Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Trump has moderated in several areas, he is being checked in others, and less impactful in others.

This will underscore the focus on Yellen’s testimony this week.

At same time, many will be reluctant to short the dollar ahead of the tax reform plans that may be unveiled in Trump’s upcoming speech to Congress.

There is a lull in the maelstrom launched by the Trump Administration. His ban on immigrants from seven of the ten Muslim-majority countries in the Middle East has been stymied by the judicial system that has emerged as a check on the assertion of executive authority but is on its way to the Supreme Court. He backed off after goading China by threatening to recognize Taiwan.

After accusing Japan of manipulating its currency, Trump reportedly did not broach the topic with Prime Minister Abe in their meeting before the weekend. The Administration also eased some concerns by underscoring its commitment to NATO, despite Trump’s claim it was obsolete. Contrary to earlier reports, the US apparently has agreed to continue sanctions against Russia associated with the aggression in Ukraine. After seemingly encouraging a more aggressive Israel, President Trump warned that its construction efforts on the West Bank were not helpful for peace.

Not only did Trump move back toward more traditional positions, but he also threw investors a bone. Investors and businesses have been eager for more details on the President’s economic agenda. After meeting with airline executives, Trump announced that “phenomenal” tax reform was a few weeks away. This seemed to be just what some investors wanted to hear, and the major equity indices were goosed to new record highs, and the US dollar had its best week of the New Year.

At the same time, the President’s tweets may be losing their market impact. The retailer that dared drop his daughter’s clothing line was subject to a critical tweet, and the stock rallied. The Mexican peso, which had dramatically depreciated under a barrage of criticism from Trump staged a recovery. Since January 19, the peso has been the strongest currency in the world.

The prospect of a border adjustment (tax imports and remove taxes on exports) has prompted many classically trained economists to claim that the dollar will automatically appreciate offsetting the import tax. While we retain our long-term constructive outlook for the dollar, we are skeptical of what still strikes us as a naïve understanding of purchasing power parity and a misuse of economic identities. Their case rests on the dollar’s exchange rate being the burden of adjustment. There is an alternative moving part, the general price level. That is to say, the result of the import tax could be higher inflation.

This brings us to Fed’s chief Yellen’s Congressional testimony. There are three main issues. First is the economic assessment. Little has changed since the FOMC statement. The Federal Reserve appears more confident in the resilience of the economy and the continued recovery in price pressures. She is unlikely to pre-commit the central bank to raising rates at any meeting, but will likely reiterate that the commitment to gradually normalizing monetary policy.

Second, she will likely be asked about the Fed’s balance sheet. Several regional Fed Presidents have broached the issue. The official position, as has repeatedly been expressed in FOMC statements, is that when the normalization process is well underway, the balance sheet will be addressed. Yellen will be reluctant to commit to any fixed time frame, maximizing the Fed’s flexibility. She may deign to repeat some general principles, like eventually returning the balance sheet to all Treasury securities. She may offer that the first step would likely be a passively now rolling over maturing issues.

Third, Yellen may be queried about the impact of fiscal policy on monetary policy. However, while there is little doubt that Fed officials are monitoring the progress of the tax proposals in the negotiating process, it still does not reach the threshold of a policy variable yet. It may before the mid-March FOMC meeting when forecasts will be updated.

Given some vitriolic comments by candidate Trump about the Federal Reserve, including using a picture of Yellen (alongside Goldman Sachs’ Blankfein and Soros) in an campaign ad, some investors were concerned about encroachments of the Fed’s independence. We argued that this would not be necessary; that Trump could shape the Federal Reserve through the power of appointment.

The seven-member Federal Reserve Board of Governors has two vacancies, and as we anticipated, Governor Tarullo has indicated plans to retire at the start of Q2. In addition, early next year Yellen’s term as Chair ends, and toward the middle of the year, Fischer’s term as Vice Chair is complete. This means that by the middle of 2018, Trump’s appointees will dominate the Board of Governors.

In the week ahead, there are two general data memes: Inflation and GDP. The US, UK, Switzerland, and China report January CPI. The eurozone and Japan report Q4 GDP. A 0.3% rise in the US headline CPI and a 0.2% rise in the core rate will not prevent the year-over-year rate from slipping a bit due to the base effect. Still, it won’t change the underlying trend.

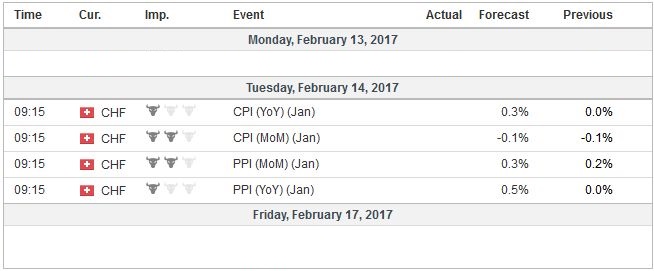

SwitzerlandIn the other countries that report, inflation pressures are set to increase. In the UK, the year-over-year rate is likely to rise from 1.6% in December to 1.9%-2.0% in January. This is still primarily the impact of the rise in energy prices, but the past depreciation of sterling will likely drive it going forward. In Switzerland, deflationary pressures are subsiding. CPI is likely to rise to 0.3% from the flat reading in December. |

Economic Events: Switzerland, Week February 13 - Click to enlarge |

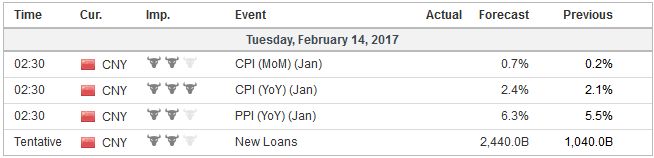

ChinaChina’s inflation is also rising, and the stabilization of the economy may allow officials to turn their attention toward curbing credit growth. Still, the expected January increase to around 2.6% from 2.1% may overstate the case if prices rose ahead of the Lunar New Year. Yet, producer prices continue to accelerate. The year-over-year pace bottomed in last 2015 at -6.0%. It moved above zero last September. Producer prices are expected to have accelerated to a 6.6% pace in January from 5.5% last December. |

Economic Events: China, Week February 13 - Click to enlarge |

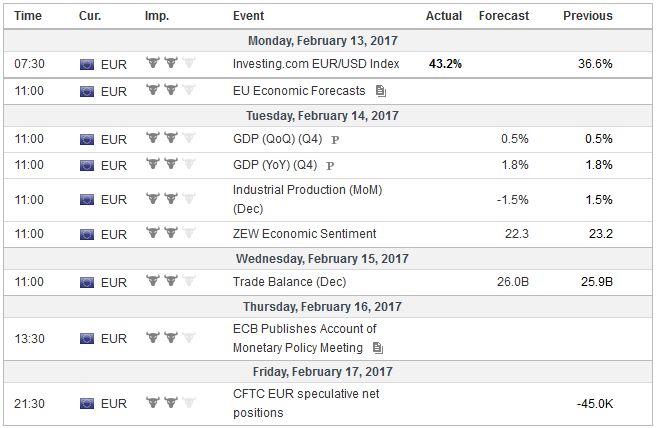

EurozoneSweden’s Riksbank meets on February 15. It is not expected to change policy. However, it is in a bit a quandary. The ostensibly reason for its aggressive unorthodox monetary policy was to arrest deflation, and that meant in part to curb the strength of the krona. Inflation has moved toward 2%, but the krona appreciated about 5.25% on a trade-weighted basis since early November. It has recouped 61.8% of the previous six-month (~7.6%) decline. Industrial output and consumption finished 2016 on a soft note, but the January PMIs’ suggest it was a temporary lull. The euro’s 6.75% decline against the krona is the driver. The central bank may find some consolation that the euro finished last week with two successive closes above its 20-day moving average for the first time since the first half of last November when the cross was SEK9.85 rather than SEK9.49 now (having been down to SEK9.41). Given the political calendar for the eurozone, the krona may not receive the same selling pressure as the euro. Sweden reports the January CPI figures two days after the Riksbank meeting. The optics of a 0.7% monthly decline, which the median expects, may be worse than the reality. Headline CPI has fallen in January for at least the past decade. Due to the base effect, the year-over-year rate would ease, if the median is correct, to 1.5% from 1.7% in December. That was the highest reading in a little more than five years. What Sweden calls the underlying rate, which uses fixed rate mortgages to calculate CPI is expected to slip to 1.7% from 1.9%. |

Economic Events: Eurozone, Week February 13 - Click to enlarge |

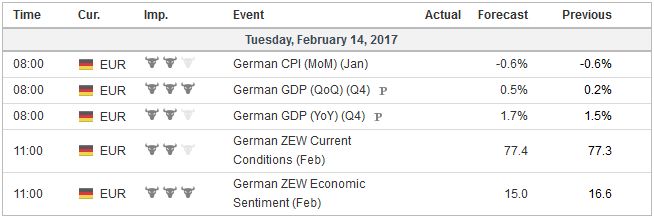

GermanyThere are some downside risks to the initial eurozone’s initial Q4 GDP estimate of 0.5% after the disappointing German industrial output figures. Little appreciated, especially given the divergence of monetary policy, the US and eurozone growth in 2016 may have been the same at 1.6%. For the US, this is a little below trend, while eurozone growth is a little above trend. |

Economic Events: Gernany, Week February 13 - Click to enlarge |

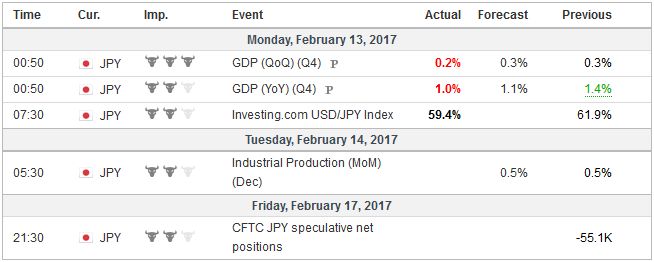

JapanJapan’s economy likely stagnated in Q4 after growing at a 1.3% annualized pace in Q3. Foreign demand (exports) and business investment appears to have offset the decline in domestic consumption. The BOJ estimates trend growth in to be near 0.2%. |

Economic Events: Japan, Week February 13 - Click to enlarge |

United StatesThe US and UK also report January retail sales. They may move in opposite directions. In the US, December retail sales rose a strong 0.6% and likely slowed to around 0.2%. Auto sales remained elevated but slowed sequentially, and this may be offset by an increase in gasoline prices. UK retail sales fell a sharp 1.9% in December and are expected to bounce back in January. The median forecast in the Bloomberg survey was for a 1.0% gain. |

Economic Events: United States, Week February 13 - Click to enlarge |

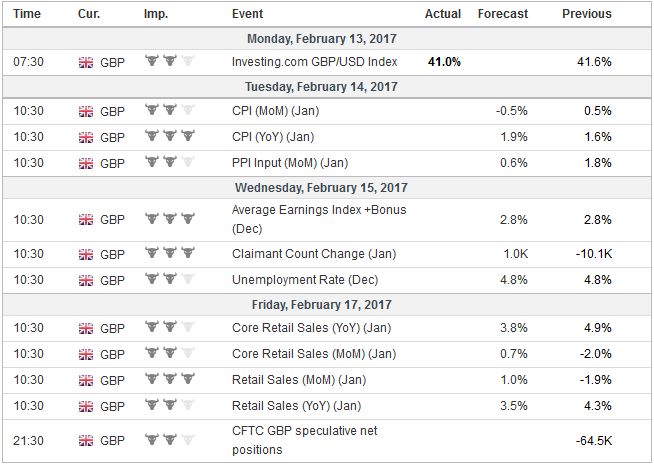

United KingdomThe UK and Australia report their latest employment figures. The British labor market has been fairly steady. The three, six, and 12-month averages have converged just above zero. In percentage terms it has been between 2.1% and 2.3% for nearly two years. In January, the claimant count is expected to have edged slightly higher. However, some signs of deterioration have emerged. Employment growth, which is reported with an extra month lag, like earnings, has slowed, and on three-month comparative basis has been negative in October and November, but is expected to have snapped back in December. Average weekly earnings growth is expected to have remained unchanged in December at 2.3% and 2.1% when bonuses are excluded. In December 2015, average earnings on the three-month year-over-year measure rose 1.9%. |

Economic Events: United Kingdom, Week February 13 - Click to enlarge |

AustraliaAustralia experienced unusually strong job growth in Q4 16. The monthly average was 22.4k, which follows a loss of nearly five thousand jobs a month in Q3 16. Full-time jobs growth was even more impressive, rising 31k a month on average in Q4, the strongest three-month average since Q3 2010. This is not sustainable. Thus there would seem to be downside risks to the median forecast for a 10k increase in jobs in January. The unemployment rate may be driven by the participation rate, which is expected to have remained at 64.7%. Last October’s 64.4% participation rate may have been the low point. |

Economic Events: Australia, Week February 13 - Click to enlarge |

Full story here Are you the author?

Tags: #USD,$EUR,Federal Reserve,newslettersent,SEK