Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Jonathan Watson

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitter

Swiss Franc |

EUR/CHF - Euro Swiss Franc, January 09(see more posts on EUR/CHF, ) - Click to enlarge |

|

I am reading a lot about the pound in 2017 which is likely to be as volatile as in 2016. But the Franc is a harder beast to predict. Loosely tracking the euro but subject to its own rules and trends GBPCHF could be an interesting pair to watch in 2017. There are numerous global events which can shape the direction on the Franc and clients looking to exchange pounds into Francs or move Francs back to the UK should be considering the path ahead. As a safe haven currency the Franc is seen by investors as a safe bet and will often perform well in times of global and economic uncertainty. In the past the Swiss National Bank have cut their base interest rate into negative territory to help fight the strength of the currency. I think that 2017 could see them be forced to act further on such moves as global uncertainty piles pressure on the Swiss currency. But despite cutting interest rates the Franc will still strengthen as investors avoid the Euro and the pound. Global uncertainty can include for example wars but also political uncertainty. I foresee increased Russian aggression in Europe which will put pressure on the strained NATO relations. I also foresee increased political uncertainty in the Eurozone as the sentiments that predicated the UK’s Brexit vote are mirrored across the continent. Nationalist uprisings in France, Holland and Germany are all gathering pace and even if 2017 isn’t the year they take power I do feel that this trend towards less international cooperation will help the Franc. |

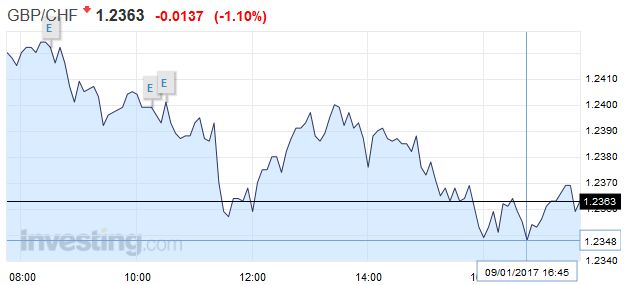

GBP/CHF - British Pound Swiss Franc, January 09(see more posts on GBP/CHF, ) - Click to enlarge |

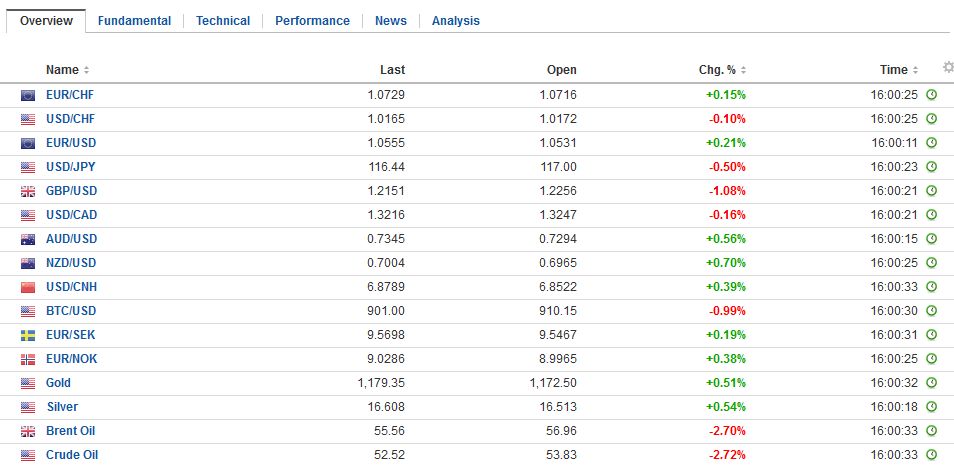

FX RatesSterling has stolen the US dollar’s spotlight. The issue facing market participants was if the rise in hourly earnings reported as part of the pre-weekend release of US December jobs data was sufficient to end the dollar’s downside correction. Instead, May’s comments over the weekend indicating not just a desire but strategic thrust to abandon the single market in exchange for regaining control over immigration and not being subject to the European Court of Justice has cost sterling more than one percent. Sterling has been sold through $1.22 for the first time since the end of October. Last week’s recovery fizzled near $1.2430. It reached $1.2125 in the European morning. The next downside target is near $.12080. The $1.22 area that was once support is likely to be seen as resistance. The weakness of sterling is helping allow the FTSE 100 extend its winning streak to its tenth session and 14 of 15 sessions (yes, it had declined once since December 14 when the Fed hiked rates). |

FX Daily Rates, January 09 - Click to enlarge |

| Asian equities extended their pre-weekend losses, without Japan, where markets were closed due to a national holiday. The MSCI Asia-Pacific Index excluding Japan fell nearly 0.25%. The loss before the weekend snapped an eight-day advance. Chinese shares bucked the trend. The Shanghai Composite gained a little more than 0.5%.

|

FX Performance, January 09 - Click to enlarge |

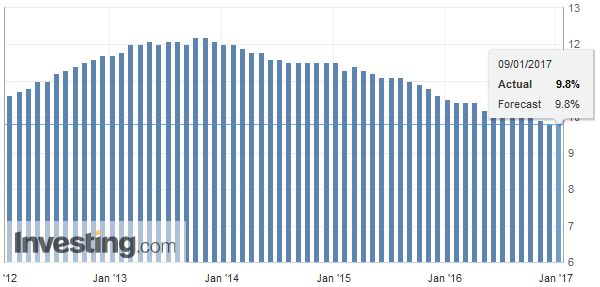

EurozoneEuropean shares are otherwise heavy today, with the Dow Jones Stoxx 600 off 0.4%, lead by the telecoms and real estate sectors. If sustained, it would be the third decline in four sessions as the momentum seen early last week fades. Italian and German data drew some attention. Even though Italy created 19k jobs in November, the employment ticked up to 11.9% (from 11.8%). When combined with the other EMU members, the aggregate unemployment rate was unchanged at 9.8%. |

Eurozone Unemployment Rate, December 2016(see more posts on Eurozone Unemployment Rate, ) Source: Investing.com - Click to enlarge |

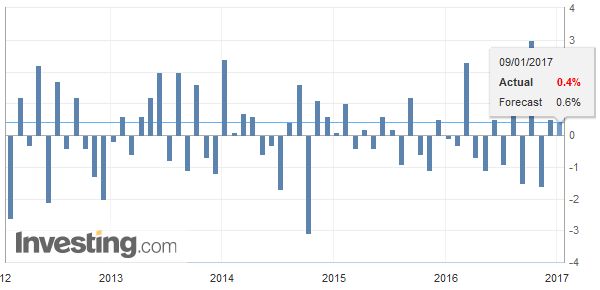

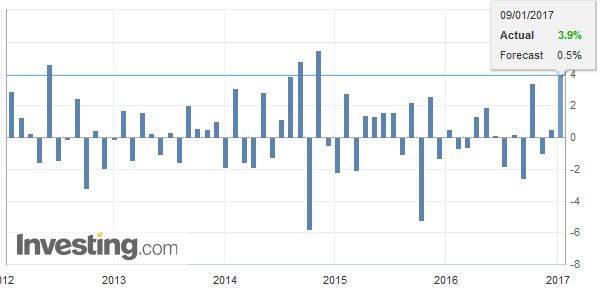

GermanyGermany reported a 0.4% rise in November industrial output, which was a bit softer than the 0.6% median forecast. However, the year-over-year pace of 2.2% was above expectations and the best in three months, and the third best of the year. This, alongside the PMI, provides more evidence acceleration of the Germany economy in Q4. Construction output rose 1.5%. Manufacturing production rose 0.4%, while energy output fell 0.4%. |

Germany Industrial Production MoM, December 2016(see more posts on Germany Industrial Production, ) Source: Investing.com - Click to enlarge |

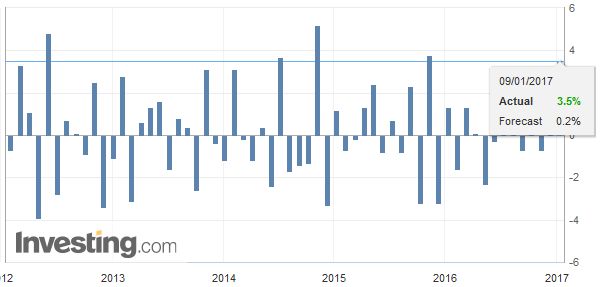

| It appears that some of the manufacturing was for exports, as separately, Germany reported exports rose 3.9% in November. This is a four and a half year high. The median forecast was for a 0.5% increase. |

Germany Exports MoM, December 2016(see more posts on Germany Exports, ) Source: Investing.com - Click to enlarge |

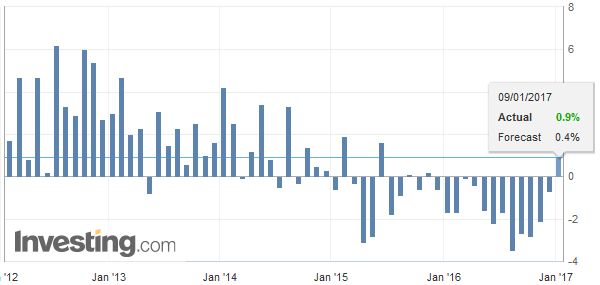

| German imports rose 3.5%. The net result was a 22.6 bln euro trade surplus, up from 19.4 bln euros in October. The surplus was steady around 21.1-21.6 bln euros where the six- and 12-month moving averages are found. The three-month average is 22.1 bln. |

Germany Imports MoM, December 2016(see more posts on Germany Imports, ) Source: Investing.com - Click to enlarge |

Switzerland |

Switzerland Retail Sales YoY, December 2016(see more posts on Switzerland Retail Sales, ) Source: Investing.com - Click to enlarge |

China

Outside of sterling and European data, the third development on investors radar screens is the easing of the money market squeeze has seen the Chinese yuan come under new pressures. The overnight offshore yuan (CNH) deposit rate fell 12.5 percentage points, after hitting 105% before the weekend. CNH fell nearly 0.5% today as some of the bears who were squeezed out last week may have begun reestablishing positions. The onshore yuan fell 0.2%.

South Korea rivaled China for attention today in Asia. The won fell nearly 1.3%. Part this may be a strong dollar. Part of this may be concern that North Korea may launch a long-range missile any day. However, the won’s weakness also seems to be partly a function of a spat with Tokyo relating to the so-called comfort women. Japan not only recalled its ambassador but also suspended talks about the currency swap arrangement. Lastly, there was also some concern that the influence-peddling scandal that toppled the Park government may be spreading to industry.

United States

The US economic calendar is light with only November’s consumer credit on tap late in the session. Fed’s regional Presidents Rosengren and Lockhart speak. After the rise in hourly earnings, the market increased the probability of a March rate hike. We note that the base effect means likely means that the pace of hourly earnings growth slows in January.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,EUR/CHF,Eurozone Unemployment Rate,FX Daily,gbp-chf,Germany Exports,Germany Imports,Germany Industrial Production,newslettersent,South Korea,Switzerland Consumer Price Index,Switzerland Retail Sales,yuan