Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Weekly Market Pulse: The Turkey Leg

Weekly Market Pulse: The Turkey Leg23 Jun 2025

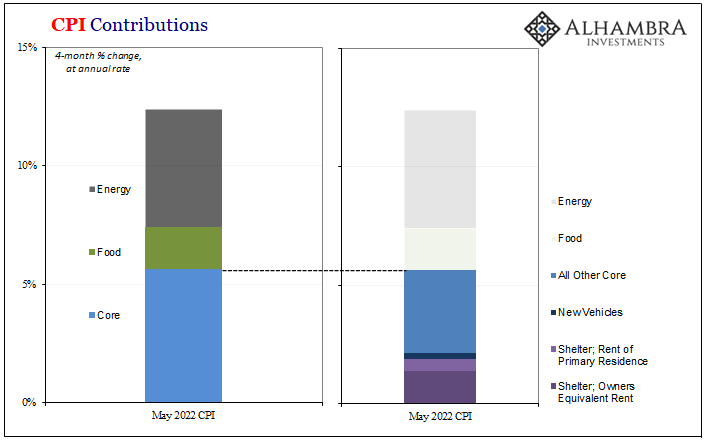

Curve Inversion 101: US CPI Politics Up Front, China PPI Down(ing) The Back16 Jun 2022

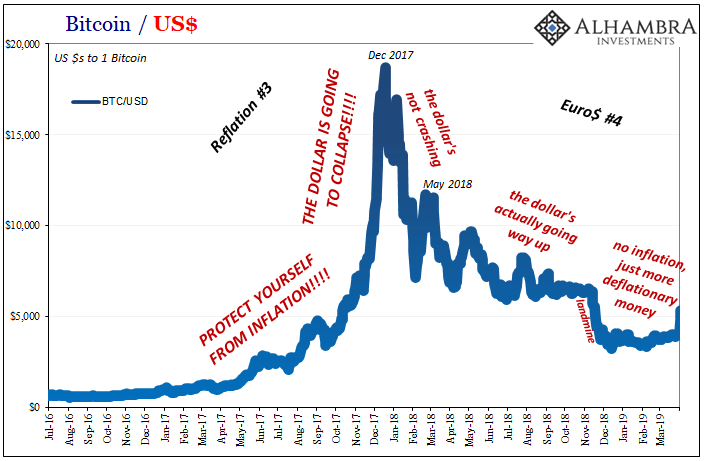

It’s Not Nothing, It’s Everything (including crypto)15 Jun 2022

The Hawks Circle Here, The Doves Win There26 Jan 2022

The Curve Is Missing Something Big21 Oct 2021

From QE to Eternity: The Backdoor Yield Caps4 Jun 2020

The Fallen Kings & The Bond Throne of Collateral24 Apr 2020

It’s Not About Jobless Claims Today, It’s About What Will Hamper Job Growth In A Few Months29 Mar 2020

The Greenspan Moon Cult5 Mar 2020

Still Stuck In Between9 Nov 2019

As Chinese Factory Deflation Sets In, A ‘Dovish’ Powell Leans on ‘Uncertainty’14 Jul 2019

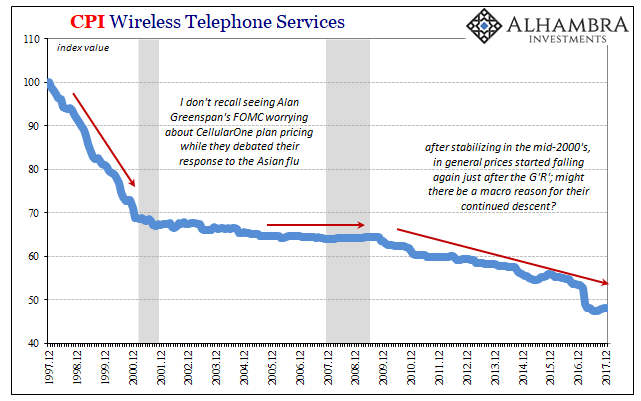

When Verizons Multiply, Macro In Inflation16 Jun 2019

Bond Curves Right All Along, But It Won’t Matter (Yet)3 Feb 2019

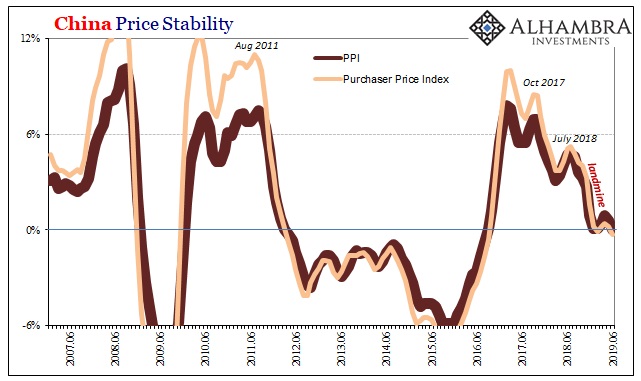

Unexpected?7 Dec 2018

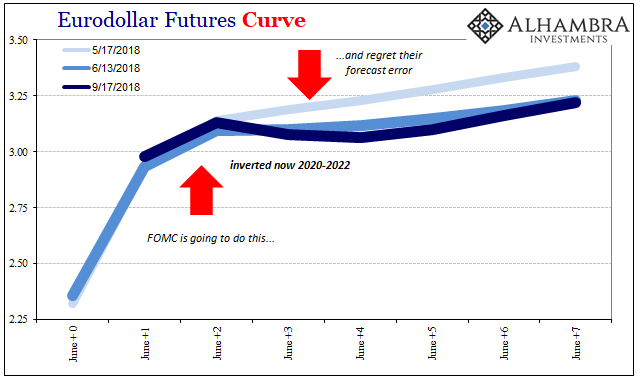

Eurodollar Futures: Powell May Figure It Out Sooner, He Won’t Have Any Other Choice20 Nov 2018

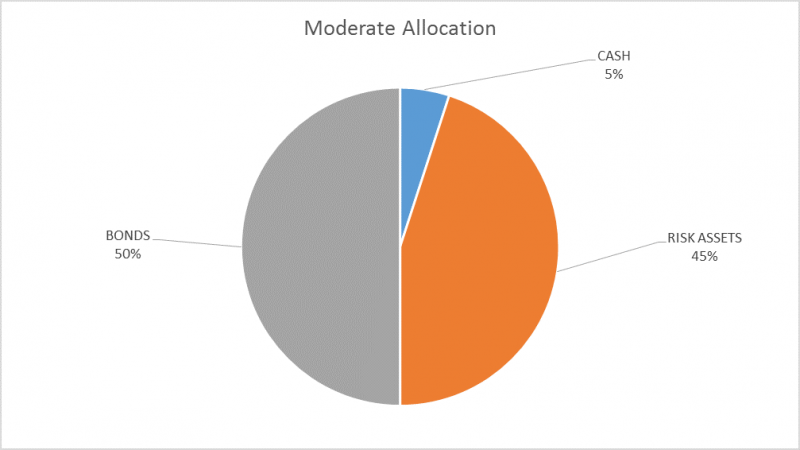

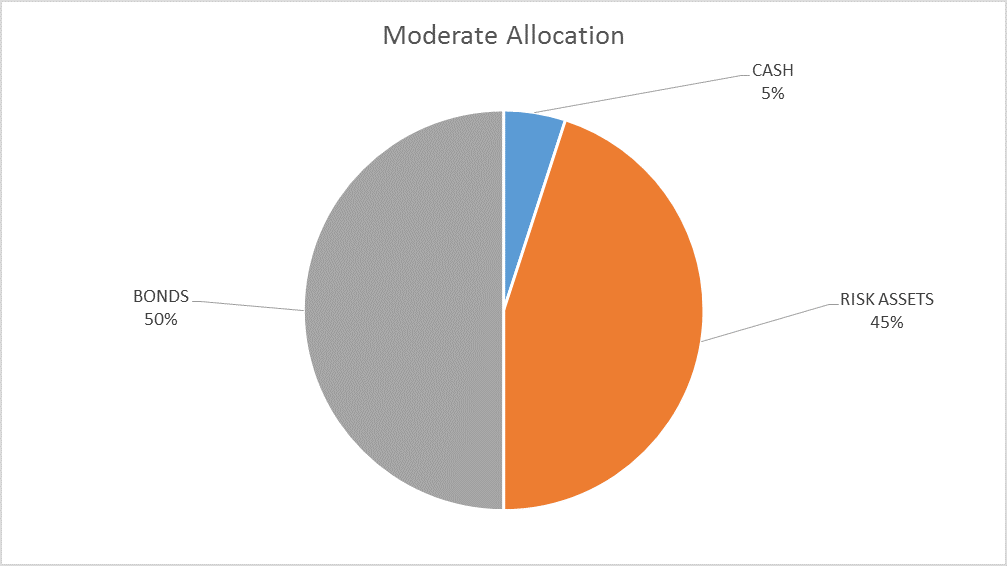

Global Asset Allocation Update:

Global Asset Allocation Update:9 Feb 2018

Good or Bad, But Surely Not Transitory19 Jan 2018

Jim Grant: “Markets Trust Too Much In The Presence Of Central Banks”15 Dec 2017

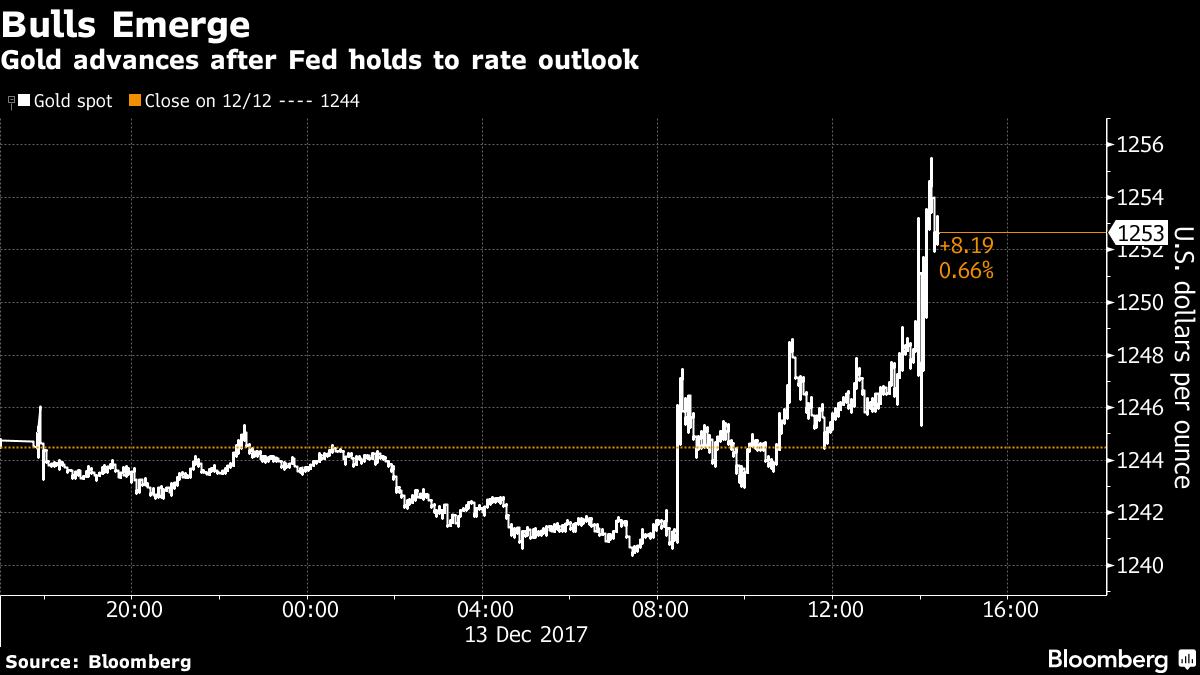

Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price15 Dec 2017

Political Economics28 Oct 2017