Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

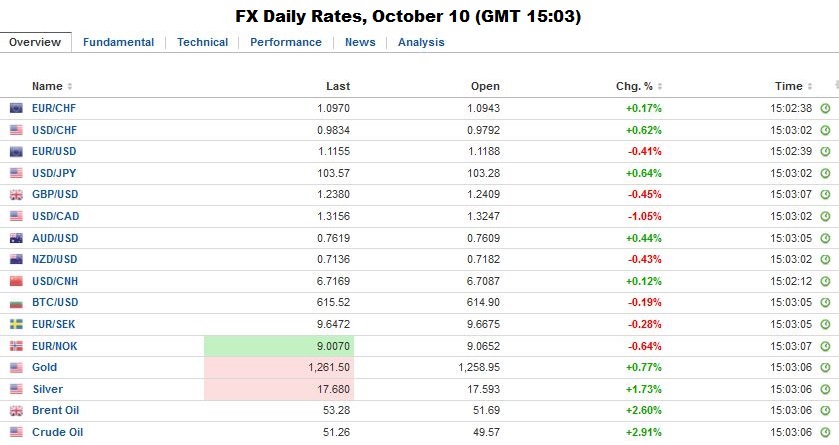

Swiss Franc |

EUR/CHF - Euro Swiss Franc, October 10 2016(see more posts on EUR/CHF, ) - Click to enlarge |

FX RatesThe US dollar has started the new week on a firm note. The light news stream and holidays in Japan, Canada and the United States make for a subdued session. Notable exceptions to the dollar’s gains are the Canadian dollar and Mexican peso. Both currencies appear to have been. underpinned by US political developments, the main feature of which is the implosion of the Trump campaign.

Many Republican officials retracting their support and a smaller number are calling for Trump to step down. This does not seem likely, though Trump’s pre-debate and debate tactics are unlikely to expand his support. Indeed, as we suggested nearly six weeks ago, it is more likely that the Democrats win control the legislative branch than Republicans capture the White House.

Lastly, over the weekend, BOJ’s Kuroda hinted that the achieving the inflation target may be postponed again. It has already been pushed out four times. Doing so again may amount to admission of failure as Kuroda’s term is expires April 2018. Kuroda cited cheaper oil and a decline in inflation expectations as the culprit. Many observers suspect that the modifications of the QE and the targeting of the yield curve makes it less likely that the BOJ will move again in Q4.

|

|

|

The dollar found a bid near JPY102.80. The immediate cap is seen in the JPY103.30-JPY103.60 area. A move above there will target last week’s high near JPY104.15 and the September high around JPY104.30.

The euro pushed to $1.1210, marginally extended the pre-weekend recovery, but its met good offers which sapped its residual strength. Initial support is seen in the $1.1145-$1.1155 area. A break of there puts it back to the $1.11 area seen briefly before the weekend, which is also the lowest level in nearly two months. The US employment was not deemed strong enough to overcome tradition of not changing rates close to a national election, and the logistic challenge of having an ad hoc press conference without it being leaked. However, the pricing of the Fed funds futures suggest, if anything, a slightly greater chance of a December hike.

|

- Click to enlarge |

|

Sterling, which fell victim to a flash-crash of sorts before the weekend, has stabilized around $1.24. Developments over the weekend in the UK warned of the risk of a constitutional crisis as the House of Common seeks a greater role in the Brexit decision and negotiations. Prime Minister May argued that the strong support (6 to1) for the referendum was their sanctioning of the outcome, and that it now is a ploy to thwart the will of the people. There is talk that Labour’s Miliband and Tory MPs may seek a possible alliance on this issue.

Separately, but related, the government appears to have backed away from requiring companies to publicly reveal the number of foreign workers on their payrolls. Apparently, the information, collected by the government ostensibly to identify skill shortages, will remain confidential.

|

- Click to enlarge |

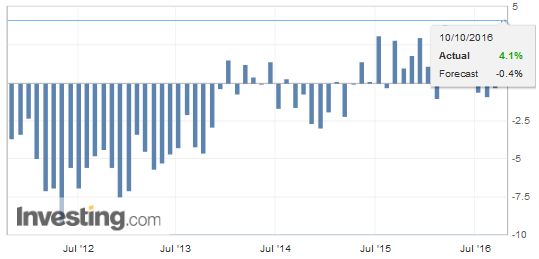

EurozoneThe news stream is light. The only economic data of note is Italy’s industrial output figures. Consistent with the pattern seen last week when Germany, France, and Spain beat expectations, Italian industrial output jumped in August. The 1.7% increase compares with the median forecast of a 0.1% decline. The year-over-year, workday adjusted pace surged to 4.1%. The median guesstimate was for a 0.3% decline.

Some may suggest that on the margins, stronger economic data is favorable for Renzi and his constitutional referendum. We are less sanguine. The referendum may not be judged strictly on the merits of the reform of the Senate, but on Renzi’s government in general. While a jump in industrial output sounds good, it does not make up for the fact that just last week the IMF downgrade Italy’s growth prospects to 0.8% this year and 0.9% next.

Deutsche Bank stock is snapping last week’s four-day advancing streak, with a nearly 2.4% loss today. The lack of a compromise with the US Justice Department, contrary to rumors a week ago, appears the main culprit. The weaker share price comes despite reports that the Qatar royal family may be interested in boosting its stake in the bank to 25% from around 10% presently. The drop in the share price of Germany’s largest bank is weighing on European financials more broadly. The Dow Jones Stoxx 600 is little changed, but the financial sector is off 0.5% near midday in London.

|

Italy Industrial Production YoY, September 2016(see more posts on Italy Industrial Production, ) Source: Investing.com - Click to enlarge |

| Deutsche Bank stock is snapping last week’s four-day advancing streak, with a nearly 2.4% loss today. The lack of a compromise with the US Justice Department, contrary to rumors a week ago, appears the main culprit. The weaker share price comes despite reports that the Qatar royal family may be interested in boosting its stake in the bank to 25% from around 10% presently. The drop in the share price of Germany’s largest bank is weighing on European financials more broadly. The Dow Jones Stoxx 600 is little changed, but the financial sector is off 0.5% near midday in London. |

Germany Trade Balance, September 2016(see more posts on Germany Trade Balance, ) Source: Investing.com - Click to enlarge |

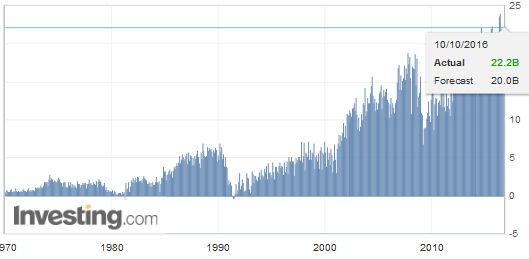

Japan Adjusted Current Account |

Japan Adjusted Current Account, August 2016(see more posts on Japan Current Account, ) Source: Investing.com - Click to enlarge |

United Kingdom

We note that UK rates continue back up. This is different than what was seen in Q3. The weakness of sterling came along lower interest rates. The rise in UK rates is not simply a function of fading hopes of a rate cut next month, but rather a recognition that sterling’s fall will boost inflation. If prices rise faster than wages, the UK current account deficit may indeed fall, but it may note be so much because of exports but a decline in imports and a compression of domestic demand.

Graphs and additional information on Swiss Franc by the snbchf team.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: #GBP,#USD,$CAD,$EUR,$JPY,Deutsche Bank,EUR/CHF,FX Daily,Germany Trade Balance,Italy Industrial Production,Japan Current Account,MXN,newslettersent