draghi was upbeat about the region’s growth, which he seemed to acknowledge was mostly based on survey data. He was less sanguine on inflation, and due to the distortions with the April CPI, the May figures will be awaited for a cleaner read. The next ECB meeting is on June 8, and new staff forecasts will be available. |

Eurozone Core Consumer Price Index (CPI) YoY, April 2017 (flash)(see more posts on Eurozone Core Consumer Price Index, ) Source: Investing.com - Click to enlarge |

| The data appears to have been flattered by calendar effect of Easter, and trip packages, for example, are included in the core. It is the highest level since mid-2013. The CPI report followed news of a stronger gain in M3 than expected, and an improvement in lending to both households and non-financial businesses.

The month-end and what for many in Europe and Asia will be a long holiday weekend with May Day celebrations and the bank holiday in the UK at the start of next week. Perhaps that could help explain the subdued market reaction to a series of economic reports. |

Eurozone(see more posts on Eurozone Consumer Price Index, ) Source: Investing.com - Click to enlarge |

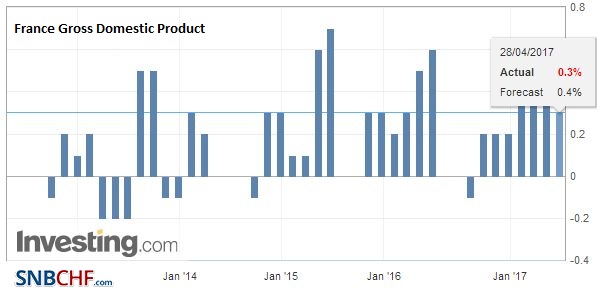

FranceHowever, as we have noted, it appears the survey data is running ahead of actual activity. This concern materialized today. France reported a 0.3% expansion in Q1 17, which was a little softer than expected, weighed down by a 0.7% decline in net exports and household spending that practically stagnated. That said, Q4 16 growth was revised higher. |

France Gross Domestic Product (GDP) QoQ, Q1 2017(see more posts on U.K. Gross Domestic Product (QoQ), ) Source: Investing.com - Click to enlarge |

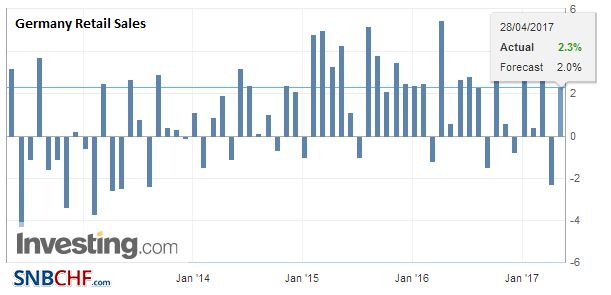

Germany |

Germany Retail Sales YoY, March 2017(see more posts on Germany Retail Sales, ) Source: Investing.com - Click to enlarge |

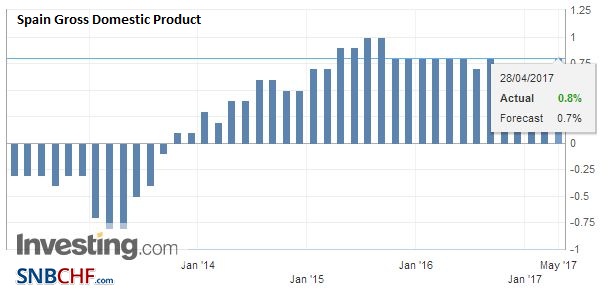

Spain |

Spain Gross Domestic Product (GDP) QoQ, Q1 2017(see more posts on Spain Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

Spain Gross Domestic Product (GDP) YoY, Q1 2017(see more posts on Spain Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

|

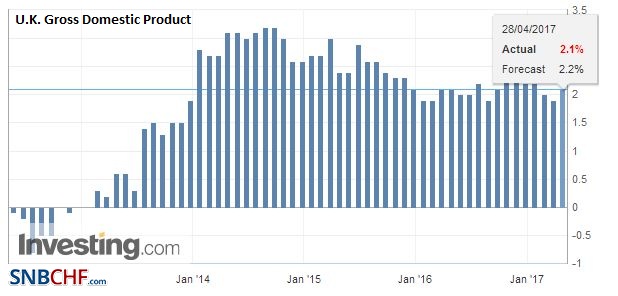

United KingdomThe UK also disappointed. The economy expanded by 0.3% in Q1. It is the weakest growth in a year. Services grew by 0.3%, their poorest showing in nearly two years. Industrial output rose 0.3%, arguably helped by stronger exports and a weak pound. Manufacturing output rose 0.5%. Construction rose a more modest 0.2%. Separately, the UK reported that mortgage approvals and consumer credit growth slowed in March. |

U.K. Gross Domestic Product (GDP) YoY, Q1 2017(see more posts on U.K. Gross Domestic Product, ) Source: Investing.com - Click to enlarge |

United StatesThe US reports Q1 GDP. The median forecast in the Bloomberg survey is for a 1.0% annualized gain. We suspect the risk is on the downside. Beginning in 2010, Q1 growth in the US has averaged 1.1%, but our back of the envelope calculation warns that Q1 17 was likely weaker than average. Outside of the headline shock, it has no implications for monetary policy. The Federal Reserve hiked rates in March, rendering Q1 data moot. The FOMC meets next week, and the statement is likely to look past the setback in Q1. The US jobs report at the end of next week may be of greater importance than the FOMC meeting.

|

U.S. Gross Domestic Product (GDP) QoQ, Q1 2017(see more posts on U.S. Gross Domestic Product QoQ, ) Source: Investing.com - Click to enlarge |

| The US also sees the Chicago PMI for April. |

U.S. Chicago Purchasing Managers Index (PMI), April 2017(see more posts on U.S. Chicago PMI, ) Source: Investing.com - Click to enlarge |

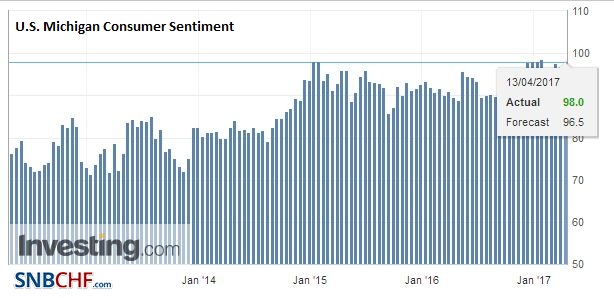

| The final University of Michigan consumer confidence and inflation expectation survey. It is important that the US Congress approves a spending authorization bill or some stop gap measure. Otherwise, government closure cannot be ruled out. Separately, although press reports suggest progress on health care, a resolution still seems elusive. To appease the wing of the Republican Party (Freedom Caucus) that blocked the previous attempt appears to be alienating the moderate wing (e.g. Tuesday Group). |

U.S. Michigan Consumer Sentiment, March 2017(see more posts on U.S. Michigan Consumer Sentiment, ) Source: Investing.com - Click to enlarge |

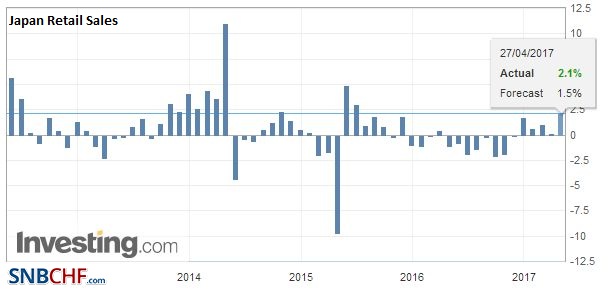

JapanJapan’s end of the month data dump shows many expect the BOJ to lag behind the ECB. March CPI was a touch softer than expected at 0.2%, and the core rate was steady at 0.2%. However, excluding food and energy, CPI slipped back into negative territory (-0.1% vs. 0.1%). Although retail sales ticked up in March (0.2%). |

Japan Retail Sales YoY, March 2017(see more posts on Japan Retail Sales, ) Source: Investing.com - Click to enlarge |

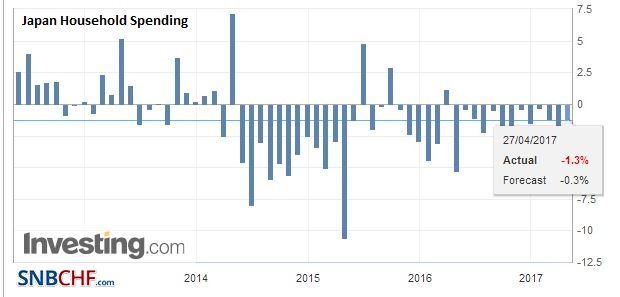

| Overall household spending disappointed. It fell 1.3% year-over-year, which was more than twice the expected pace, though not as deep as the decline in February. Industrial output was also weaker than expected, falling 2.1% in March, which gives back more of February’s 3.2% gain than expected. The median expectation was for a 0.8% decline. Lastly, unemployment was unchanged at 2.8%, though the jobs-to-applicant ratio increase to 1.45 from 1.43. |

Japan Household Spending YoY, Q1 2017(see more posts on Japan Household Spending, ) Source: Investing.com - Click to enlarge |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,EUR/CHF,Eurozone Consumer Price Index,Eurozone Core Consumer Price Index,France Gross Domestic Product,FX Daily,gbp-chf,Germany Retail Sales,Japan Household Spending,Japan Retail Sales,newslettersent,Spain Gross Domestic Product,U.K. Gross Domestic Product,U.K. Gross Domestic Product (QoQ),U.S. Chicago PMI,U.S. Gross Domestic Product QoQ,U.S. Michigan Consumer Sentiment