Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Investors will finally be able to focus on what the new US President does rather than what he says.

The UK Supreme Court decision is expected, but it may not be the driver than it may have previously seemed likely.

The dollar-yen rate does not appear to be driven by domestic variable as much as US yields and equities.

Prices not real sector data may be the key for the euro.

United StatesThe US economy grew 3.5% in Q3, and the first estimate of Q4 will be reported on January 27. The NY Fed’s GDP tracker sees growth at 2.4% quarterly annualized rate (2.7% for Q1 17). The median in the Bloomberg poll is 2.2%, while the Atlanta Fed GDP Now estimate is 2.8% for Q4. Third, tax code reform appears high on the priority list. The new Administration wants to cut corporate taxes, simplify the code and reduce income taxes. Although there was some talk of reducing the tax rate on all income brackets, Mnuchin seemed to rule out tax cuts for wealthy households. Trump seems to have rejected the border adjustment tax that the Congressional Republicans advocated, but taxing imports (tariff) continues to be touted. Trump promises deregulation and new regulation have been frozen. The Obama Administration also froze new regulation at the very start. The fourth plank is the $1 trillion infrastructure initiative. It is important for jobs and growth, though apparently not cited on the new White House website. President Trump did include it is his inauguration speech. It is not clear the priority that will be given to filling the two empty seats on the Board of Governors of the Federal Reserve. It is possible that one of the current Governors step down, we expected Yellen (and Fischer) to complete their current terms. Several regional Fed Presidents have already begun to discuss reducing the size of the balance sheet, which seemed to have been an issue for some economic advisers. The US interest rate premium over the UK has narrowed, and this appears to be helping sterling find traction after the brief push below $1.20 at the start of last week. The premium offered by the US on two-year money has fallen below 100 bp from 120 bp at the end of last year. The 10-year premium has fallen from nearly 125 bp to almost 100 bp. Although the US premium over Germany appears to have begun widening again, it has not spilled over to the UK. |

Economic Events: United States, Week January 23 - Click to enlarge |

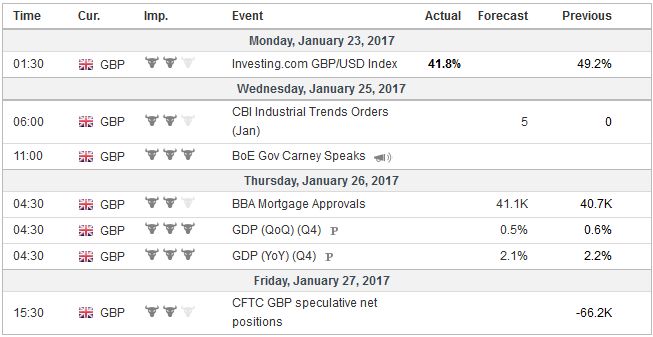

United KingdomAnother important non-economic event that investors will be monitoring is the UK Supreme Court ruling on whether Parliament approval is necessary to trigger Article 50. After Prime Minister May’s speech last week, the decision may have lost some of its ability to roil the markets. May reassured that Parliament would vote on the final agreement. Although many in Parliament seem to has some misgivings about the clean break strategy, which had been thought of as a hard Brexit scenario, there is little doubt a majority will vote to trigger Article 50. The failure to do so would likely spark a political crisis. Northern Ireland will go to the polls on March 2. An anti-Brexit parliament could still frustrate May’s timetable, and Scotland independence efforts may be fanned by the UK government’s position. It is also not immediately clear the implications of the change in leadership of the European Parliament, which will also vote on the final Brexit deal. The UK also reports the first estimate of Q4 GDP. UK growth has been remarkably stable. Quarterly growth has averaged 0.6% over the last four and 12 quarters. Quarterly growth has averaged 0.5% over the past five years. Economists expect the UK economy grew 0.5%-0.6% in Q4 16. |

Economic Events: United Kingdom, Week January 23 - Click to enlarge |

EurozoneThe eurozone reports flash PMI and money supply. Germany reports IFO, and several countries, including Germany, report retail sales. Economic growth in the eurozone, in aggregate, is not a problem. It has been fairly stable and, if anything, a little above trend. The key issue is prices. At last week’s ECB press conference, Draghi argued that underlying price pressures remain muted. Despite the pop in headline prices (1.1% in December from 0.6% in November), core inflation is subdued at 0.9% compared with the trough at 0.6%. One of the concerns of policymakers and investors is a problem with Italian banks. While this is still a work in progress, we note that Italian bank shares have advanced in six of the past eight weeks. More broadly, the bank sub-index of the Dow Jones Stoxx 600 has fallen for the past two weeks and is off five of the last eight weeks. |

Economic Events: Eurozone, Week January 23 - Click to enlarge |

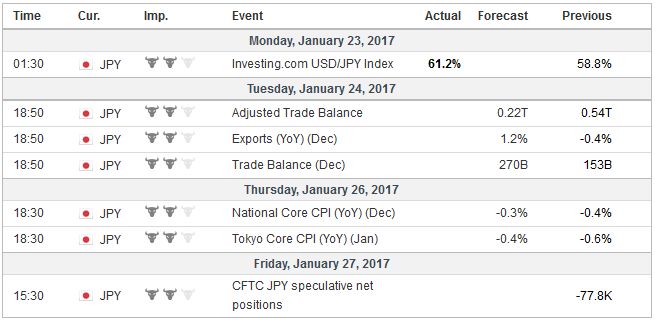

JapanJapan reports December trade figures and CPI. There is a strong seasonal component to Japan’s trade balance. Over the past 20 years, the December trade balance has not improved over November only three times. Exports appear to have risen on a year-over-year basis for the first time since September 2015. Imports are slowly recovering as well. Excluding food and energy, Japan’s CPI is expected to fall back below zero for the first time since August 2013. The drivers of the yen seem clear, and it is not the domestic economy per se. Rather the dollar-yen continues to be driven by two attractors-US yields and equities. On a purely directional basis, the correlation between US 10-year yields and the dollar-yen exchange rate is above 0.95 over the past 60 and 100 days. On a percent change basis, the correlation is at the upper end of where it has been since the middle of 2014. The correlation on a directional basis between the Nikkei and dollar-yen and the S&P 500 and dollar-yen are also elevated. On a percentage change basis, the correlations are not nearly as strong, of course, but are at or near multi-month highs. |

Economic Events: Japan, Week January 23 - Click to enlarge |

AustraliaLastly, we note that the Australia reports Q4 CPI figures. The headline rate is expected to accelerate to 1.6% from 1.3%. Price pressures appear to be bottoming in Australia. A 1.6% pace would be the fastest quarterly increase in 2016. It was at 1.0% in Q2. Rising price pressures appear to have dampened ideas that the central bank may still cut rates. The RBA meets on February 6 and rates will most likely remain on hold. Separately, Australia will report export and import prices, and it appears the terms of trade are improving, partly with the help of stronger iron ore prices. |

Economic Events: Australia, Week January 23 - Click to enlarge |

SwitzerlandUBS will publish the consumption indicator on Wednesday. This is followed by the ZEW investor expectations, that is driven more by stock markets than by economic data. |

Economic Events: Switzerland, Week January 23 - Click to enlarge |

The developments over the last few days, including the strident tones of the inauguration speech, the dispute of the number that attended the inauguration, and the nearly incoherent speech to the CIA may be a small hint to investors of the unpredictable nature of the new US President. The unorthodox style and rhetoric should not distract from the necessary focus on policy. Ultimately, public policies and private sector behavior, not speeches or wishes, drive interest rates, equities, and currencies. Investors will have to get accustomed to the new Administration’s way of conducting itself and communicating.

With broad strokes, and recognizing some contradictory impulses, at this juncture we suggest four main elements of Trump’s economic policy.

The first is re-writing trade deals. This is a central plank. It is one of the key elements of Trump’s foreign policy and job creation plans. The potential of TPP being re-purposed as a bilateral free-trade agreement between the US and Japan remains possible but unlikely.

The priority appears to be to re-negotiate NAFTA. Few people are opposed to reviewing old agreements. No doubt it can be updated; it is 23 years old. Intellectual property rights have evolved, the Internet not only exists but is an important distribution channel for goods, services, and information, there are new tax and accounting rules, and the like. While modernizing old agreement is one thing, changing the essential thrust (reduced barriers to trade, in the North American continent) is quite a different thing. It is not clear to many whether Trump’s rhetoric is part of the “Art of the Deal,” or whether it is a principled position.

Like his predecessors, Trump also talks about enforcing existing agreements. Sometimes there have been trade disputes among NAFTA countries. That is an important thing that is often overlooked about trade agreements. They provide a conflict resolution mechanism; invaluable for resolving and containing disputes. It is like a penalty in a football game or a foul in basketball. The violation of the rules is incorporated into the rules themselves.

Remember too, the desire to negotiate NAFTA (by Bush-the-elder, and approved under Clinton) was partly a reflection of the significance of north-south trade. In effect, the agreement codified and furthered trends already in place, as well as a means to address infractions. The agreement followed trade just as much as more trade followed the agreement.

Second, the White House says it wants the US to create 2.5 mln new jobs over the next decade. Over the last five years, the US created an average of 197k net new jobs a month. The five-year monthly average has rarely been over a 200k. Although during the campaign there was talk of achieving 5%-6% growth, the White House now says 4%, while Mnuchin said 3%-4% in his confirmation hearings.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$EUR,$JPY,newslettersent