Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

| The assassination of Jo Cox, a member of the UK parliament is a personal and political tragedy. Her needless death provided an inflection point. The suspension of the referendum campaigns and a steady stream of reports and speeches has the emotionalism of contest freeze. Investors quickly understood that the Cox’s death injected a new unknown into the forces that seemed to build toward a decision to leave the EU. |  |

The assassination of US President Kennedy in 1963 turned the conservative Democrat into a martyr, which was a critical inspiration for the 1964 Civil Rights Act. Similarly, it is too early to say with any degree of confidence that Cox’s assassination has the potential and investors responding by reducing some of their risk off trades ahead of the weekend.

Perhaps the most striking move has been sterling. It neared $1.40, a key psychological level we have noted and rebounded to $1.4250 as investors grappled with the impact of the Cox’s death. Asia picked up with North American markets let off to take sterling a little through $1.4300. The intraday technicals suggest it may be difficult for the North American session to significantly extend sterling’s gains further.

After sterling, the Australian and Canadian dollars are leading the major currencies higher. The less risk averse tone and firmer commodity prices are helping. Oil is snapping a six-day slide. Other industrial metals, including copper, is firmer. The roughly 0.5% gain in gold is consistent with the broader commodity move even if not with general risk-on.

FX RatesThe dollar extended its recovery against the yen after reaching JPY103.50 yesterday in Asia. It finished the North American session near JPY104.25 and edged to almost JPY104.85 in Asia earlier today. Despite the firmer tone in equity markets and higher core bond yields, the dollar has not sustained its earlier momentum. It is consolidating above JPY104.00. The sharp move in the yen in recent days has seen Japanese officials renew their expressions of concern. |

click to enlarge |

Japanese YenThe yen has gained 2.6% against the dollar this week and the same against the euro, which is flat against the dollar. Given the dovish tilt of the Fed, the stand pat BOJ, and slide in equities, the yen’s gains do not seem unusual or a sign of a disorderly market. |

click to enlarge |

The quiet economic news stream and somber mood have seen equity markets recoup part of yesterday’s losses. MSCI Asia Pacific was up 0.6% after falling 1.1% on Thursday. It is nearly 3% this week. The MSCI Emerging Market equity index is up 0.7% ahead of Latam’s open but is still off 2.2% on the week. European shares are seeing a stronger response. The Dow Jones Stoxx 600 is up a little more than 1.6% near midday in London. Financials and energy sectors are leading the way, but the breadth is good with all sectors higher. The index is off less than 2% for the week.

S&P 500The US S&P 500 staged an impressive recovery yesterday. It initially gapped lower to extend its losing streak into a sixth consecutive session. It fell to 2050, the lowest level since May 23, before rallying to news session highs near 2080. The gap may have been an exhaustion gap, follow through buying is needed to confirm, and ahead of the weekend, a cautious tone will likely prevail. |

click to enlarge |

US TreasuriesUS 10-year Treasuries also staged an impressive reversal yesterday. Yields fell to nearly 1.50% before rebounding to nearly 1.58%. Unlike the S&P 500, there is follow through in the notes, and yields stand at 1.61%. At the end of last week, it closed at 1.64%. The low US yields are partly a reflection of the anticipated trajectory of short-term rates, which is driven by Fed policy. The low US yields also partly reflect the demand, which has been elevated by the negative yields that prevail in much of Europe and Japan. |

click to enlarge |

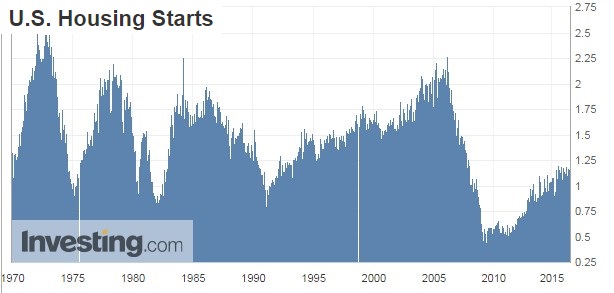

North AmericaIn the North American session, the US reports housing starts and permits, while Canada reports May CPI. Housing starts are expected to slow by around 2% after a strong 6.6% rise in April. Permits, which are a forward-looking indicator, are expected to edge higher after a 3.6% increase in April. A 0.5% rise in Canada’s headline CPI will be consistent with a slowing of the year-over-year pace to 1.6% from 1.7%. The core rate is expected to rise 0.3%, but slow to 2.1% year-over-year. Market impact is likely to be minimal. Lastly, after rising for the past two weeks, the rig count may draw new attention. The July light sweet crude contract was recovering from the dip below $46 yesterday. The target we suggested at the start of the week was $45.40. A move above $.47.80 may signal the downdraft is over. |

|

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: Brexit,FX Daily,Japanese yen,Jo Cox,newslettersent,U.S. Housing Starts,U.S. Treasuries