Addicted to SpendingThere are many falsehoods being perpetuated these days when it comes to money, financial markets, and the economy. But when you cut the chaff, three related facts remain: Uncle Sam needs your money. He needs a lot of your money. And he needs it bad! |

The inescapable logic of tax & spend: empty vault… empty pockets… gimme more! PT |

| According to the Congressional Budget Office, the federal budget deficit for the first two months of fiscal year 2020 is $342 billion. This amounts to $36 billion more than the deficit recorded during the same period last year. At this rate, Washington is going to add over $1 trillion to the national debt in FY 2020.

Still, the figures from the CBO aren’t all bad. Revenues in October and November of 2019 were 3 percent higher than they were in October and November of 2018. Regrettably, outlays for these two months were 6 percent higher in 2019 than they were in 2018. Jacks and Jennets both know from experience that taking three steps forward and six steps back is an inefficient way to lose ground. They also know that the longer this goes on the more ground you lose. So, too, they know that the more ground you lose the harder it is to make up. For example, after the big three budget items – Medicare, Social Security, and Defense – comes Interest on Debt. Presently, Interest on Debt is over $375 billion. However, the debt is growing by over $1 trillion a year. By this, the Treasury is losing ground. Moreover, when interest rates rise, and as the pile of government debt approaches $40 trillion over the next decade, interest on the debt will quickly jump to well over $1 trillion. This will put merely the interest on debt at par with expenditures for Medicare and Social Security, and well above Defense. This is why Uncle Sam needs your money. But how he gets your money is a recipe for disaster… |

Federal Outlays: Interest, 1974-2019 The US Treasury’s outlays for interest have soared despite historically low bond yields [PT] - Click to enlarge |

Dotards AnonymousPresident Trump doesn’t want to raise taxes, especially in an election year. He wants to cut taxes. Because voters love tax cuts… so long as they are not for the rich. The proven method for a Presidential incumbent to stay in office is to cut taxes and increase spending. And this is precisely what Trump is doing. Spending is increasing two times faster than revenue. So how will Uncle Sam get your money? He will get it by doing more of what he is already doing. He will get it via greater and greater deficits. When Fed expands the money supply through monetizing debt it effectively dilutes wealth from the dollar. But for Uncle Sam it doesn’t matter if the dollar is watered down to a lite beer. He gets the newly created money first. And he gets to spend it while the money can still lay claim to real labor and resources. John Maynard Keynes succinctly clarified:

In practice, the increase in the money supply leads to a reduction in purchasing power per monetary unit. So, without levying taxes, Washington confiscates your wealth – your stored time and productivity – in return for debased money. Still, this doesn’t solve the problem of taking three steps forward and six steps back. Instead, it makes it worse. As the nation ages, and the interest on the debt consumes more and more of the budget, the economy weakens like an anonymous dotard. Yet this isn’t the half of it… |

A habit impossible to kick… [PT] |

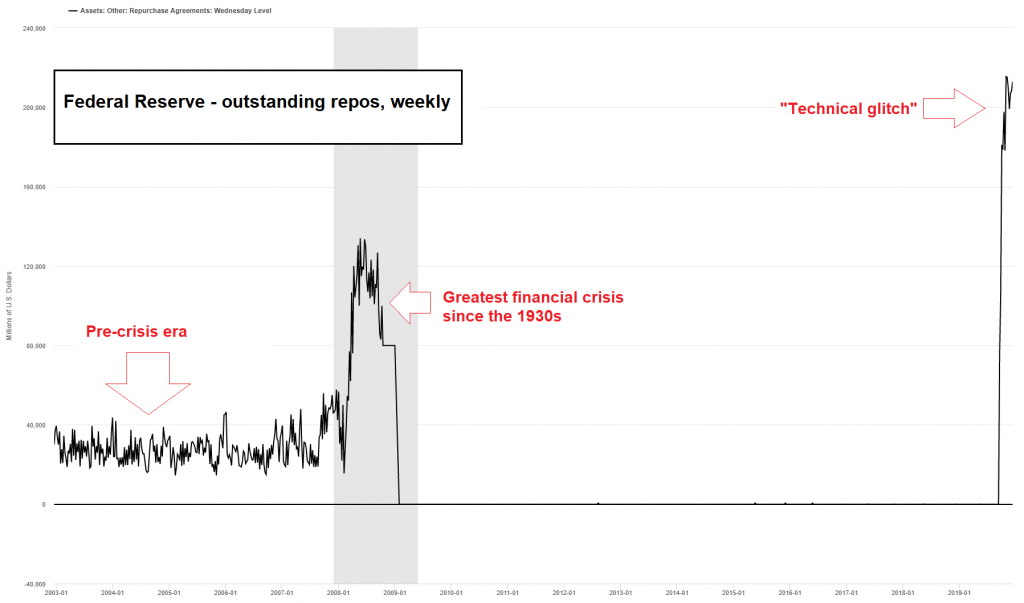

Banana Republic Money Debasement In AmericaYou see, the US debt-based fiat money system, which is dependent on greater and greater issuance of Fed credit, is set up for ultimate failure and disaster. Yet, the road to this endgame, as we discover more and more every day, is paved with madness. This week, for example, the Federal Reserve Bank of New York published their latest schedule of overnight and term repurchase agreement operations. This, in short, lays out how much fake money they are going to print up and give to the big banks through January 14, 2020. Cutting through the minutia, and tabbing it up, is mind-numbing. Fortunately, the astute fellows at Zero Hedge were up to the task:

|

Federal Reserve - outstanding repos, weekly 2003-2019 This chart is soon going to become even more interesting, as the Fed is trying to forestall a year-end liquidity crunch in the repo markets (and elsewhere) by massively increasing its repo operations further at the turn of the year. [PT] - Click to enlarge |

| This, without question, constitutes mass money debasement of the likes typically reserved for banana republics. Somehow we think all this funny money is needed to keep the U.S. Treasury flush with cash.

Moreover, if this $500 billion madness is needed just to get to January 14, what madness will be needed come January 15? Our guess: Take the current number and double it. Then double it again.

Charts by St. Louis Fed

Chart annotations and image captions& editing by PT |

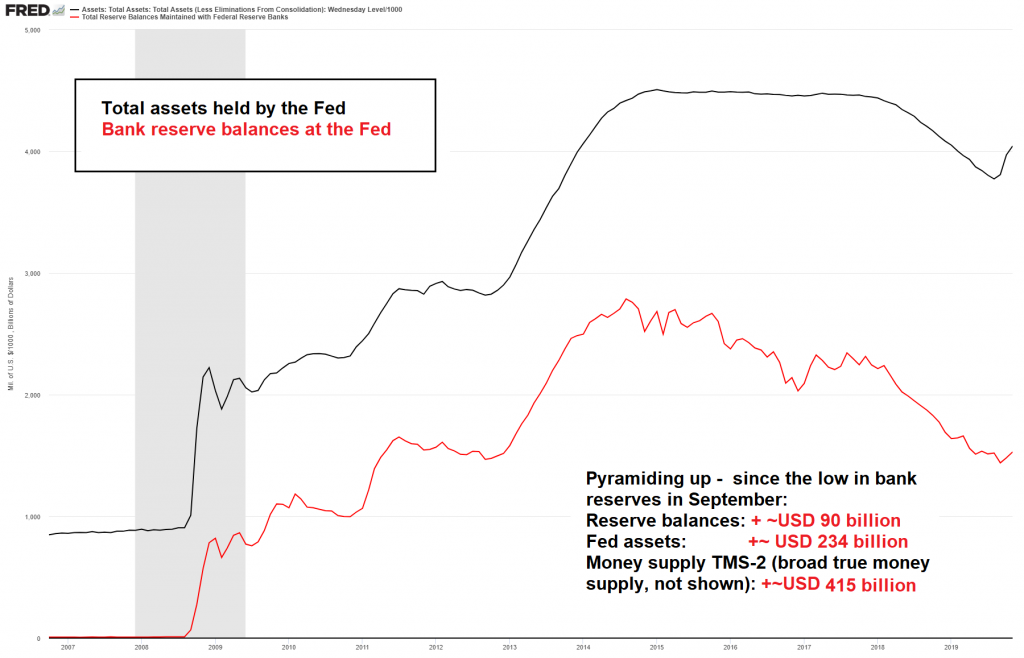

Total assets held by the Fed, 2007-2019 - Click to enlarge The problem in a nutshell: since the interim low in bank reserves in September, the resumption of QE (or rather, “not-QE”) has so far boosted assets held by the Fed by USD 234 billion and the broad true money supply TMS-2 (not shown on the chart) by USD 415 billion. However, bank reserves have only grown by slightly less than USD 90 billion, reportedly because the Fed has focused on purchasing t-bills rather than the longer maturities predominantly held by banks. Whatever the reason, this USD 90 billion addition to bank reserve balances is apparently held to be insufficient to get the system across the traditional turn-of-the-year liquidity crunch. While this is officially shrugged off as a mere technicality, this can hardly be considered a stable situation. In fact, it is slightly reminiscent of the initial emergency liquidity injections in late 2007/early 2008 – readers may recall that these were also characterized as temporary technical aberrations. Not long thereafter, the aberrations became a permanent feature of the monetary landscape. [PT] |

Tags: central-banks,newsletter,On Economy,On Politics