Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Swiss FrancThe EUR/CHF has soared again. Later during the day, it has even achieved 1.0970. |

EUR-CHF - Euro Swiss Franc, October 04 2016 . - Click to enlarge |

Federal Reserve

|

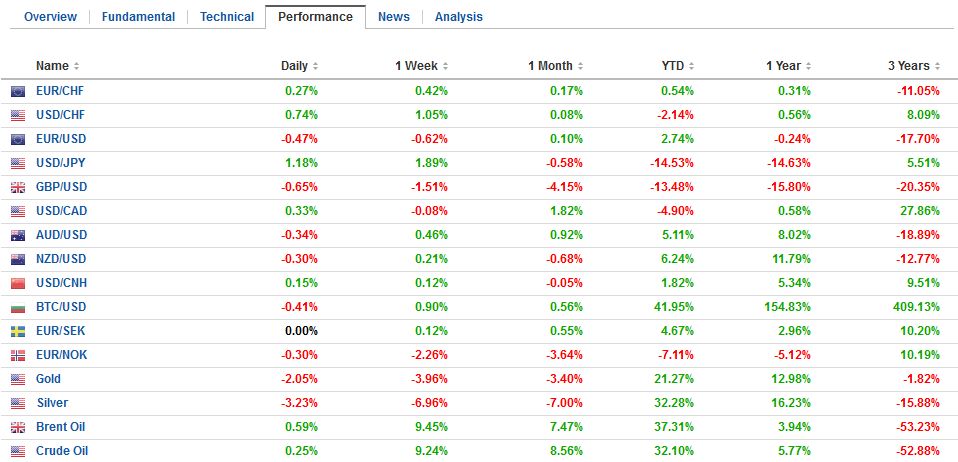

FX Performance, October 4, 2016 Source Dukascopy. - Click to enlarge |

| Sterling’s decline is not coinciding with lower interest rates. UK shares though are doing well. This is not surprising for the FTSE 100, where the significance of foreign earnings make this a currency play, but the FTSE 250 and FTSE 350 are performing slightly better than the FTSE 100. Industrial are the strongest sector, followed by telecom and information technology.

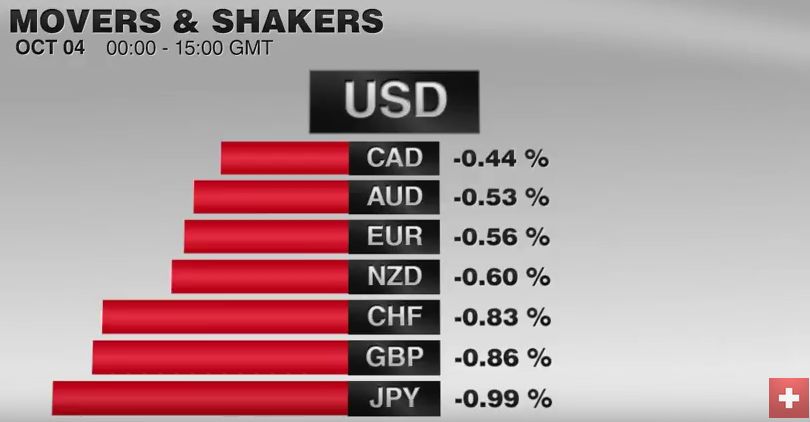

That said, sterling is not the weakest currency on the day. It is the yen today. Quietly the dollar has strung together a six-day advancing streak against the yen. The greenback had spent the last two sessions consolidating, and today, exploded out the little triangle to push to JPY102.50, the highest since September 21. The dollar has risen through a trendline that began in late-May, caught the July and September highs. It came in near JPY102.00 today. The next hurdles are seen near JPY102.80 and JPY103.35. |

FX Daily Rates, October 04 (GMT 15:00) . - Click to enlarge |

| The Reserve Bank of Australia met earlier today for the first time under Governor Lowe. There were no surprises. The cash rate was unchanged at 1.50%. There was a dovish tilt. Rates on hold for the remainder of this year and scope for a rate cut next year. The Australian dollar is made a three-day high before consolidating within striking distance of the $0.7700 cap that has proved so frustrating for the bulls over the past couple of months.

Gold is lower for the sixth consecutive session. This streak follows a six-session advance. It leaves the precious yellow metal near the low end of its recent range, just above $1300. It has not traded below there since late-June. |

FX Performance, October 04 (GMT 15:00) . - Click to enlarge |

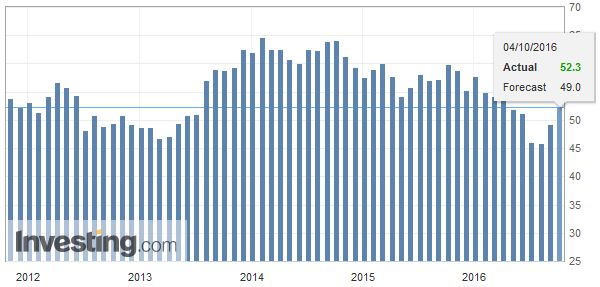

United KingdomThe UK construction PMI jumped to 52.3 from 49.2. The Bloomberg median anticipated further weakness. In snaps a three-month streak of below 50 (boom/bust) readings. The manufacturing PMI reported yesterday was also stronger than expected. Tomorrow, the service sector PMI will be reported. The median forecast is for a decline, and the same is true for the composite. The risk on both is to the upside, though sterling may be less sensitive to short-run economic data as anxiety over the other shoe dropping in six months is palpable. |

U.K. Construction PMI, October 2016(see more posts on U.K. Construction PMI, ) Source Investing.com - Click to enlarge |

EurozoneThe euro is also under pressure. Recall that before the weekend; it had approached support near $1.1150 before AFP reported about a compromise over Deutsche Bank’s fine. The euro is slipped back toward there despite Deutsche Bank’s stock is higher today after yesterday’s unification holiday. The shares dipped below 10 euros tat the end of last week and reached almost 12 euros today. The $1.1150 support may fray today. Additional support is seen near $1.1120. The euro will likely struggle to stage much of a recovery ahead of tomorrow’s service PMIs in Europe and the US ADP job estimate. On the other hand, the Dow Jones Stoxx 600, the index of European large cap companies has a six-day streak to the upside, with today’s 0.75% gain, led by materials and energy sectors. Asian shares moved higher but were more restrained. The minor 0.2% increase, however, masks the breadth, as all markets were higher, though Chinese markets are still closed for the week-long national holiday. The equity market gains are not preventing a firmer tone in bond markets. Yields are mostly lower. Portugal is playing a bit of catch-up today as its 10-year yield slides eight bp. DBRS is set to review Portugal’s rating later this month. It is the only major rating agency that grants the country investment-grade status. If it were to lose this, it would disqualify the use of government bonds as collateral for borrowing from the ECB and their inclusion in QE. This seems like a greater risk than what many observers focused on, and that is the Italian referendum in December. It is true that Portugal does not pose the contagion risk of a fall of the Italian government. However, it seems clear that Italian Prime Minister Renzi will not step down, a la Cameron if the reform of the Senate is rejected. |

Eurozone Producer Price Index, October 2016(see more posts on Eurozone Producer Price Index, ) Source Investing.com - Click to enlarge |

United States

Many observers are attributing the firmer dollar tone to comments by Cleveland Fed President Mester, who had dissented in favor of a hike at last month’s FOMC meeting. We are sympathetic to her arguments, but we cannot follow her in claiming a rate hike is compelling in November. In most circumstances, we could, but what is unusual about the November meeting is that it is a week before the national election. There is precedent to move rates in September and December of election years but not November. Given the power of this tradition, a violation would require near emergency like conditions. That is not the case.

Bloomberg’s calculation shows about a 17% chance of a hike in November. The CME puts it near 10%, and our calculation is a little lower. Moreover, Mester was the only Fed official to speak yesterday. NY Fed President Dudley did too, and he sounded cautious. On balance, our understanding of the decision-making dynamics gives more weight to Dudley than Mester.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?

Tags: #GBP,#USD,$AUD,$EUR,$JPY,Eurozone Producer Price Index,FX Daily,newslettersent,U.K. Construction PMI