Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

European Court of Justice could rule on July 19 that private investors do not have to be bailed in before public money can be used to recapitalize banks.

Italy stands to gain the most, at least immediately, from such a judgment.

Italian bank shares recovered after initial weakness.

After the 2007-2008 bank recapitalization by governments, which means taxpayers’ money, Europe changed the rules. The new rules require that private investors are “bailed in” before the bank is “bailed out.”

After the 2007-2008 bank recapitalization by governments, which means taxpayers’ money, Europe changed the rules. The new rules require that private investors are “bailed in” before the bank is “bailed out.”

Europe’s fastidious with rules allows for exceptions and flexibility. Italy is pushing for this flexibility now, and Portugal is watching closely because its largest bank also may require recapitalization.

However, there is another source of relief is a little more than a week away. On July 19, the European Court of Justice will hand down its ruling on 2013 case brought to it by Slovenia over its bank bailout. The Advocate General made a preliminary judgment in February. The European Court of Justice upholds that Advocate General 80% of the time, according to reports.

So what did the Advocate General say? Essentially he threw shade on the Bank Recovery and Resolution Directive that forces private investors to take losses before public money can be provided. The Advocate General argued that the EC has not binding powers on this issue and that bailing in investors is not a prerequisite to using of government aid. The EC, according to the Advocate General, cannot force losses on private investors.

The Bank Recovery and Resolution Directive (BRRD) outlines the process of recapitalizing banks with state money. Its flexibility allows for state funds to be used if the ECB’s stress test reveals the need for capital infusion and the country is in serious economic trouble. Italy first tried to claim “exceptional circumstances” post-the UK referendum, that would have been widely applicable to EU members. It required unanimity and German quickly blocked it. Now Italy is negotiating its own exemption.

The issue is not whether the state funds can be used, but who must take losses first. In Italy, nearly half of the bank bonds were reportedly sold to retail investors. Bailing them in as investors risks hurting the fragile economy further through consumption. Also, they are taxpayers. So the logic of BRRD would be to hit them as imprudent investors before forcing them as taxpayers to capitalize the bank. These investors are not only consumers but also voters.

The Italian referendum in October is the next major political challenge in Europe. The referendum is about constitutional changes to reduce the size and power of the Senate. Although Prime Minister Renzi does not want to be so, voters may use the referendum as a vehicle to express their opinion about the third unelected Prime Minister rather than the merits of the issue.

If the referendum loses, which appears likely now according to polls, Renzi has indicated he would resign. Polls also suggest that the Five Star Movement (M5S) has replaced Renzi’s PD as the biggest party in Italy. The M5S appears to have softened its anti-EU stance, but it still appears to support a referendum on EMU membership. The bottom line is that if the referendum losses and Renzi resigns, Italian politics potentially would be a significant disruption.

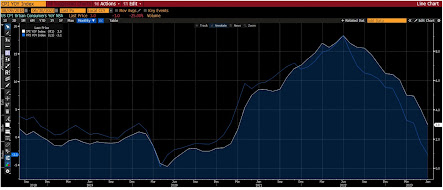

The market seems to be sensing that the tide is turning in Italy’s favor. Between the European Court of Justice, which would de-fang the BRRD (July 19) and the ECB’s stress tests (July 29), that Italian banks will get the support they need. It is too early to tell whether the condition of the aid will be putting some closure of the NPL problem that is saddling several Italian banks. The Italian bank shares index initially retreated today after the 9.7% rally before the weekend. It managed to close higher on the day.

Full story here Are you the author?

Tags: Bailout,Bank-Recapitalization,Five Star Movement,Italy,Matteo Renzi,newslettersent