Panic PauseThe sudden panic about a potentially imminent Italian banking sector collapse back in July has somewhat subsided for now, but sooner or later the issue will inevitably rear its ugly head again. |

The impressive headquarters of the world’s oldest surviving bank, Monte dei Paschi di Siena, Piazza Salimbeni Photo credit: Stefano Rellandini / Reuters - Click to enlarge |

| Two months after Italian bank stocks collapsed even further in the aftermath of the Brexit vote, fears of an imminent need for a bail-in have receded as the Italian government works on plans to shore up its weakest bank, Monte dei Paschi di Siena (MPS).

This will be achieved via an alternative but rather ambitious method culminating—if all goes according to plan—in a new capital injection. However, MPS, which came up short in July’s ECB stress tests, has already received capital injections in the past. |

Euro Stoxx Bank Index(see more posts on Euro Stoxx bank index, ) Euro Stoxx bank index, monthly. The index remains close to its 2012 panic lows. The decline since 2015 has been broad-based, but Italian bank stocks were particularly weak. - Click to enlarge |

| Such plans to patch up banks have tended to involve kicking the can down the road rather than providing a more definitive solution to the 360 EUR billion of non-performing loans (NPLs) weighing down Italy’s banking sector, equivalent to one fifth of its GDP.

If a sustainable solution is not found to clean up Italian bank balance sheets in the near future, they will inevitably constrain domestic demand and thereby weigh on the country’s already feeble growth even further. |

The Italian Dilemma Italy: GDP components, GDP growth rates and current account – click to enlarge. - Click to enlarge |

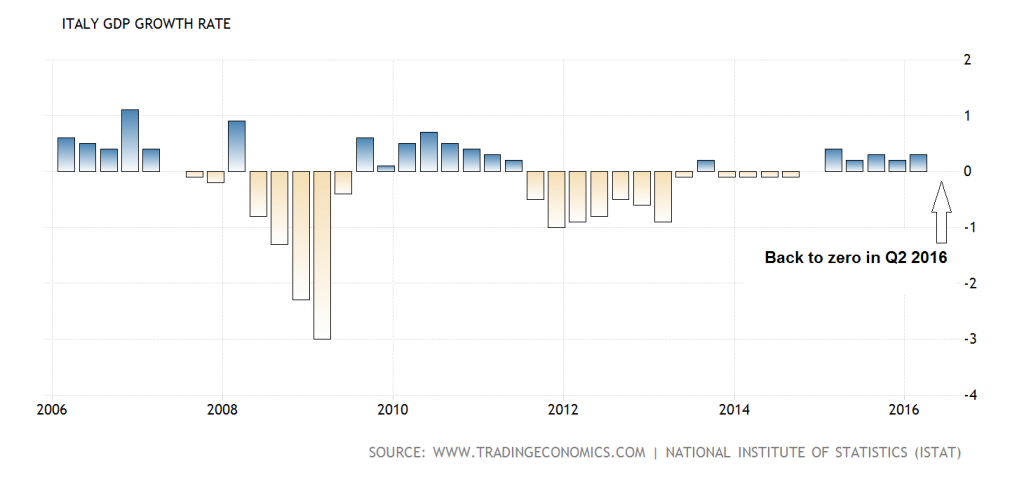

Faltering Domestic DemandDomestic demand, the longstanding mainstay of the Italian economy, is already under intense pressure. In the second quarter, GDP failed to grow in quarter-on-quarter terms, primarily on the back of a broad-based deterioration in all components of domestic demand (private consumption, government consumption and fixed investment), which could not be offset by the unusually-positive contribution of the external sector to growth. The difficult climate for domestic demand in Italy is nothing new, since the austerity policies implemented in recent years have taken their toll and Italian governments have centered their efforts on trying to boost external demand instead in order to reverse the current account deficit Italy had until 2012 and keep it positive going forward. And yet private consumption has remained the main driver of Italy’s feeble economic recovery. Analysts foresee that the poorer-than-expected performance of domestic demand (especially private consumption) in the second quarter this year will be temporary, but its growth rate will nevertheless decelerate in 2017. Our latest September Consensus Forecast for Italy, obtained by polling 37 local and international analysts, sees GDP growing a meager 0.9% both this year and next, a figure which has in both cases been gradually revised down in recent months from the 1.2% forecasts for both years back in January. The panel are basing their growth projections primarily on modest improvements in consumer spending, albeit at a slower rate than initially expected, on the back of gradual gains in household disposable income fueled mainly by improving employment and low inflation. Domestic demand is forecast to contribute 1.1 percentage points to total growth this year (which will be dragged down slightly by a 0.2% contraction in the external sector), of which 0.7 percentage points will come from the strongest component, private consumption. In 2017, domestic demand is expected to decelerate and contribute 0.8 percentage points to growth while the external sector will pick up slightly. Of the domestic demand components, private consumption is seen remaining the main cornerstone of the tentative recovery next year, decelerating from 2016 but still contributing 0.5 percentage points to growth. |

Italy GDP Growth Rate Italy, q/q GDP growth – back to zero as of Q2 2016 (note: y/y growth was 0.8%) - Click to enlarge |

Vicious CircleA failure to swiftly clean up bank balance sheets means domestic demand will inevitably suffer as bank credit supply constraints continue to prevent the recovery of investment. Loan-loss provisioning reduces the credit banks have available for lending, especially to small and medium-sized enterprises (SMEs) and consumers, which are perceived as risky. Arguably, analysts assessing the Italian banking sector are now most worried about the risk of chronically constrained growth rather than another systemic shock, as banks are trapped in a vicious circle whereby poor economic growth means bad loans keep growing, which in turn weigh on growth even further. The latest ECB stress tests showed that most Italian banks do have loss-absorbing capacity to withstand a theoretical three-year economic shock, but strong concerns remain about their profitability as NPLs reduce their lending ability and deter investors. Moreover, this scenario of sustained weakness prolongs the risk of banks eventually being forced to resort to a bail-in. A recapitalization of the banking sector involving substantial losses for retail investors would strongly hit consumer confidence and spending, the backbone of Italy‘s economy, which analysts we surveyed foresee as remaining essential to its fragile recovery. For a country whose already weak economic growth is heavily dependent on domestic demand, this would therefore bode disaster, and not only for the individual citizens with affected bond holdings. |

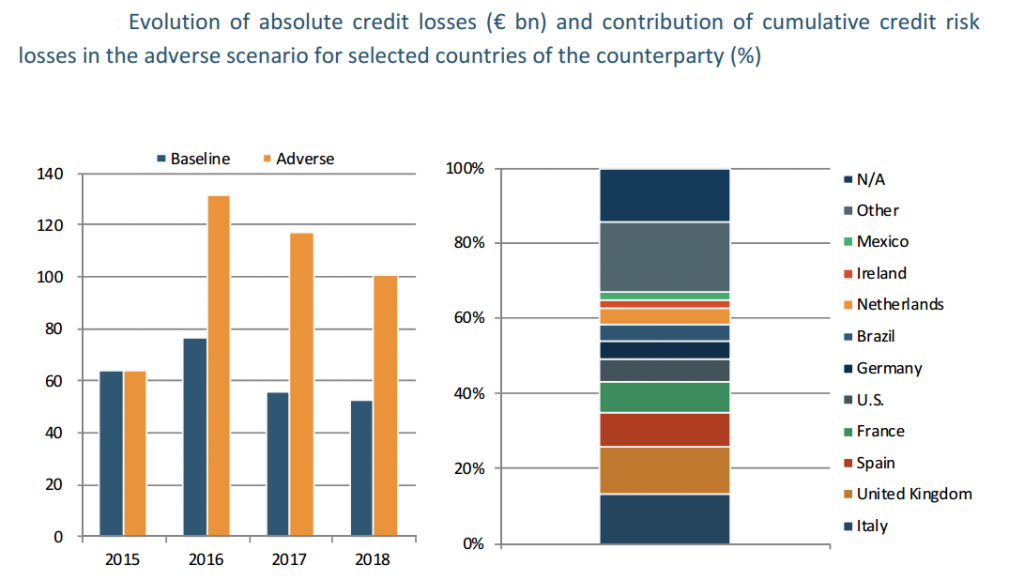

EBA Credit Losses Evolution of absolute credit losses and contribution of cumulative credit risk losses in the adverse scenario for selected countries of the counterparty (%) - Click to enlarge Estimate of aggregate absolute credit losses (in EUR bn.) of systemically important European banks under the EBA’s baseline and adverse scenario, plus effect on counterparty domiciles. The problem is that the “adverse scenario” isn’t a particularly adverse one, but rather a run-of-the-mill recession – click to enlarge.

|

Italy’s Banking Sector WoesThe Italian government is desperate to avoid any need for a bail-in, especially after the politically disastrous bail-ins of a handful of small regional banks last year. In this context, it has sought to reassure the markets that individual critical cases of weakness are contained and new capital can be raised without the need for individual investors to take a hit. But exactly how the overwhelming quantity of NPLs in the Italian banking sector will be dealt with is still far from clear. Italian banks have only made provisions to cover just under half of the 360 EUR billion NPLs weighing down their bank balance sheets, of which 210 EUR billion are already estimated by the IMF to be bad loans that will be irrecoverable. Plans such as that affecting MPS, where NPLs are to be offloaded into a securitization vehicle in an attempt to sell them to investors, would seem to be in line with the IMF’s recommendation that Italy build a robust market in NPLs. And yet many analysts consider such ambitions rather wishful thinking, especially since most of the bad loans on Italian bank balance sheets are uncollateralized loans to small businesses and consumers (in contrast to the mortgage NPLs that dominated Spanish and Irish bank balance sheets during their time of stress), and specialist NPL buyers tend to be more attracted to loans with easily recoverable, tangible collateral. Moreover, if Italy is to create a functioning NPL market, banks will need to accept significant write-downs on their loans compared to their current book value. There is a sizeable discrepancy between banks’ valuations of the NPLs and the price they would get for them if they attempted to sell off the loans to specialist distressed debt players, which will create yet more of a gaping hole on bank balance sheets. The small private Atlante fund and its successor Atlante 2, set up by the Italian government to help participate in distressed banks’ recapitalization and also to buy NPLs from banks, are unlikely to be anywhere near large enough to resolve these problems. |

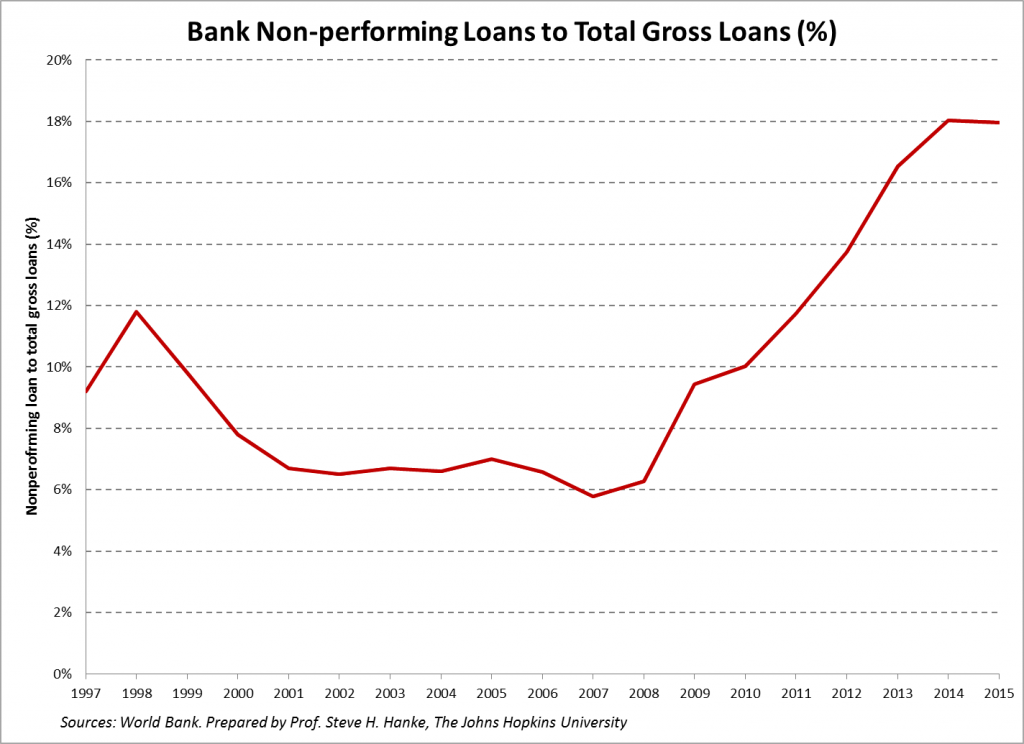

Bank Non performing Loans to Total Gross Loans Italian NPLs as a percentage of gross loans outstanding (as of 2015). The bulk of these non-performing loans have been extended in the economically extremely weak and Mafia-riddled South of the country and recoveries are likely to be very small - Click to enlarge |

Bailing in Retail Investors?To complicate matters further, holdings of bank bonds by retail investors are exceptionally high due to the longstanding practice in the country of selling (or rather mis-selling) bank bonds to ordinary citizens. An IMF report published back in July calculated that retail investors own about one third of around 600 EUR billion of senior bank bonds and nearly half of an estimated 60 EUR billion of subordinated bonds on the balance sheets of Italy’s 15 largest banks. Under the bail-in requirement of the EU’s Bank Recovery and Resolution Directive (BRRD) in force since the start of this year, at least 8% of a failing bank’s total liabilities must be written off before state aid can be requested, if the EU enforces strict adherence to the rules (the Italian government has been investigating every possible loophole in case). In Italy, the IMF estimates that this requirement would hit the majority of subordinated bond holdings by retail investors in the fifteen largest banks and that it would also hit some of their senior debt holdings in two thirds of those cases. After the experiences of massive publically-funded bank bailouts in countries such as the UK, Ireland and Spain during the height of the financial crisis, the whole idea behind the BRRD was to break the link between banking and sovereign risk and to stop putting taxpayers on the hook for private banking sector failures, making bank bondholders pay instead. But this assumes that the bondholders are institutional investors, and fails to take account of the specific circumstances of countries such as Italy where retail investors risk having their holdings wiped out too. In Italy’s case, many of the bank bondholders at risk are ordinary citizens and taxpayers, who were mis-sold bank debt as if it were as safe as placing their money in a savings account but with the added benefit of a much higher interest rate. In fact, retail investors are likely to be disproportionately affected compared to institutional investors, since individual citizens are usually sold more risky subordinated debt rather than its safer senior counterpart. |

Italian Stock Exchange Shareholders in Monte dei Paschi have essentially been wiped out. Bondholders are next in line. - Click to enlarge

Banca Monte dei Paschi’s share price has collapsed – and is reaching new lows almost daily. Bondholders are in the crosshairs now – the problem is, many of them are retail clients of the bank and have essentially been duped when the bonds were sold to them.

|

Recession Risk

Unless concrete plans for how to create a functioning NPL market are devised, it is unclear how banks that need to recapitalize will be able to do so without ultimately ending up hurting at least some of their equity and subordinated debt holders.

For a country where consumer spending is the cornerstone of an already weak recovery, imposing losses on retail investors, if they are not somehow exempted, would risk dampening consumer confidence to the extent that this could in itself push the country back into recession.

This is before the wider downside risk implications of a struggling banking sector are even taken into consideration. Even if a bail-in remains avoidable, if banks are forced to use their own precious reserves to increase loan-loss provisions and capital buffers in the absence of any substantial state aid injection, this risks prolonging the Catch-22 of poor growth leading to a weak banking sector and vice versa.

Charts by: BigCharts, Focus Economics, TradingEconomics, EBA, Steven Handke / John Hopkins University, 4-traders

Chart and image captions by PT

This article originally apperared as “The Italian Dilemma: Weak banks pose risk to already faltering domestic demand” at FocusEconomics.

Caroline Gray is the Senior Economics Editor at FocusEconomics. She specializes in politics and political economy. She recently completed a PhD on regional financing and nationalist politics in Spain, funded by the Economic and Social Research Council. Previously, she spent three years (2010-2012) reporting on the financial crisis in Spain for government departments and then private sector clients, first as a Political and Economic Officer at the British Embassy in Madrid and subsequently as a financial reporter responsible for covering Spain at a fixed income intelligence service (Debtwire) within the Financial Times Group. She has also worked as a freelance translator (Spanish-English) and copy editor for think tanks on international affairs. She graduated from the University of Oxford with a First Class degree in Modern Languages (French and Spanish).

Full story here Are you the author?

Tags: Euro area,Euro Stoxx bank index,Italy Gross Domestic Product,newslettersent,On Economy