Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss Franc |

EUR/CHF - Euro Swiss Franc, November 11(see more posts on EUR/CHF, ) . - Click to enlarge |

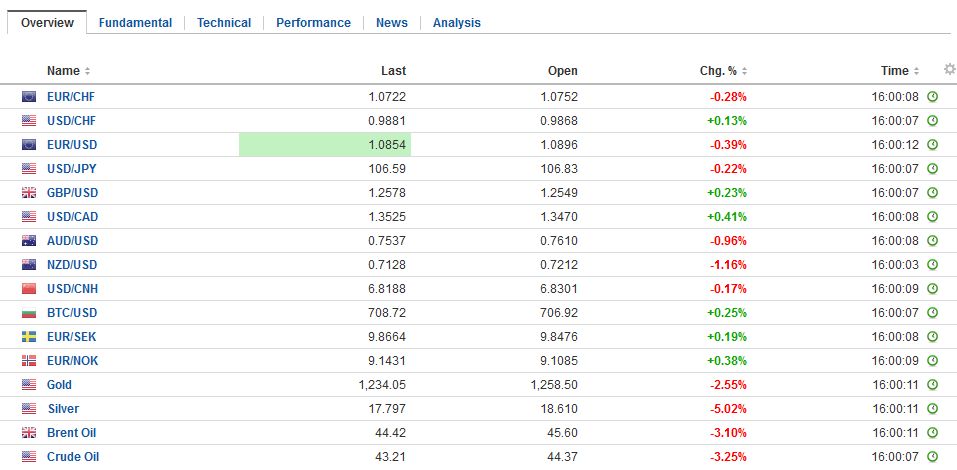

FX RatesThe forces unleashed by the US election results continue to drive the capitals markets. The combination of nationalism, reflation and deregulation are seen as good for US equities and the US dollar. It has not been so kind to US Treasuries, where the 10- and 30-year yield has risen about 32 bp this week coming into today’s federal holiday that closes the bond market, while the stock market is open. The rising US yields, anticipated trade policy, has hit emerging markets particularly hard. Many Asian countries are predisposed to manage their currencies, and the downside pressure on them has seen a wave of intervention today, according to reports. Contrary to ideas of “race to the bottom” or “currency wars” were “everyone” wants weaker currencies, a number of Asian central banks are believed to have sold dollars and bought their own currencies to slow the descent. |

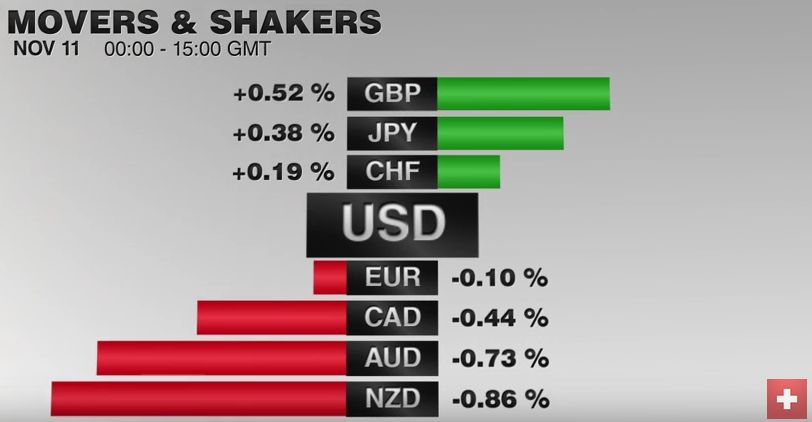

FX Performance, November 11 2016 Movers and Shakers . Source: Dukascopy - Click to enlarge |

| Flows out of the emerging markets are one of the important themes to have emerged in recent days. The MSCI Emerging Market equity index fell for the third consecutive session. The 2.4% decline so far today brings the three-day decline to almost 6%. The index is at its lowest level since July.

Among the major currencies, there has been only one that has outperformed the US dollar this week, and it is the British pound. Ir recouped the losses from earlier in the week yesterday and is extending those gains today. At $1.2660, it has risen 1.1% on the week and has surpassed the flash crash high (~$1.2625) for the first time. It has also met the 50% retracement objective of the last notable high from September 6 (~$1.3440). The next retracement is seen near $1.2830. |

FX Daily Rates, November 11 (GMT 16:00) . - Click to enlarge |

| Sterling’s gains are partly a function of unwinding short positions, especially against the euro. The euro’s decline against sterling this week (~3.6% at GBP0.8575) is the most since early 2009. It is the second consecutive weekly decline and is only the third such decline since early September. The driving force is not so much a reassessment of the UK as much as the recognition that EMU is particularly vulnerable to the rise of nationalism.

While sterling has been the best performing major currency, the Japanese yen has been the worst. It has fallen a little less than 3% this week. The dollar’s five-day advance against the yen may be in the process of being snapped. Near midday in London, the dollar is off about 0.6% to near JPY106.00. It has run into some offers near JPY107.00. Given the sharp advance from the initial drop to JPY101.20 on the US election results, the initial support on a break of JPY106 is not found until closer to JPY104.75JPY105.00. |

FX Performance, November 11 . - Click to enlarge |

ChinaOf note, China’s markets are resilient in the face of the reassessment of emerging markets. The yuan is fallen about 0.7% this week, making it among the performing Asian currencies this week, with only the fixed Hong Kong dollar and Indian rupee doing better this week. We note that there the Indian officials are believed to have intervened today as the rupee slipped to seven-week lows. The Shanghai Composite rose about 0.8% today to take the five-day advance to 2.25%, reaching its highest level since January. If Brexit and the US election represents a new expression of nationalism, China’s nationalism may put it in a relatively better position than other countries. |

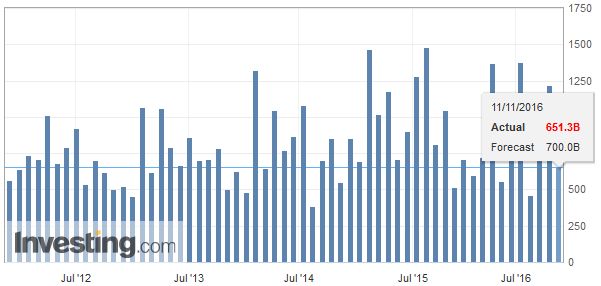

China New Loans, October 2016(see more posts on China New Loans, ) . Source: Investing.com - Click to enlarge |

Eurozone

The next blow against globalization and integration is seen to come from the eurozone. The Italian referendum and the Austrian presidential election are about three weeks away. Somewhat more down the field is the Dutch election in Q1 17 and the French presidential election next spring in which the National Front’s odds of winning are seen to have increased over the past few days.

European shares as measured by the Dow Jones Stoxx 600 is up about 3% this week, though is narrowly mixed today. However, the more acute pressure is coming from the adjustment of interest rates. European bonds continue to sell-off, and in the rising interest rate environment, the spreads against Germany are widening. It is not just in the periphery, but the French premium over Germany on 10-year money has widened by 10 bp to more than 40 bp. It is the most in five months.

Italy

Italy’s 10-year benchmark yield has risen nearly 25 bp this week, pushing the yield to 2%, its highest in more than a year. Rising sovereign yields may weigh on Italian banks, which are large holders of government bonds. Italian banks have fared well so far the face of the dramatic rise in yields, but are snapping a four-day advance today with a minor loss.

The euro has steadied after approaching last month’s low near $1.0850. It is off 2.4% on the week. With today’s minor slippage, it has extended its losing streak to the fifth consecutive session, snapping the four-day advance seen last week. Below the $1.0850 are the March lows near $1.0820, and the lower Bollinger Band comes in a little below there.

We see two main forces weighing on it. The first, we have already mentioned, and that is the political calendar and the forces of nationalism. The second is the widening interest rate differential between the US and Germany. The two-year spread finished last week near 142 bp. It closed yesterday near 153 bp. The US Treasury market is closed today, so the slight narrowing is a result of the small rise in the German two-year yield. The ECB is expected to announce the extension of its asset purchases next month beyond the soft March 2017 end-date, while the market is more confident of a Fed hike a couple of weeks later.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$EUR,$JPY,China New Loans,EUR/CHF,newslettersent