Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

Bank of Canada may be more upbeat following strong jobs and trade figures.

China’s President Xi will speak at Davos and likely defend globalization and free trade, which some think the US is abandoning.

UK PM May’s speech on Brexit may be blunted by few surprises, collapse of the government in Northern Ireland, and the pending Supreme Court ruling.

ECB will leave rates on hold and look for Draghi to push back against ideas that rise in CPI means QE should be tapered.

Donald Trump becomes the 45th US President on January 20.

Like many, we recognize that political factors may overshadow macroeconomic drivers in shaping the investment climate in the period ahead. We suspect this will be very much the case in the coming days. It is not that the economic data doesn’t matter, but for many investors, the imprecision and quirky nature of the high frequency economic data pale in comparison to the risks emanating from politics and policy.

Before providing a thumbnail sketch of the five events, we think may shape the investment climate in the week ahead, allow us to briefly preview the economic highlights. The US and Japan round out the large countries industrial output reports. Europe accelerated. Japan is will likely confirm the strongest monthly increase since March 2014. US industrial output is expected to have snapped back from a weak November. The soft patch the dragged it lower for three of the past four months through November may have ended.

The US, UK, and Canada report inflation measures. UK inflation is expected to have stabilized at higher levels, though PPI may continue to trend higher. US headline CPI is expected to continue to converge with the core rate, as is repeatedly done for the past fifty years. It is expected to push through 2.0% for the first time since July 2014. The core rate is expected to tick up to 2.2% from 2.1%. Canada’s CPI has averaged 1.4% this year and 1.1% in 2015. It is expected to rebound from 1.2% in November to 1.7% last month.

Investors will get an update the UK labor market, which has lost some momentum in recent months, and average weekly earnings that appear to have steadied. Australia reports December employment figures. It created almost 25k jobs a month in 2015 and less than a third of that in 2016. It reported an outsized 39.1k job growth in November. These were all full-time jobs. Economists expect a 10k increase in December, which seems optimistic. Canada reports November retail sales. The 1.1% jump in October (1.4% excluding autos) is obviously unsustainable. The risk seems to be on the downside of the Bloomberg median forecast of 0.5%.

Now, let’s turn to the five key events:

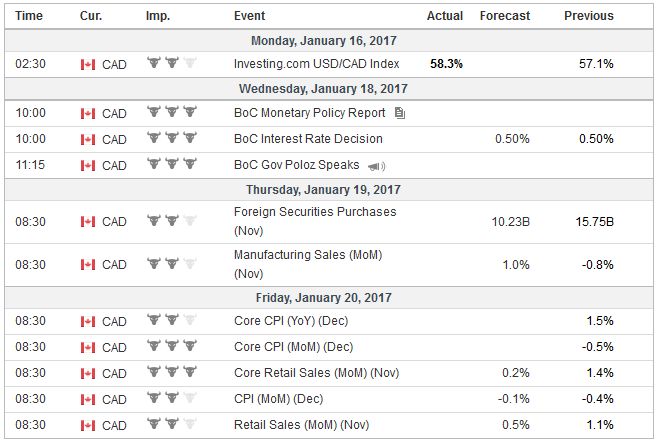

CanadaBank of Canada meeting and updated economic assessment: The overnight rate will remain unchanged at 0.5%, and the anticipation of closing the output gap in mid-2018 also won’t be altered. However, we flag this because we expect a more upbeat tone to the central bank’s neutrality. Also, we suspect that in the US dollar appreciation that we expect to resume shortly, investors will also look for alternatives to the greenback and the Canadian dollar is a potential candidate. The Canadian dollar was the strongest of the major currencies against the US dollar in 2016, gaining almost 3%. The US dollar has been sold from CAD1.36 on December 30 to nearly CAD1.30 on January 12. The US two-year premium has fallen from nearly 48 bp to 39 bp at the end of last week. It is approaching the lower end of a range (~35 bp) that has been sustained since the middle of November. The US premium had risen steadily from below six bp last-July. The US 10-year premium more than doubled from last April’s 32 bp to 81 bp peak in late-November. It has subsequently pulled back and has not been above 70 bp since January 4. |

Economic Events: Canada, Week January 16 - Click to enlarge |

United StatesTrump’s inauguration: Donald J Trump will become the 45th President of the United States on January 20. There is great uncertainty surrounding the policies his administration will pursue, and its priorities. The only thing we can be confident of is there will be changes in both style and substance. It has already become clear in the confirmation process that many of new cabinet officials disagree with important elements Trump’s campaign rhetoric, and disagree with each other. Presidents have their own decision-making style, and it is not clear where power will truly lie. Only infrequently is an org chart particularly helpful. Amid the uncertainty, there are a few important constants. First, the economic team is very pro-growth. The usual reasons for not pursuing policies that lead to stronger growth, as the effect on the trade deficit, the dollar, or inflation are not acceptable to many in the new economic team. Second, Trump does not feel bound by American tradition, including resisting sphere of influence claims (including formally recognizing Russia’s annexation of Crimea), opposing nuclear proliferation, defender of free-trade, and the acceptance that Taiwan is part of China (even while opposing a military solution). Third, the communication style, including the extensive use of Twitter and citing names of specific companies and people, create new uncertainties for investors. In situations like that, people often find ways to look like they are complying in hopes of deflecting negative attention while pursuing their own agenda. Fourth, the style and policy substance is likely to lend itself to a heavy volume of misunderstanding, clarifications, and in one word, controversies, that make it all the more important that investors distinguish between noise and signal and focus on the latter. |

Economic Events: United States, Week January 16 - Click to enlarge |

ChinaChina’s President Xi goes to Davos: This will be the first time a Chinese President attends Davos. It is part of an important and ironic juxtaposition that appears to be unfolding. It will be Chinese “core” leader that will defend globalization from the populism and protectionism that appears to be on the rise in the United States and Europe. The shoe has been on the other foot for years. Chinese nationalism was worrisome for many. It was China’s reluctance to free-trade rules embodied in the WTO agreements that was the cause of much trade friction. Meanwhile, the price of stabilizing the economy has been a continued increase in credit extension. At the same time, capital controls have been tightened stem the outflows. The painful squeeze inflicted in the offshore yuan market continues to deter speculation as CNH is trading at its largest premium (rather than the more usual discount) for the longest period under this dual currency regime. We had argued that just like Bush and Obama backed off their campaign pledges to cite China as a currency manipulator when they assumed office. Our forecast that Trump would also back off his pledge to cite China on day one was also bluster is coming to pass. In an interview in the Wall Street Journal, the President-elect says it won’t be day one. He will talk to them first. Revealing either his reluctance to take language seriously or a subtle slight to China, Trump referred to President Xi as chairman. It would be like calling a US president Commander. It is a title they have but not this purpose. Alternatively, it could be a jab that Xi is not elected. More antagonistic to the Chinese, Trump said he is not committed to the US traditional one-China policy. He claimed it was up for negotiations. |

Economic Events: China, Week January 16 - Click to enlarge |

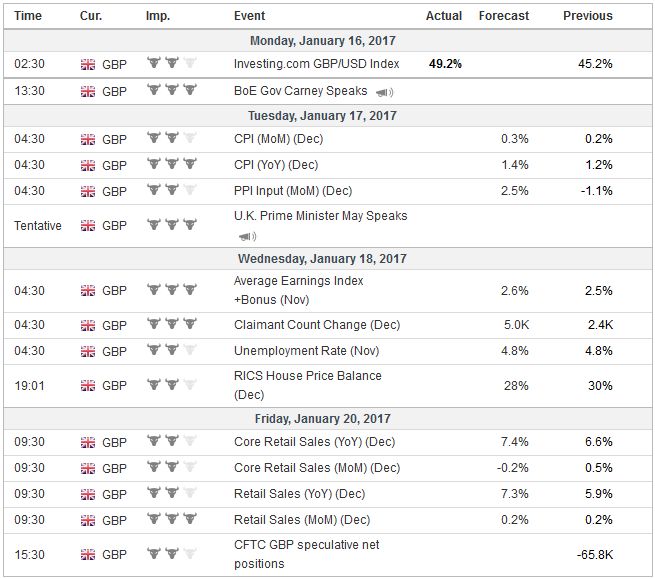

United KingdomMay’s Brexit strategy: When May became Prime Minister there was a small window of opportunity to change the trajectory. She could have said she was not bound by Cameron’s pledge to adhere to the results of the referendum. May’s government has not been bound by other policies of the previous Tory government. She could have said that the referendum was non-binding and why pretend otherwise. It won with the slightest of majorities, which was not to make such an important decision as changing a treaty. With Labour having inflicted on itself serious injury, she could have won an election if she lost a vote of confidence. Instead, she went with the “Brexit is Brexit” slogan that may still prove tantamount to cutting one’s nose to spite one’s face. A week ago, May confirmed that she was willing to sacrifice access to the single market in exchange for greater control over immigration and not being subject to the European Court of Justice. Sterling fell in response through the $1.22 area that had served as a base since October and fell to two-month lows against the euro. She is expected to outline more of her approach in a speech on January 17. A new wrinkle has emerged, and it may blunt or neutralize the negativity of the hard exit that May appears to be leading the UK. The Northern Ireland government collapsed at the start of last week. If the UK Supreme Court grants, it is expected to do shortly, a role for the parliament that sits in Westminster, the Parliament in Northern Ireland has joined the suit. Without a sitting parliament in Northern Ireland, May’s intention on triggering Article 50 at the end of Q1 would likely be frustrated. |

Economic Events: United Kingdom, Week January 16 - Click to enlarge |

EurozoneECB meeting:After having adjustment policy last month, there seems to be practically no chance that the ECB introduces new initiatives. Draghi’s presentation may be ho-hum. The eurozone economy has evolved in line with the ECB’s expectations. Investors will be most interested learning Draghi and the ECB’s take on the stronger than expected rise in CPI. Recall headline CPI jumped to 1.1% in the preliminary estimate in December from 0.6% in November. It is expected to be confirmed the day before the ECB meets. Draghi can be expected to resist ideas such as those suggested by German Finance Minister Schaeuble that it is time to reconsider the thrust of monetary policy. If it were up to officials like Schaeuble, the policy would not have been implemented in the first place. The first inkling that policy is indeed working is not the time to pullback, Draghi may say. In addition to cautioning against jumping to conclusions based on one month’s data, he may note that the rise in headline measures is primarily the result of energy prices. The core rate increased to 0.9% in the preliminary estimate for December. The cyclical low was 0.6%. Pressure is likely to mount until the updated staff forecasts in March. Note that the base effect warns of additional gains in CPI. Last January’s 1.4% decline (month-over-month) will drop out of the year-over-year comparison. Despite the increase in price pressures, inflation expectations remain deflated. The German 10-year breakeven is a little below 1.3%. |

Economic Events: Eurozone, Week January 16 - Click to enlarge |

Switzerland |

Economic Events: Switzerland, Week January 16 - Click to enlarge |

Full story here Are you the author?

Tags: #USD,Brexit,EUR/GBP,newslettersent,yuan