Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

Jonathan Watson

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitter

Swiss FrancThe Swissie has remained very strong against a much weaker pound but the outlook is still very shaky. The principal reason for the changes are of course the election of Donald Trump which has sent some big ripples through financial markets. The Swiss Franc did strengthen significantly as we saw uncertainty ahead of the election but following the result it was more the pound making headway with some big shifts on GBPCHF. Will the pound now make a comeback against the ever safe haven Swiss Franc? |

EUR/CHF - Euro Swiss Franc, November 16 . - Click to enlarge |

| With the outlook on the pound remaining uncertain but slightly more positive there is a real risk of disappointment for clients buying CHF with sterling. Most clients will be very familiar with the Brexit but we know almost nothing about what it means and we will have to wait and see exactly what it does mean. It does appear the weaker pound will weigh on the UK economy and in the future higher inflation will put increased pressure on the already delicate economic situation in the UK.

With the Franc having strengthened in recent months it is now the pounds turn to find some favour but I do believe the current improvements will prove shortlived. I would personally be very concerned about what lies ahead for the UK and would be cautious expecting big improvements for CHF buyers. If you are selling CHF following a property sale or repatriating any funds to the UK rates remain very good and might yet get better. |

GBP/CHF - British Pound Swiss Franc, November 16 . - Click to enlarge |

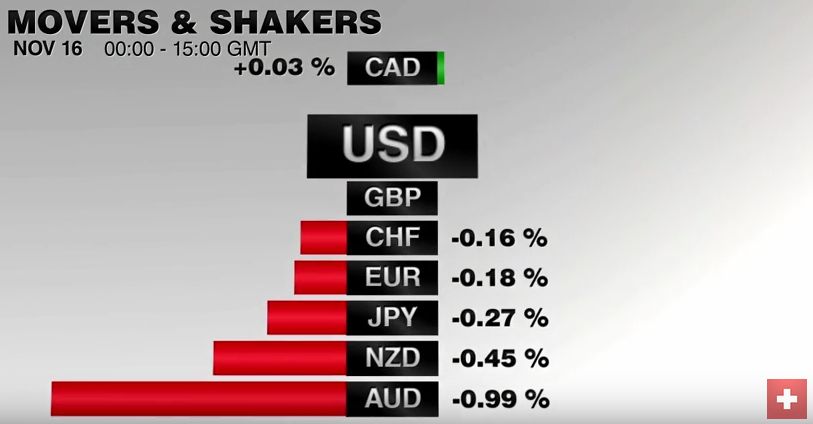

FX RatesThe US dollar remains bid. It is at its year high against the euro and five-month highs against the Japanese yen. Sterling, which has performed better recently, remains in the trough around 30-year lows. It surge since the election reflects three considerations. The first is December Fed hike. Prior to the election, the market was assessing around a two-thirds chance. Now both the CME and Bloomberg’s WIRP estimate the odds above 90%. Investors have also increased the anticipated path of Fed next year as well. |

FX Performance, November 16 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| Second, and partly related, the new US Administration has promised significant fiscal support on par with the Feb 2009 package delivered near the low point of a deep downturn. Of course, there is more unknown than known at this juncture. However, it does seem that some measure of fiscal stimulus will be forthcoming. Both candidates had promised it, and Trump’s proposal was larger. The Democrats may support the spending increases and the Republicans the tax cuts. More broadly, a pattern may be emerging where fiscal policy is no longer taboo, though the EC apparently has not gotten the memo. |

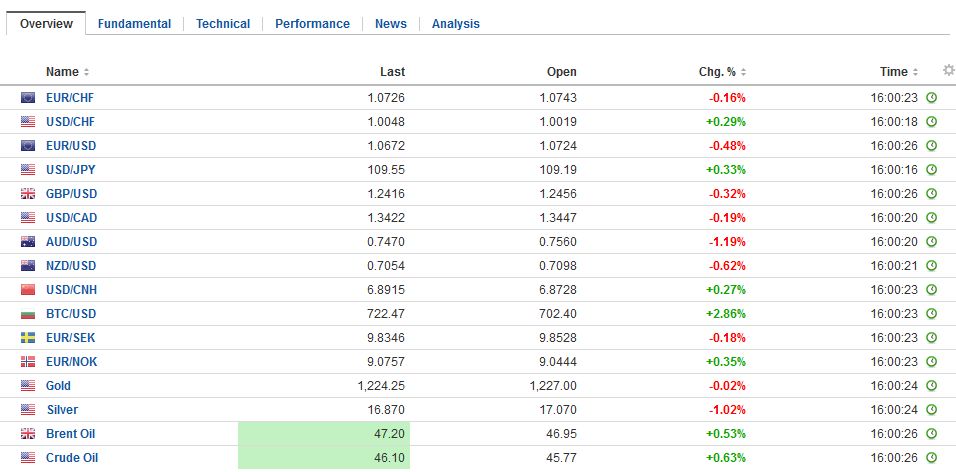

FX Daily Rates, November 16 (GMT 16:00) . - Click to enlarge |

| Third, another pattern that is influencing investment is the rise of the populist right. Europe is particularly vulnerable. The calendar is not particularly kind, with the Italian referendum and Austrian Presidential election (do-over) in early December. The Dutch go the polls in early spring. These events are like a dress rehearsal for the French presidential election. Le Pen is running strong and, given the disrepair of the Socialist Party, is expected to make it to the run-off to face the Republican candidate (first round of the first primary is this coming weekend).

The combination of these considerations and market positioning helps explains the persistence of some of the moves in the capital markets, including the strength of the dollar. Another persistent move is the adjustment of long-term interest rates. Yesterday’s pullback in yields was corrective in nature and not the start of a serious correction. Japan’s 10-year bond yield is above zero today (one basis point), the highest since March and the fifth consecutive increase. |

FX Performance, November 16 . - Click to enlarge |

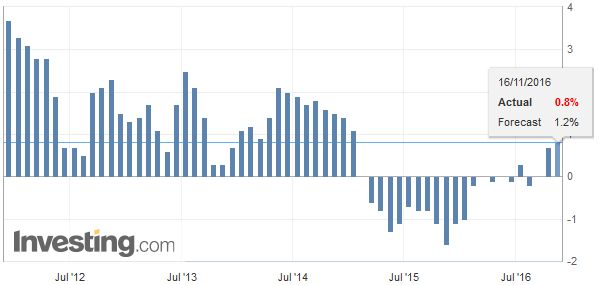

United KingdomEconomic news has been largely limited to the UK labor report. Although the unemployment rate ticked lower (4.8%) and is a new cyclical low, there are some yellow flags below the surface. The claimant count increased for the third consecutive month. Employment rose 49k in Q3 after 172k in Q2. It also means that increase in output per hour slowed.

|

U.K. Unemployment Rate, October 2016(see more posts on U.K. Unemployment Rate, ) . Source: Investing.com - Click to enlarge |

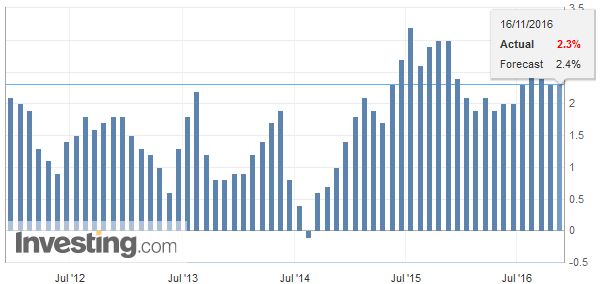

| Average weekly earnings remain steady at 2.3% (Q3 16 over Q3 15). However, with inflation rising, real wage growth eased to 1.7%, the lowest in 18 months. |

U.K. Average Earnings Index +Bonus, October 2016(see more posts on U.K. Average Earnings, ) . Source: Investing.com - Click to enlarge |

United StatesThere are also questions about President-elect Trump promising to cite China as a currency market manipulator. A cautionary note is that such promises are not uncommon on the campaign trail. Obama made similar declarations as did Bush. Most recently China has been intervening to strengthen its currency. If it did not intervene and stepped away from the market, it seems most likely that the yuan would weaken, and perhaps dramatically. On the trade front, we point out that the US trade deficit with China, whether relying on Chinese figures or American data, has fallen this year. Yesterday’s US retail sales data were stronger than expected, and Q4 GDP estimates were likely tweaked higher. Today’s data releases include producer prices, which are likely going to show what some economists call pipeline price pressures building, and industrial production. The markets are not particularly sensitive to these reports. Three Fed Presidents speak today, though Bullard has already spoken. His new approach, unveiled earlier this year, calls for only one rate hike to restore equilibrium. In contrast, many in the market are talking about two or three next year. Kashkari speaks in the NY morning and Harker late in the session. |

U.S. Producer Price Index (PPI) YoY, October 2016(see more posts on U.S. Producer Price Index, ) . Source: Investing.com - Click to enlarge |

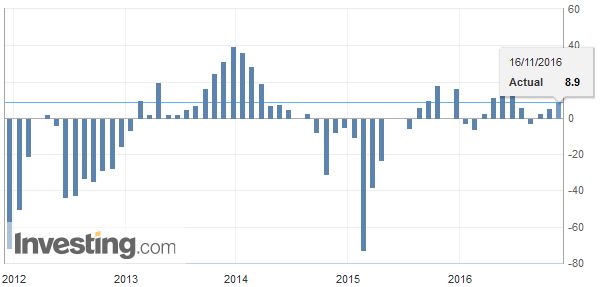

Switzerland |

Switzerland ZEW Expectations, October 2016(see more posts on Switzerland ZEW Expectations, ) . - Click to enlarge |

Eurozone

European benchmark bond yields are rising after yesterday’s brief dip, and premiums over Germany are widening. Italy and Spain’s 10-year yields are up eight and six basis points respectively, while Germany is up 3 and France 4. The US 10-year yield is up five bp at 2.27%. We note that the US premium over Germany is edging to new decade highs.

Japan

Japan’s Topix extended its rally for a fifth consecutive session with a 1.3% gain. A key driver has been the financials. In the past five sessions, the bank index has rallied 20%, the most since 2008. There are at least three considerations here. First, despite negative rates and other hardships, banks earnings were better than expected. Second, the weaker yen is helpful. Third, increase in domestic and global interest rates is also beneficial.

The MSCI Asia-Pacific Index snapped a three-day decline and rose by 0.35%. Stocks in Europe are struggling to extend the two-day rally. The Dow Jones Stoxx 600 is up less than 0.2%, energy and financials are leading the advancing sectors. Interest-rate sensitive utilities continue to underperform and are off 1.25% near midday in Europe.

The dollar is at eight-year highs against the Chinese yuan today. While it seems to be a talking point, it does not appear to be a major market force. We share the following observations. Since the US elections, the Chinese yuan has been among the strongest currency in the world. Since November 7, it has fallen 1.4% against the dollar. In Asia, the only currencies to have done better is the pegged Hong Kong dollar, the Taiwanese dollar (-1.0%) and the Thai baht (-1.3%). Among the major currencies, the yuan has appreciated against all but the British pound (+0.4%) and Canadian dollar (-0.8%).

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,China,newslettersent,Switzerland ZEW Expectations,U.K. Average Earnings,U.K. Unemployment Rate,U.S. Producer Price Index