Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, April 12(see more posts on EUR/CHF, ) - Click to enlarge |

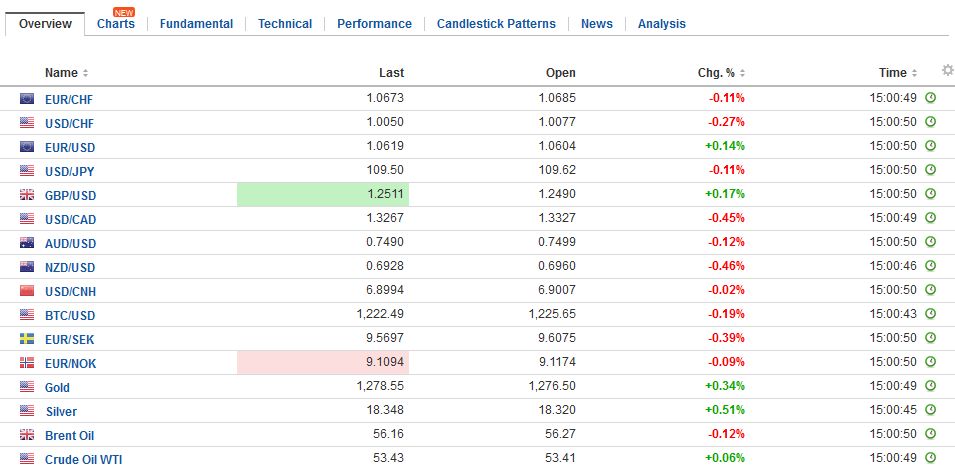

FX RatesMarkets are calmer today. The significant movers yesterday have stabilized. The dollar has been unable to resurface above JPY110, but after plumbing to new lows near JPY109.35 in Asia, the dollar has recovered back levels since in North America late yesterday. The decline in the US 10-year yield was also initially extended in Asia before stabilizing and returning to levels seen in the US afternoon. Consistent with theme, the Korean won and the local stock market snapped a six-day decline and posted small gains on the session. After moving to its highest level since last November, gold has reversed earlier gains and is now slightly lower on the day. |

FX Daily Rates, April 12 - Click to enlarge |

| The MSCI Asia Pacific Index eased for the first time in four sessions. European stocks are firmer for the first time this week, with the Dow Jones Stoxx 600 up about 0.5% in late morning turnover. Many European centers will be closed for the Easter holiday. Full liquidity is not expected to return until after Easter Monday.

The $1.2520 area for sterling corresponds to a recent trend line drawn off late March and early April highs. Initial support is seen in ahead of $1.2470. For its part the euro, is trading within yesterday’s range. Breaks of the $1.06 level did not seem to spark selling as much as bottom picking buying. The dollar-bloc currencies continue to under-perform as they did yesterday. |

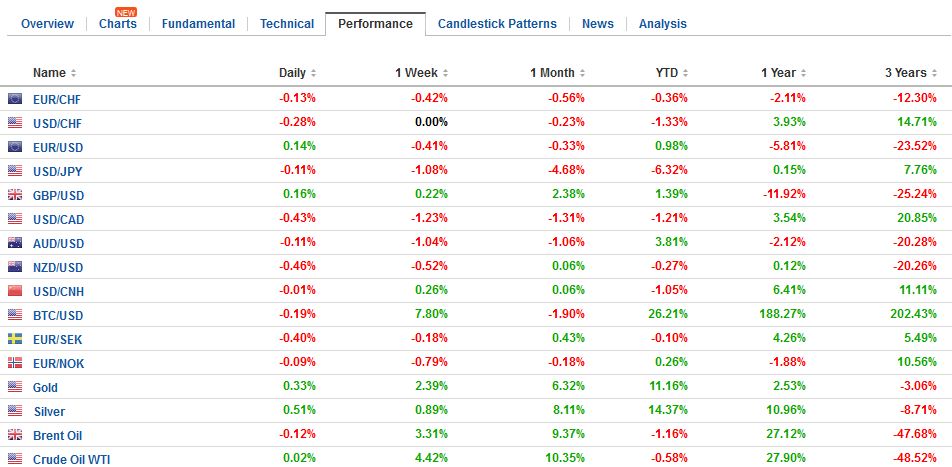

FX Performance, April 12 - Click to enlarge |

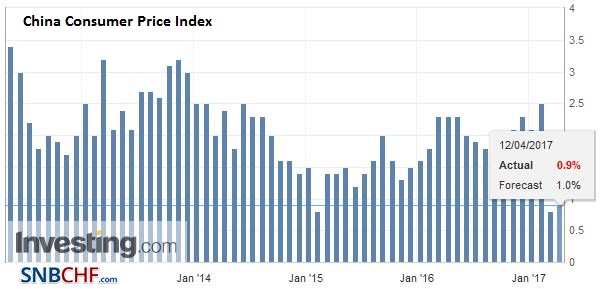

ChinaThere have been two economic reports of note today. The first is China’s inflation. The fall in various food prices is helping keep consumer prices stable. Consumer prices rose 0.9% year-over-year in March after a 0.8% rise in February. |

China Consumer Price Index (CPI) YoY, March 2017(see more posts on China Consumer Price Index, ) Source: Investing.com - Click to enlarge |

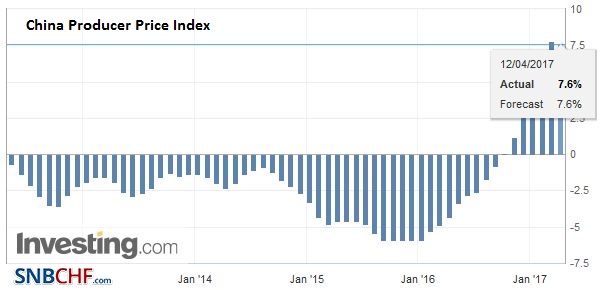

| Producer prices moderated to a 7.6% year-over-year pace from 7.8%. The surge in China’s producer prices appears nearly over as some moderation is already evident. Iron ore prices that surged earlier this year have come off the boil and have declined more than 20% from the recent high, including more than 3% today. |

China Producer Price Index (PPI) YoY, March 2017(see more posts on China Producer Price Index, ) Source: Investing.com - Click to enlarge |

United KingdomThe second economic report was the UK labor market update. Sterling popped to session highs near $1.2520 apparently on the back of somewhat firmer earnings growth than had been expected. The other details, however, were a bit disappointing. The claimant count rose 25.5k, the most in about 5 1/2 years. The 12-month average was slightly negative before today’s report. Employment growth slowed, though the ILO unemployment rate was unchanged at 4.7%. |

U.K. Unemployment Rate, February 2017(see more posts on U.K. Unemployment Rate, ) Source: Investing.com - Click to enlarge |

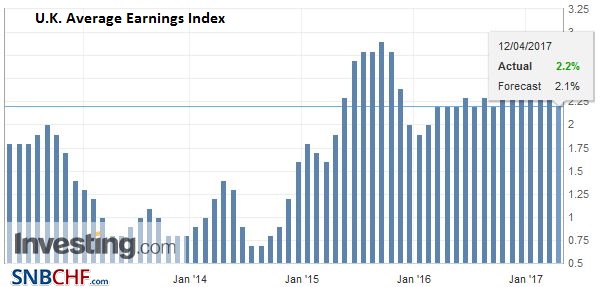

| The average weekly earnings was unchanged at 2.3% after the January series was revised to 2.3% from 2.2%. Excluding bonus payments, average weekly earnings eased to 2.2% from a revised 2.4% (initially 2.3%). |

U.K. Average Earnings Index, February 2017(see more posts on U.K. Average Earnings Index, ) Source: Investing.com - Click to enlarge |

Spain |

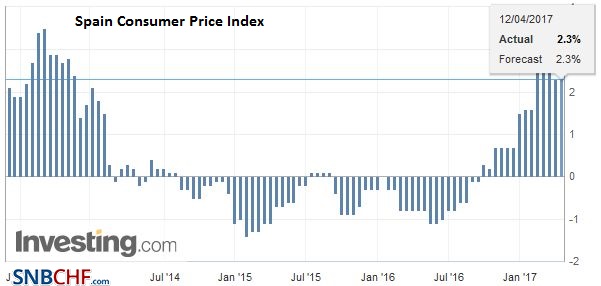

Spain Consumer Price Index (CPI) YoY, March 2017(see more posts on Spain Consumer Price Index, ) Source: Investing.com - Click to enlarge |

United States

The US Treasury is expected to issue its semiannual report on the foreign exchange market later this month. Despite Trump campaign promises to cite China as a currency manipulator, we have suggested that Treasury Secretary Mnuchin is unlikely to do so at the first formal opportunity. China simply does not meet the criteria that have been developed. Its current account surplus is smaller than 3% of GDP. It was about 1.8% of GDP last year. Its reserves have been falling (though they have edged higher in the last two months) as the PBOC sought to moderate the yuan’s decline.

Late yesterday, President Trumps top outside adviser, Schwarzman, the Chairman of Blackstone lent credence to our suspicions by confirming that the Treasury Department probably won’t cite China as a manipulator. Recall that in the last report, China and five other countries were cited as having unfair practices, though not reaching the threshold of manipulation. Recall that if a country is found to be manipulating its currency, the first consequence is that bilateral talks are necessary. Well, it turns out Japan and China have already agreed to talks. That said, no country has been formally accused of manipulation since 1994 and this length of time itself turns it into an important symbolic threshold.

Canada

Today’s Bank of Canada meeting is the only major central bank that meets in this holiday-shortened week. For all practical purposes, there is no risk that the Bank hikes rates. The focus is on its forward guidance. Recall that Governor Poloz previously revealed that a rate cut was considered in January. We anticipate that one of the most important developments will be that this easing bias is removed. Since the middle of last year, Canada is the fastest growing G7 country. Although Q1 17 GDP has not been released, conservative assumptions suggest it was the third consecutive quarter of annualized growth in excess of 3%.

There are a few elements that may determine how the market perceives the forward guidance. First, is the distribution of growth. If 2017 growth is lifted from the 2.1% official estimates, is it offset by downgrading 2018 growth by a similar amount? Second, when will the output gap be closed?

The Bank’s current forecast is for the output gap to close in the middle of 2018. We suspect officials may be reluctant to bring it forward, as it would spur speculation of a rate hike. Some derivative market indications suggest the odds of a rate hike this year have nearly doubled to approach 45% in response to the spate of strong jobs and robust economic activity. Housing permits and starts are particularly strong, with March starts near the highest level since before the crisis. However, with the federal government contemplating macro-prudential curbs, the central bank may not want to encourage speculation of a rate hike. Some may fear that rate hike speculation that strengthens the Canadian dollar would serve as another headwind to the disappointing non-energy exports.

Governor Poloz seems particularly sensitive to the risks for which there are plenty. The chief risks may emanate from the Washington’s policy uncertainties. Trade and tax policies have not crystallized. However, it is easier to foresee negative rather than positive shocks. The prospect of the border adjustment tax would be such a shock, and the central bank cannot look past this yet. Even if there is a one-in-three or a one-in-four chance of a border adjustment being imposed, the odds-adjusted impact would still be severe.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,$TLT,Canada,China Consumer Price Index,China Producer Price Index,EUR/CHF,newslettersent,Spain Consumer Price Index,U.K. Average Earnings Index,U.K. Unemployment Rate