Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The macroeconomic fundamentals have not changed much in the first three months of the year. The US growth remains near trend, the labor market continues to improve gradually, both headline and core inflation remain firm, and the Federal Reserve remains on course to hike rates at least a couple more times this year, even though the market is skeptical. The uncertainty surrounding US fiscal has not been lifted, and it may not be several more months.

Europe is growing perhaps a little quicker than a trend, but price pressures remain subdued. The preliminary March core CPI reading underscores the ECB’s conclusion that inflation has yet to be put on a stable path toward the target. While a move away from the negative deposit is understood to be beneficial to European banks, it seems premature to expect a change in rates in the coming months.

The Japanese economy appears to be finding some traction, but it is narrowly based, and household consumption remains poor. There is no price pressure of which to speak. There is no pressure on the Bank of Japan to change monetary policy.

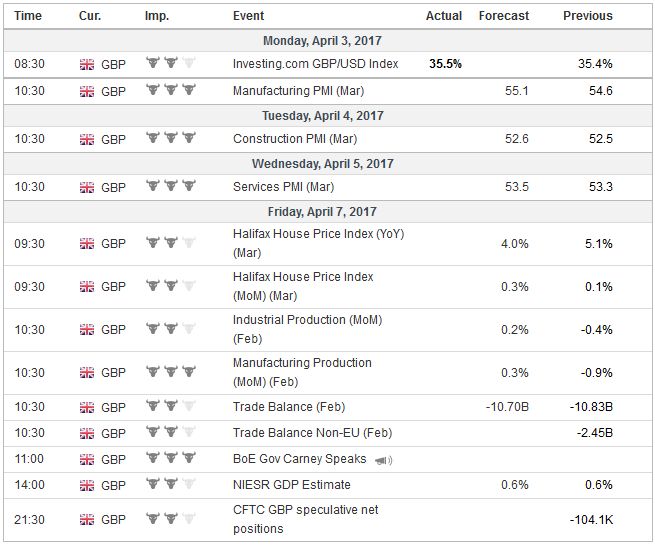

United KingdomAfter nine months since the UK’s referendum, Article 50 of the Lisbon Treaty has been triggered. At this juncture, it was an important formality but a formality nonetheless. There will be much jockeying for position, feints, and parries, and investors need to look past the noise and remain focused on the signal. The signal is still a function of macroeconomics and market positioning. Although there has been a dramatic adjustment of speculative positioning in the futures market for euros, sterling positioning has hardly adjusted. The UK economy remains resilient, though it is expected to slow. Price pressures may not have peaked, but without stronger wage growth, the impact from the past decline in sterling and rise in oil prices will dissipate. |

Economic Events: United Kingdom, Week April 03 - Click to enlarge |

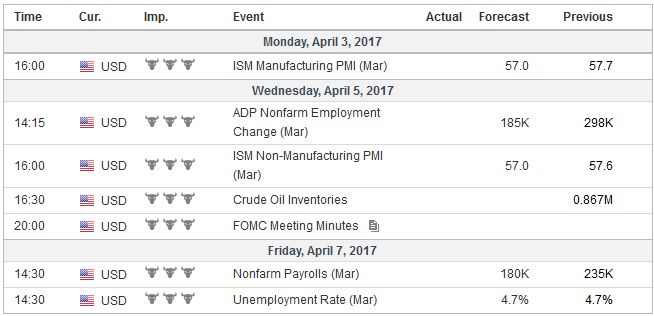

United StatesUS non-farm payrolls are often the single most important economic report in the US monthly data cycle. After two months of jobs growth in excess of 200k a month, a reversion to the mean seems likely. It may have been hinted by the increase in weekly jobs claims. Payback may come from manufacturing and construction sectors, which have been particularly strong. However, provided that job growth does not collapse, but simply returns to trend, it ought not impact expectations for Fed policy. A June hike still seems to be the most likely scenario. The minutes from the March FOMC meeting will be released. The minutes often have a high noise to signal ratio as voters and non-voters voices are included, and the important views of the of the leadership are obscured. The Federal Reserve publish the confidence intervals (fan lines) around their projections. Once introduced, the dot plot cannot be discontinued, but it can be softened, which is precisely what the confidence intervals will accomplish. The end of the week features the US, and Chinese Presidents have their first face-to-face meeting. Trump has toned down the bellicose rhetoric in which he accused China of “raping” America, threatened to abandon the one-China policy, and citing China as a currency manipulator “on day one.” China seems to have made a few concessions. It has banned coal imports from North Korea, and the US had long wanted China to do more to rein in its ally. It has also granted Trump a little more than three dozen trademarks, including, according to the Guardian, an escort service. |

Economic Events: United States, Week April 03 - Click to enlarge |

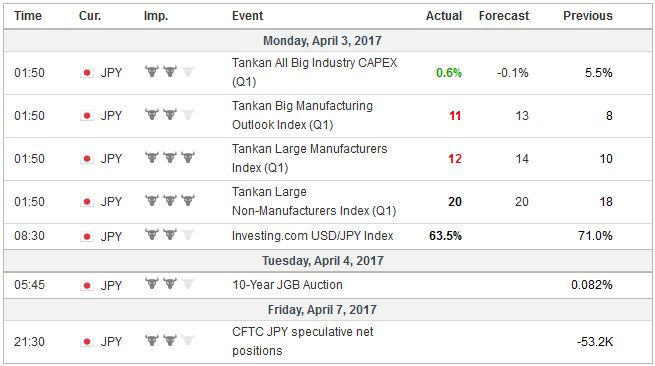

JapanWhen Japanese Prime Minister Abe visited President Trump recently, the two agreed to trade talks to be led by the US Vice President Pence and Japanese Finance Minister Aso. This may very well serve as the template for the US and China. Such talks, incidentally, are also similar to part of the consequences of the US Treasury finding a country guilty of currency manipulation. That report is due later in the month, and given the current criteria, China is unlikely to be cited. Also, President Xi may announce some new commercial activity and purchases of US goods, which is part of China’s modus operandi. The Senate confirmation of a Supreme Court Justice hardly seems to be an issue for investors, but it is important now. Trump enjoys a slim majority in both houses. A key strategic choice is whether to seek greater control of the Republican Party, which like all modern parties, is a coalition, or seek support from moderate Democrats. To overcome a filibuster over Gorsuch’s nomination, it is possible that the Republicans in the Senate modify the rules to allow a simple majority for judicial appointments. Such a maneuver would antagonize the Democrats and make cooperation more difficult on other parts of the Trump Administration’s agenda. |

Economic Events: Japan, Week April 03 - Click to enlarge |

EurozoneIn the eurozone, survey data has been running ahead of real sector data. German industrial output likely fell, though there was a little sign from the PMI. The final March PMI may slip. February retail sales are expected to soften. The unemployment rate may ease to 9.5% from 9.6%. It peaked a little above 12%. These real sector reports are of little significance in the current environment. The key is the reaction function of the European Central Bank, and it is not presently about the real sector, but prices. The weaker than expected preliminary March CPI report dealt a blow to the hawks, who seemingly had been pressing to begin the exit from the unorthodox policies even before the asset purchases are complete. The record of the recent ECB meeting will be released, and it will likely show that the hawks remain in a small minority. The divergence between the surveys and real sector data is also evident in Sweden and Norway. The March manufacturing PMI in Sweden may ease from a heady 60.9 reading in February, but industrial output likely fell around 0.5% in February. Norway’s manufacturing output may edge higher March, but manufacturing output likely also fell 0.5% in February. |

Economic Events: Eurozone, Week April 03 - Click to enlarge |

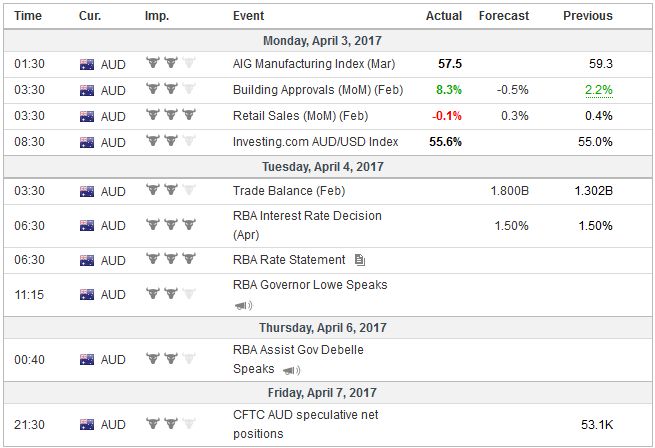

AustraliaThe Reserve Bank of Australia is the only major central bank to meet in the first week of April. There is little chance of a change in policy. There has been very little change since the last meeting. The government has tightened mortgage issuance rules, which may reduce an obstacle that the central bank may see in its way if it wanted to ease policy. |

Economic Events: Australia, Week April 03 - Click to enlarge |

CanadaCanada will also report March jobs data at the end of the week. It has grown 254k jobs in the past seven months, and nearly all were full-time positions. While other high frequency data have been robust, the pace of job growth is simply not sustainable. Interest rate differentials, the underlying direction of the US dollar, and perhaps, oil prices, seem more important for the Canadian dollar’s direction than the jobs data. In broad strokes, we expect US interest rates to stabilize and turn higher. There has been a powerful adjustment to the net speculative position in US 10-year note futures. The Commitment of Traders data suggests that the decline in yields has been a function of bottom pickers establishing new longs, while short-covering has been minimal. With the help of a rebound in oil prices, and the likely reacceleration of growth (January-March growth has averaged 1.1% beginning in 2010, while the other quarters grow 2.5% on average), a reduced safe haven bid as angst over the French presidential election eases, firmer interest rates will likely lend the dollar better support in Q2 than in Q1. |

Economic Events: Canada, Week April 03 - Click to enlarge |

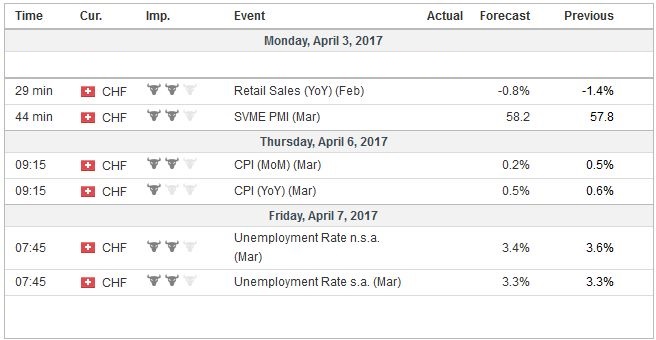

Switzerland |

Economic Events: Switzerland, Week April 03 - Click to enlarge |

Tags: #USD,$CNY,China,ECB,FOMC,Interest rates,jobs,newslettersent,US