Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary:

FOMC statement will not likely close door on September hike, though economists are more inclined for a December move.

There is great uncertainty surrounding the BOJ’s outlook. We suspect odds favor tweaking assets being purchased rather than cutting rates further or dramatically increasing JPY80 trillion balance sheet expansion.

European bank stress test results due at the end of the week.

Contrary to conventional wisdom, we think monetary policy remains an important variable for asset prices. Interest rates and foreign exchange are two dimensions of the price of money. There is a relationship, even if it is not linear or temporally consistent.

Contrary to conventional wisdom, we think monetary policy remains an important variable for asset prices. Interest rates and foreign exchange are two dimensions of the price of money. There is a relationship, even if it is not linear or temporally consistent.

Moreover, as a great discounting mechanism, the markets often price in the likelihood an event before it happens. In our day-to-day lives, causes take place before the effects by definition, but in the markets, sometimes, the effect comes place before the cause. The effect was selling yen since earlier this month, for example, and the cause is the Bank of Japan meeting on July 28-29.

A couple of days before the BOJ meets the Federal Reserve Open Market Committee will gather. While there is much uncertainty about what the BOJ will do, there is great confidence in the outcome of the FOMC meeting–nothing. This does not mean that the meeting is unimportant.

As you know, our understanding of the Federal Reserve places a heavy emphasis on the leadership: the Chair Yellen, Vice-Chairman Fischer, and the NY Fed President, who unlike the other regional Fed Presidents, has a permanent vote on the FOMC. The FOMC minutes are more comprehensive than the FOMC statement. They report on the views of voting and non-voting members, regional presidents and governors, and therefore the dilute the signal emanating from the leadership.

The statement that follows an FOMC meeting is among the cleanest expressions of the views of the Fed’s leadership. It is crafted by the leaderships though may be written in way to ensure support of as many voting members as reasonable. Dissents by Governors are rarer and understood to be more significant than dissents from regional Presidents,whose qualification for office is not economic or acumen.

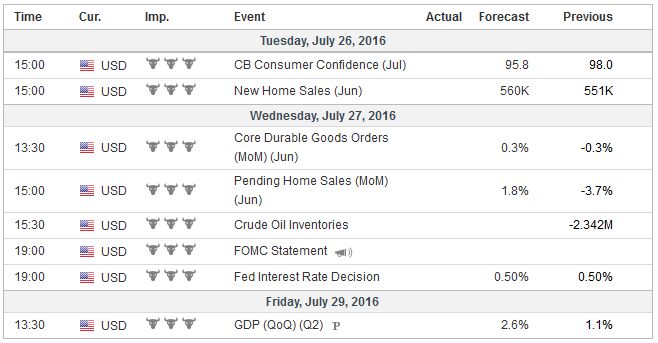

The FOMC statement is likely to recognize that since the June meeting the economy has evolved largely in line with what the Fed expected, or hoped for, as the case might be. Nearly every piece of economic data since late-June have been better than expected. This includes the non-manufacturing ISM, job creation, retail sales, industrial and manufacturing output, and existing home sales. Headline and core CPI were also firmer than anticipated.

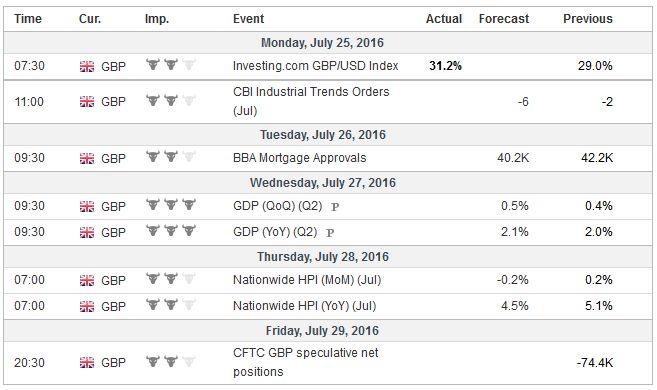

United KingdomThe statement is likely to recognize the resilience of the capital markets since the UK referendum. Many equity markets, including the US benchmarks, have made new highs. The drop in long-term bond yields have not fully recovered but have stabilized and the 10-year breakeven has returned to levels above the 1.50% that were seen a week before the UK referendum. Meanwhile, the yuan, which was a source of investor angst last summer, is no longer driving the capital markets, even though its depreciation is larger and its equity market is among the worst performers this year. On balance, the FOMC statement is unlikely to say anything that closes the door on a September move. It wants to keep the market on notice that as the Fed’s objectives are approached, gradually removing accommodation is appropriate. The data dependent stance seems to mean the alignment of three stars: continued improvement in the US labor market, favorable consumption patterns, and a stable international environment. A recent Reuters poll found about half of the 100 economists surveyed expect a hike in Q4, which really means December since the November meeting is too close to the national election. The other half is split between a Q3 rate hike (September) and some time in 2017. That said, two primary dealers anticipate no hike until the end of 2017. A couple days after the FOMC meeting, the first estimate of growth in Q2 will be released. The median forecast in the Bloomberg survey is 2.6%. The NY Fed GDP tracker puts it at 2.2% as of July 15 and the Atlanta Fed tracker say 2.4%. Given that the economy appears to have gained momentum as Q2 came to a close, we suspect the risk is softer than expected growth that gets revised up, as was the case with Q1 GDP, where the final estimate was more than twice the initial projection. The UK and the eurozone also provide initial estimates of Q2 GDP. Growth in the UK was remarkably stable in the period leading up to the referendum. The median guesstimate from the Bloomberg survey is 0.5% (quarter-over-quarter) after a 0.4% pace in Q1. In contrast, the eurozone economy is expected to have slowed markedly from the heady 0.6% quarter-over-quarter expansion in Q1, which is understood to be above trend, to 0.3% in Q2. |

Click to enlarge. |

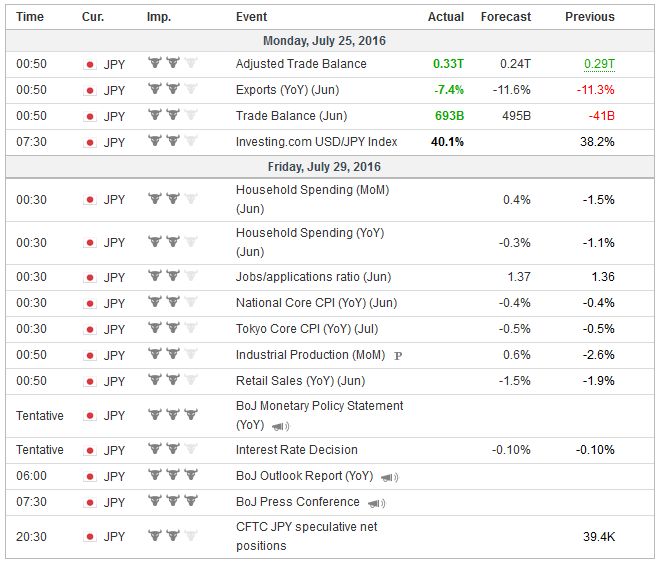

United StatesOverall household spending, comparable to the US personal consumption expenditure, is expect to have remains in negative territory in June. In a fact, with the exception of February 2016 and August 2015, household spending in Japan has been contracting on a year-over-year basis since last May. Industrial output may have edged higher in June (~0.5%) after a sharp (2.6%) drop in May, but the year-over-year rate remains negative, as it has since September 2014 (with three exceptions, March 2016, and June and November 2015). The latest readings on inflation will also be available. Simply put, the aggressive expansion of the BOJ’s balance sheet has not lifted consumer prices, and it is not clear that the asset purchases are even lifting the price of those assets. Headline CPI in Japan will likely stand at minus 0.4% at the end of H1 16, as will the measure for which the BOJ ostensibly targets, which excludes fresh food. Even when energy is also excluded, the core rate is expected to be near 0.5%, having peaked last November near 0.9%. We noted that the US 10-year breakeven stands at 1.5%. Japan’s is at 0.35%. The Nikkei has been trending lower since June 2015 and by last month it had fallen nearly 28%. The recent two-week 12.5% rally appears to have been driven by expectation of fiscal stimulus, for which the whisper number has tripled from JPY10 trillion to JPY30 trillion, and the speculation of “helicopter money”. Economists and policymakers define helicopter money differently. At is essence is a central bank creating credits and using the credits to give to economic agents, including the government directly. It bypasses the normal channel of injected funds through various means to the banks who then allocate it |

Click to enlarge. |

JapanThe Bank of Japan’s two-day meeting concludes on July 29. As the meeting begins, Japanese officials will be reminded of the state of the economy. Despite a relatively tight labor market in terms of a low unemployment rate and a high jobs-to-applicant ratio, consumption remains poor. The Federal Reserve did not refer to its asses purchases as quantitative easing. The market did. Similarly, the BOJ does not consider its current aggressive monetary stance “helicopter money” but some in observers do. The magnitude of its purchases of government bonds arguably blurs the distinction between monetary and fiscal policy. The fact that banks disintermediate the process, and seem to be less inclined to do so, does not alter the consequences. It is a necessary legal veil. It is currently important because it means that the idea, spurred perhaps by Abe-advisor Honda, of the BOJ buying non-marketable perpetual bonds from the Japanese government, which has captured the imagination of many, is not legally possible. Kuroda stated as much in the mid-June interview that was recently aired, and which he reiterated at the weekend G20 meeting. The BOJ’ s stance has three dimensions, the quantity of assets being purchased, the quality of those assets (hence QQE) and interest rates. A rate cut, putting the deposit rate into deeper negative territory, or including a greater amount of deposits into the negative rate category would be an affront to Japanese banks, who argue it is disruptive. The experiment with negative rates has been fascinating but it has not yielded the desired results, but it has weakened the financial system and inflicts a hardship on the elderly. Increasing the quantity of assets being purchased is possible, but the current pace of JPY80 trillion is aggressive in at least two ways. The first is relative to the what other central banks did relative to the size of the underlying economy and second is relative to the market. While much of the focus on the shortage of assets has been in Europe, BOJ purchases are creating liquidity distortions. That leaves the quality of the assets that the BOJ purchases to be the least disruptive dial to turn. ETF purchases, for example, may be an attractive place to pump with newly created central bank credits. There may be scope in some of the other asset classes the BOJ buys to tweak a little. Of course, it is difficult to have much confidence in predictions of what the Kuroda will do. He himself might not know. We suspect the risk is greater that Kuroda disappoints expectations rather than announcing another large burst of monetary stimulus. We are also concerned that the fiscal plans may disappoint as well. It is a bit like the pufferfish that makes itself look bigger to its adversaries if not its friends. In Japan, the custom is to include in the package other programs whose funding has already been earmarked, which inflate the apparent size of the stimulus. Also no distinction is made between programs in which the funds must be paid back (like Fiscal Investment and Loan Program, FILP). That this distinction between the announcement and real new spending is evidenced by the fact that in the Japanese vernacular it has a name: “mamizu” or “freshwater”. When the fiscal plan is announced, there will be some short-term headline risk, but ultimately the freshwater is what matters. There are two mitigating factors in Japan that we suspect many investors do not give sufficient consideration. First, what ultimately matters is not the nominal or even real value of a country’s output. What matters is the value of output relative the number of people. This is to say that Japan has a shrinking population. Its population appears to be shrinking faster than its economy. This means that GDP per capita is doing considerably better than the abstract, un-moored aggregate GDP measure. Second, one measure of a governments fiscal soundness comes from its consolidated balance sheet. Government liabilities to other parts of itself are netted out. What this means is that Japan’s consolidated balance sheet shows its net debt position has improved, despite running persistently large budget deficits. The bonds that the BOJ holds offsets an increasing amount gross debt. Now most discussions focus on the flow (of BOJ’s JGB purchases), but in the future is may turn to the stock of BOJ holdings. At some point those bonds could be swapped for new perpetual non-marketable, perhaps even zero coupon, bonds. It may all about the sequence. . |

Click to enlarge. |

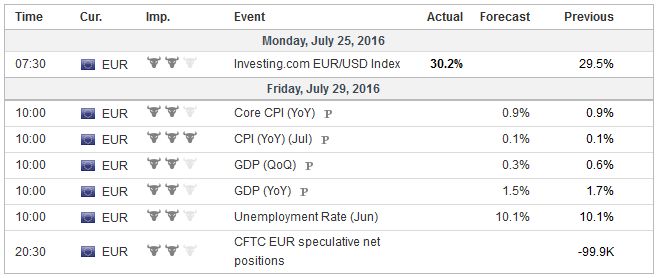

EurozoneLastly, we note that European Banking Authority stress tests results will be released at the end of the week. The recent focus has been on Italian banks for good reason. However, the risk is that other member banks, including some from core countries, will need to raise capital as well. MSCI European Bank Index lost nearly a quarter of its value in the aftermath of the UK referendum, but by the end of last week recovered half of the fall. Meanwhile the correlation between the MSCI European Bank Index and the euro has grown. What is important here is not whether the change in the euro and the change in the bank index are correlated but if the direction. Running the correlation on the value or the euro and the value of the bank index finds a positive relationship of 0.51. The 60-day correlation has been negative since last June, 2015, but put turned positive with the UK referendum. This is the fifth period of the 60-day correlation has been positive since the end of 2013 and the correlation is the second strongest of since 2014. The correlation using weekly data (rolling 26 weeks) has also turned positive. It has gradually trended higher since the extreme was reached in late-April (-0.78). The weekly correlation was positive this year from mid-January through mid-February. The takeaway from this is that in the current context, investors may want to give the performance of European bank shares greater weight among the variables in understanding the movement of the euro. |

Click to enlarge. |

Tags: #USD,Abenomics,Bank of Japan,EUR/USD,FOMC,Haruhiko Kuroda,Helicopter Money,Janet Yellen,newslettersent,U.S. Existing Home Sales