Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Swiss Franc |

EUR/CHF - Euro Swiss Franc, March 06(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe US dollar’s pre-weekend pullback was extended in early European turnover but appeared to quickly run out of steam. The prospect of a constructive US employment report at the end of the week, especially given the steady decline in weekly initial jobless claims to new cyclical lows, underscores the likelihood that the Fed hikes rates next week. Bloomberg puts the odds above 90%, while the CME estimates a nearly 80% chance. The euro briefly pushed above the highs from late February near $1.0630 (and reached a high of $1.0640) before being sold back below $1.06. There are two main European talking points today. First, there is some speculation that the ECB could change its forward guidance this week. It has been saying that rates will remain at present levels or lower “for an extended period of time” beyond the asset purchase program. With headline inflation throughout the area rising, and growth solid, there is some thought that this guidance needs to be modified. We expected Draghi to forcefully push against this. Core inflation is flat in the trough and surge in inflation is likely to begin unwinding in Q2, and the especially in H2, has last year’s recovery in energy prices fall out of the base effect. |

FX Daily Rates, March 06 - Click to enlarge |

| Second, there were ideas that France’s Fillon would drop out of the presidential contest, and perhaps replaced by Juppe, who would likely shoot into second place behind Le Pen. However, Fillon is trying to hold on, while Juppe made it clear he will not stand. This encouraged some new euro sales, which pushed the single currency back below $1.06. The $.10585 area is the 38.2% of the euro’s recovery from last week’s dip below $1.05. The 50% retracement is near $1.0565 and the 61.8% retracement is $1.0650.

The pullback in US Treasury yields, and especially with the 2.50% level holding on a closing basis, weaker Japanese shares, and North Korea’s missile test helped support the Japanese yen. The dollar was sold to a three-day low near JPY113.55, meeting the 38.2% retracement of gains since JPY11.70 was tested on February 28. The 50-% retracement is near JPY113.25, which corresponds to the 20-day moving average. |

FX Performance, March 06 - Click to enlarge |

AustraliaAustralia reported that January retail sales rose 0.4%, in line with expectations. The RBA meets first thing Tuesday and is widely expected to keep policy steady. The trade-weighted index has risen 4-5% this year, and the central bank would like a weaker currency. The sharp improvement in terms of trade (rising iron ore and coal prices) appear to largely run their course. The Australian dollar was sold through $0.7600 last week for the first time since the end of January. It snapped back just before the weekend to test the old floor. The gains were extended to $0.7610 before encountering selling pressure. Initial support is seen in the $0.7570 area now. |

Australia Retail Sales, February 2017(see more posts on Australia Retail Sales, ) Source: investing.com - Click to enlarge |

EurozoneCore 10-year benchmark yields are mostly softer, though peripheral yields and French yields are higher. Premiums over Germany are widening at both the two- and 10-year tenors. Of note, the Netherlands, which goes to the polls next week, is seeing its yields slip more in line with Germany than France. The latest polls suggest that the populist-nationalist party led by Wilders has lost some momentum in recent days. |

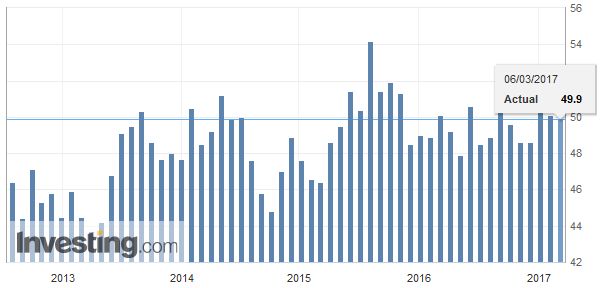

Eurozone Retail PMI, February 2017(see more posts on Eurozone Retail PMI, ) Source: Investing.com - Click to enlarge |

Japan

Japanese shares traded heavily for the second consecutive session, but the MSCI Asia Pacific Index resisted the drag and finished 0.4% higher. Korean shares, which had also fallen at the open, recorded to close marginally higher. European shares are mostly lower as well, with the Dow Jones Stoxx 600 off about 0.4% as well. Energy, information technology, and materials are leading the downside.

United Kingdom

There had been some speculation that UK Prime Minister May could trigger Article 50 this week. However, need to reconcile the amendment passed by the House of Lords with the House of Commons (so-called ping-pong) may see at least a week delay. Such a delay will keep the focus on the Hammond’s budget at midweek. Reports suggest he will seek a fiscal cushion to absorb some dislocation caused by Brexit, but also that he will seek a balanced budget over the next parliament.

Sterling barely extended the pre-weekend recovery and was turned lower near $1.23 which was the high since the $1.24 support broke in the middle of last week. Last week’s low was set near $1.2215 but is finding support above there today. Sterling’s late gains before the weekend snapped a five-day slide, during which time it lost five cents.

Although the interest rate differential between the US and Japan and between the US and Germany are well tracked, we note that the interest rate differential between the US and UK is also at extremes. The 10-year spread of nearly 130 bp is the widest since at least the 1980s, and the two-year spread of 120 bp is the largest since at least the early 1990s.

Canada

The Canadian dollar recovered before the weekend to snap a four-day slide. However, the US dollar remains firm and continues to straddle the CAD1.34 area. The greenback found a bid near CAD1.3365, a little below the pre-weekend low.

The North American session features the January factory orders and the final durable goods reports. The main focus this week is on the US jobs report with the ADP estimate on Wednesday and the national report at the end of the week. The early estimate has crept up and now stands at 190k, according to the median in the Bloomberg survey. From a larger perspective, recall that the US economy typically underperforms in Q1 and many economists are looking for a soft report (though near trend growth, which Yellen confirmed may be a little below 2% currently).

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,Australia Retail Sales,EUR/CHF,Eurozone Retail PMI,newslettersent