Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

George Dorgan

My articles My siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

CFA SocietyEconomicBlogs

Summary

Impact of Brexit will take some time to be seen, but the U.K. is already losing influence.

U.S. employment data is not sufficient to get the Fed to hike this month.

Pressure continues to build on the BOJ to act.

There have been two developments that are shaping investment climate. The first was the dramatic rally in equity markets last week, with many recovering nearly all that was lost on the Brexit wobble. The second was clear indications that the UK will not begin the formal divorce proceedings in the coming months.

There have been two developments that are shaping investment climate. The first was the dramatic rally in equity markets last week, with many recovering nearly all that was lost on the Brexit wobble. The second was clear indications that the UK will not begin the formal divorce proceedings in the coming months.

That had seemed likely when Cameron said he would leave it to his successor. However, the leading Tory candidates are suggesting that Article 50 will not be invoked this year.

Many investors appear to be concluding that thestatus quo anteprevails, that nothing really changes. Sterling is marked down, but given its current account deficit and the absence of price pressures, it might be a salutary development. We caution against such a benign view of developments.

Even if Article 50 is not invoked, the UK is already losing influence. The UK continues to be a member of the EU but is losing its voice. It EU Commissioner has resigned. Meetings and planning will be conducted with UK representatives. The UK cannot claim the rotating EU Presidency in second half of next year. Yet, the UK will still be a member of the EU and pay into the EU (though not nearly as much as the gross figures used by the Brexit camp). There will be subtle changes, like the use of English in the EU communications, and dramatic changes, like the headquarters of the European Banking Authority.

The point is that power is not subject to the legal formalities of EU rules and British law. Just because the UK has not filed divorce papers, it does not mean that the jilted significant others will just stand by waiting to be served. It will be a protracted process, but separation has begun.

The economic fallout has yet to be seen. It is true. This will take some time as the data is not available in real time. This week’s data, the June service (and construction) PMI and May industrial production will be helpful in setting the base case ahead of this (potential) shock. The important takeaway is that the UK economy appears to have lost some momentum in Q2, but in terms of pace of growth, peaked in 2015, well before the referendum became an issue. The debate among most economist seems to be whether the growth was 0.3% or 0.4% in Q2. Many are now looking for a small contraction in Q3.

The Bank of England is providing billions of sterling liquidity for the banking system. BOE Governor Carney confirmed market suspicions that the central bank would likely ease policy in the next couple of months. It may begin next week by waiving an increase in regulatory capital (counter-cyclical capital buffer).

ECB

The ECB meets later this month. The record from its June meeting will be published next week. The discussion of the UK referendum may be of interest, otherwise, the uninspiring meeting will generate a unremarkable record. The ECB is in an implementation and monitoring mode. It may be prepared to react if necessary, but it is not nearly ready for new initiatives.

Market concern about a shortage of securities given the ECB’s purchases has become more acute since the UK referendum. German bonds with maturities out seven years yield less than minus40 bp. Would anyone be surprised if the 10-year Bund, now yieldingminus12.5 bp heads toward the deposit rate?

Spurred by a report last week citing “unnamed sources” there was speculation that the ECB was considering shifting its bond buying from the capital key (share capital provided to ECB, essentially GDP) to size of debt market. We are suspicious of the story, and suspect “false flag” tactics, not by investors seeking an edge, but partisan in a political fight, maybe meant to embarrass the ECB and cajole into denying. A denial could weigh on peripheral bonds, especially Italy bonds, which would be a beneficiary of such a change.

The ECB has a number of options that would likely prove less contentious than using the size of the sovereign debt market to direct the ECB’s purchases. The ECB could lift some of its self-imposed restrictions. For example, it could waive the prohibition against buying bonds with yields less the deposit rate, or cap such purchases as a certain percentage of overall purchases.

The ECB could increase the assets being purchased, such as bank bonds, which it has been seemingly reluctant to include. Officials gave priority to agency and corporate bonds, but circumstances may force their hand, especially if the program is extended, beyond the current soft end point of March 2017.

EurozoneEurozone economic data is expected to be consistent with the somewhat slower pace of growth after unusually strong 0.6% advance in Q1. Consider that over the past five years (20 quarters) growth has averaged less than 0.15% a quarter. German industrial output is expected to have stagnated in May, while French output probably fell. Retail sales may rise for the first time in three month; consumption also appears to have softened in Q2. It is too early to consider new ECB measures even if the staff forecasts later this month confirm that Draghi’s suggestion that Brexit could shave 0.5 percentage points off eurozone growth over three years. The German 10-year breakeven is around 80 bp. It has not been above 100 bp since late-May. We expect the ECB to announce that its QE operations will continue past March 2017, but it is too early to expect the formal decision. |

Click to enlarge. |

Although there is much focus on Italian banks, the IMF cited the largest German bank as biggest risk. The US branch failed the Federal Reserve’s stress test for the second consecutive year. Shares prices are below the low point in the post-Lehman period of great duress. This unfolding drama will continue to command investors’ attention. Separately, Italy secured EU approval to provide banks with a 150 bln euro liquidity guarantee and reportedly is working on plans to have boost the Atlas Fund’s resources, with the assistance of Italy’s development bank (CDP). Italian bank shares responded favorably to these developments.

JapanPressure continues to mount on the Bank of Japan. Last week’s data showed price pressures are moving in the wrong direction, and despite a tight labor market, consumption is contracting. Any disruption emanating from Brexit does Japan no favors. Japan reports May’s balance of payments.There are strong seasonal patterns. April consistently deteriorates from March, and May tends to improve upon April. However, this time, the median guesstimate from the Bloomberg survey is for a small worsening. The bulk of the deterioration can be traced to the trade balance. However, due to size of the sums involved, the yen’s strength has larger impact on capital flows than trade flows. Japanese primary income surplus overwhelms the trade balance by orders of magnitudes. Separately, the Japan’s MOF report weekly portfolio flow data. In the week ending June 24, the day after the UK referendum, MOF data shows foreigners sold a near-record JPY2.16 trillion Japanese bonds. It was the second consecutive week of sales. It could be related to the end of the quarter, but it may also be related to a change in view on the yen (less bullish). It may take a couple more weeks to sort out what is happening. Japanese bond yields continued to decline last week. The yield curve is negative for durations up through 15-years. Reportedly, Japanese banks have stepped up their protestations to officials. |

Click to enlarge. |

The Reserve Bank of Australia and Sweden’s Riksbank hold policy meetings. Neither is expected to change policy. There is no great urgency to act. Both will keep their options open. Indicative pricing in derivatives market suggests investors are more inclined to see an RBA rate cut than the Riksbank move in the coming months. The outcome of the Australian election is too close to call and the determination process will continue on July 5. A broader coalition government, which may mean more fragile, is the most likely outcome.

The FOMC minutes from the June meeting may be of some passing interest, but events have superseded it. While Yellen said at her press conference that a July hike was “not impossible,” the bar is high, and it will take more than a healthy jobs report to change this assessment. Vice Chairman Fischer underscored this point at the end of last week.

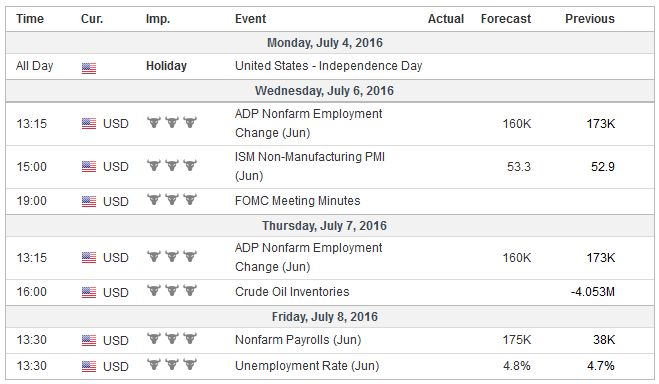

United StatesThe US also reports trade, durable goods orders, and the non-manufacturing PMI. These reports will help economists fine-tune forecasts for Q2 GDP, which by most reckoning is nearly double the Q1 pace. The most important report, of course, is the jobs data. |

Click to enlarge. |

We regard last month’s 38k print as a statistical fluke; that seems to take place once a year or so, within a gradual moderation of the pace of job growth. The median forecast is for a 175k-185k rise in June nonfarm payrolls. The six-month average is 170k. The 12-month average is 200k. The unemployment rate may tick up to 4.8% from 4.7%. The workweek is expected to be flat, while a 0.2% rise in average hourly earnings would be sufficient for the year-over-year pace to 2.7%, which would represent a new cyclical high.

Brexit has thrown a new element of uncertainty in the markets and the world economy. When in doubt, the Fed stands pat. It is not inconsistent to say the Fed is data dependent. Officials need to see how it performs in Q3, through the pattern of a weak Q1 followed by a strong Q2, and through the global shocks. The market says there is no chance of a rate hike in September, at the next FOMC meeting after this month’s. We suspect the chances are somewhat greater, even if less than even money.

Full story here Are you the author?

Tags: Article 50,Janet Yellen,Mario Draghi,newslettersent,Post-Brexit,U.S. Average Earnings,U.S. Nonfarm Payrolls