Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

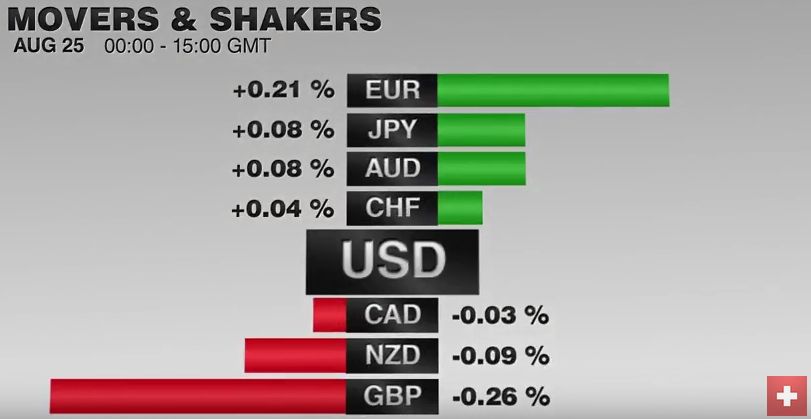

Swiss FrancEUR/CHF rose by 0.2% to 1.0919 despite SNB interventions in last week. |

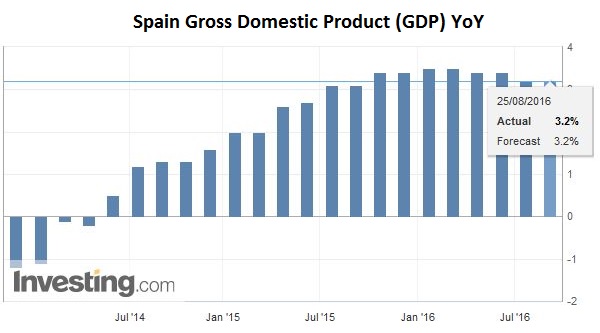

Spain Gross Domestic Product Click to enlarge. Source Investing.com |

Federal ReserveThe US dollar remains mostly within the ranges seen yesterday against the major currencies.The market awaits fresh trading incentives and the end of the summer lull, which is expected next week. The Jackson Hole Fed gathering at which Yellen speaks tomorrow is seen as the highlight of this quiet week. Two of the three Fed leaders have already provided their general take on the economic outlook and prospect for a Fed hike this year.It seems unreasonable to expect Yellen substantially deviate, to the extent that she deals with immediate issues as opposed to addressing the topic of the title of the symposium: “Designing Resilient Monetary Policy Frameworks for the Future.” |

Click to enlarge. |

| Although a September hike seems unlikely, there is nothing to be gained from Yellen ruling it out. The Fed wants investors to know that every meeting is actionable, though there is no precedent for a move in November the month of the national election. According to the Fed funds futures, the market has upgraded the odds of a Sept hike to 28% as of yesterday from 18% on August 1 and 26% on August 5 after the US jobs data.

The market has taken the news in stride. European shares are broadly lower today, with the Dow Jones Stoxx 600 off around 0.5%, to stop a three-day rally, and banks shares are slightly lower. Portugal’s bourse is off slightly (~0.15%), and bank shares are slightly firmer. The yield on Portugal’s sovereign 10-year benchmark is a single basis point higher, in line with other European bond markets today. |

Click to enlarge. |

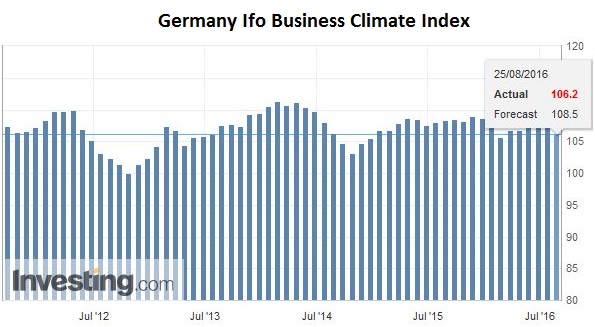

GermanyThere are two other talking points today. First, the Germany IFO survey was weaker than anticipated. The market has largely shrugged it off. Investors may not be as forgiving if next month’s survey does not show any improvement. The overall measure of the business climate fell for the second consecutive month. The 106.2 reading is the lowest since February and compares with a 107.7 average in Q2 and 106.7 average in Q1. The business climate is a function of the current assessment and expectations. The current assessment was downgraded to 112.8 from 114.8. It is the lowest level since January. The expectations component also fell for the second month, and at 100.1 (down from 102.1) is the lowest since February.

|

Germany IFO Business Climate Index(see more for Germany IFO Business Climate Index)  Click to enlarge. Source Investing.com |

Portugal

The second talking point is news that Portugal has struck reached an agreement with the EU on a 2.7 bln euro injection of public money into its largest bank by assets (Caixa Geral). It is already state-owned, and the government’s 960 mln euro investment in the bank’s contingent convertible bond will, in fact, be converted to equity and the bank will look to raise another one billion euros through the sale of new debt.

There are several flashpoints in the emerging markets, but there is limited impact on the broader markets. First, the South African rand is recovering after yesterday’s shellacking spurred by an investigation that appears to have ensnared Finance Minister Gordhan. President Zuma, which has been at loggerheads with Gordhan expressed confidence in him today. Second, Turkey has begun military operations in Syria. The lira appeared to weaken on the news yesterday but is also recovering today.

North Korea’s launch of a missile from a submarine represents a new display of its capability. South Korean stocks recovered most of their initial losses today after testing the Kospi tested its 20-day moving average for the first time in a couple of weeks.Taiwan shares rallied a little more than 1%, the most since early-July. Foreign demand was noted (~$250 mln). Taiwan equities have drawn foreign inflows all year. Through today, some $2.27 bln of Taiwanese equities have been bought by foreign investors this month. This compares with foreign purchases of $1.26 bln of South Korean shares.

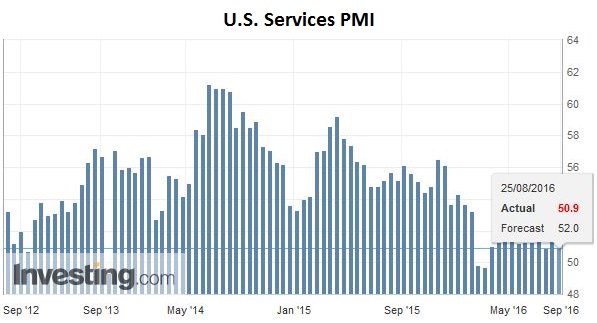

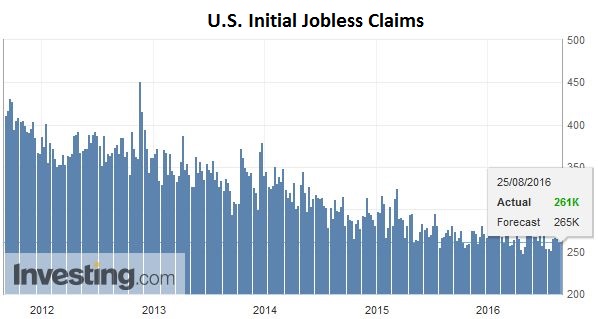

United StatesU.S. Services PMIThe US economic calendar features the weekly jobless claims, durable goods orders, the Markit service PMI and the KC Fed manufacturing survey. |

U.S. Services PMI(see more for U.S. Services PMI)  Click to enlarge. Source Investing.com |

U.S. Core Durable Goods OrdersThe durable goods orders may be the most important, and have impact on Q3 GDP forecasts. |

U.S. Core Durable Goods Orders(see more for U.S. Core Durable Goods Orders)  Click to enlarge. Source Investing.com |

U.S. Initial Jobless ClaimsA modest improvement is expected, including in shipments. Whether it is sufficient to break the market’s doldrums is a different story. |

U.S. Initial Jobless Claims(see more for U.S. Initial Jobless Claims)  Click to enlarge. Source Investing.com |

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #USD,$EUR,FX Daily,Germany IFO Business Climate Index,newslettersent,U.S. Core Durable Goods Orders (ZH),U.S. Initial Jobless Claims,U.S. Services PMI