Yesterday when summarizing the Fed's action we said that in its latest dovish announcement which has sent the USD to a five month low, the Fed clearly sided with China which desperately wants a weaker dollar to which it is pegged (reflected promptly in the Yuan's stronger fixing overnight) at the expense of Europe and Japan, both of which want the USD much stronger.

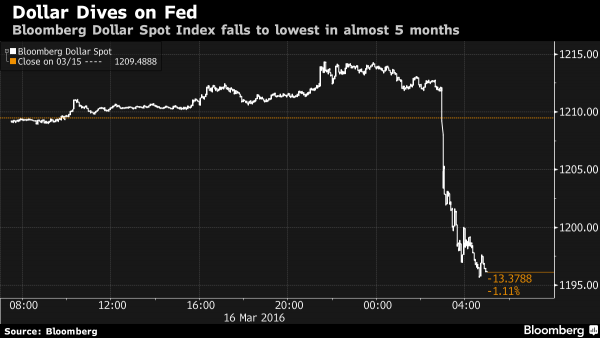

This morning the global markets got a rude reminder that at the end of the day it is all about currency devaluation and competitive debasement - even if it means appeasing China in the process - when the plunge in the dollar,, much to

Goldman's ongoing embarrassment, extended overnight as seen in the chart below.

This has led the USDJPY slide to just over 111 while the EURUSD was surging over 1.13 as of this moment,

and in the process undoing all the recent easing by both the ECB and the ECB; furthermore an expected 25 bps rate cut by the Norway Central Bank, not only did not weaken the NOK but in fact sent it surging against the EUR, indicating that even when central bank decisions are fully priced in, few can actually trade the reaction and the implication of such moves.

Worse, after briefly spiking in the aftermath of the Fed's decision overnight European sovereign and US Treasury yields have tumbled, commodities and especially gold have soared, and as of moments ago, European stocks hit their lows on the day now that the European currency is surging, leading to this:

- EUROPEAN STOCKS EXTEND DROP; STOXX 600 DOWN 1.4%

And since these are all the telltale signs of yet another Fed policy error, it was only a matter of time before the move also hit the Fed's favorite asset class - equities, and sure enough, after posting modest gains overnight, US index futures have seen a sharp reversal lower, and from up 0.3% were down -0.3% at last check, as suddenly the market appears to be getting cold feet not only about the Fed's decision to slam the Dollar at the expense of the Euro and the Yen, but also going back to that all important question which Yellen was unable to answer:

has the Fed lost its credibility?

While risk assets are suddenly

airpocketing, dollar-denominated oil, copper and zinc all jumped by more than 2 percent, with Brent trading above $40 a barrel, which means we can expect a rewriting of the narrative that higher gas prices are actually good for consumers, even if it also means that marginal shale production is likely to start coming back on line any moment.

And the cherry on top may have come when moments ago industrial bellwether Caterpillar slashed guidance, and now expects non-GAAP Q1 EPS of $0.65-$0.70 per share, about 25% below consensus estimates of 95 cents.

All of the above, this had led to sudden repricing of risk, which has seen equity futures stumble, and the ES is now down 10 points to 2,007, roughly where it was when the Fed unveiled its dovish surprise. Was that it for the Fed's intervention halflife? We don't know, but we expect much confusion today over whether even the Fed has now run out of dovish ammunition.

This is where we stand currently

- S&P 500 futures down 0.5% to 2006

- Stoxx 600 down 1.4% to 336

- FTSE 100 down 0.7% to 613

- DAX down 1.7% to 9816

- German 10Yr yield down 7bps to 0.24%

- MSCI Asia Pacific up 2.1% to 129

- US 10-yr yield down 5bps to 1.86%

- Dollar Index down 0.82% to 95.1

- WTI Crude futures up 1.6% to $39.08

- Brent Futures up 1.4% to $40.09

- Gold spot up 0.6% to $1,270

- Silver spot up 0.2% to $15.65

Top Global News

- Witty to Step Down After Tumultuous Tenure as Glaxo Chief: CEO Andrew Witty plans to step down in 2017 after almost a decade, board to begin search for a successor

- Rio Tinto Appoints Copper Chief Jacques CEO to Succeed Walsh: Copper boss Jacques replaces iron man Sam Walsh in July

- FedEx Raises Floor of Full-Year Forecast After Cutting Costs: Now sees FY16 adj. EPS $10.70-$10.90, saw $10.40- $10.90, est. $10.56; 3Q adj. EPS $2.51, est. $2.34

- Pershing Square Falls 26% Year Through March 15 on Valeant: Cut its stake in Mondelez to 5.6%

- Toshiba Said to Face U.S. Probe Over Westinghouse Accounting: Justice Department, SEC reviewing conduct in Toshiba report

- VW Said in Talks With U.S. Over Two Funds to Pay for Pollution: In talks to establish national remediation fund and a separate one for California as punishment for pollution from its cars after co. cheated on diesel- emissions tests, said people familiar with the matter

- Fed Softens Rate-Rise Urgency as Risks Abroad Cloud Outlook: FOMC cites global concerns twice as Yellen highlights in Q&A

- American Pilots Concerned by CEO Meeting on ‘Toxic’ Culture: COO Robert Isom named to deal with pilot contract concerns

- Goldman Seen Succumbing Too as Wall Street Suffers Awful Quarter: Its trading revenue may slide 17%, Credit Suisse analysts say

- New York’s Plaza Hotel Said for Sale in Foreclosure Auction: Billionaire Reuben brothers said to foreclose on mortgage

- Oil Investors See $7.4b Vanish as Dividends Are Targeted: Conoco, Kinder resort to cuts “deplored” by shareholders

- March Madness Puts Time Warner’s Big Bet on Sports to the Test: NCAA men’s championship game to air on TBS for first time

- Valeant Lenders Said to Mull New Terms in Default Talks, Reuters Says: Lender’s demands include higher interest payments, pledge to pay a larger amount of bank loans from any Valeant asset sales proceeds

- Amazon Said to Eye Office Depot’s Corporate Business Unit, NYP Report: May use some of Office Depot’s corporate accounts to jump-start its new office supply business

- Canada to Announce Bombardier Aid Decision Within Weeks, Reuters Says: Govt has finished studying co.’s request for $1b in aid

Looking at global equity markets, Asia stocks traded mostly higher in the wake of the FOMC. ASX 200 (+1.0%) was led by energy and basic materials after commodity prices benefited from USD weakness post-FOMC, while oil prices were also underpinned following yesterday's lower than expected DoE inventory build. Nikkei 225 (-0.2%) initially surged on the prospects of lower US rates for longer, but then shrugged off majority of gains as JPY strengthened, while the Shanghai Comp (+1.2%) conformed to the picture with the PBoC also said to be gauging banks for Medium-term Lending requirements. 10yr JGBs initially tracked T-notes higher following the Fed dovishness, however JGBs pared advances after a weaker 20yr bond auction result in which b/c, tail in price and lowest accepted price all disappointed.

Top Asian News

- Li & Fung 2015 Earnings Top Estimates as New Clients Boost Sales: FY net $421m, est. $405.3m, sales down 2.4% to $18.8b

- Billionaire Li’s CK Hutchison Profit Edges Above Estimates: FY adj. net HK$31.2b; est. HK$30.9b, profit helped by earnings from Europe telecom operations

- China Mobile 2015 Profit Misses Estimates, Shares Reverse Gain: Govt request to lower mobile phone rates erodes profit

- Mr. Yen Called the Rally, Now Sees Gain Toward Intervention Zone: Ex-MOF Sakakibara correctly predicted advance

- Toshiba Gets $5.9 Billion Deal to Sell Medical Unit to Canon: Deal will be funded by existing cash and borrowings, Canon said, day after unsuccessful bidder Fujifilm questioned Toshiba about the sale

- Escape From Negative Japan Rates Wrecked by Record Hedging Costs: Swap premium for yen holders reaches record 102.5 bps

- Yuan Falls to 15-Month Low Versus Basket as Fixing Lags Dollar: Reference rate shows China doesn’t want excessive gains, DBS says

- TPG Sees Opportunity in $131 Billion India Distressed Assets: Co. would like to triple India investments in 3 yrs

In Europe, this morning has seen focus fall on the fallout from the Fed rate decision and press conference yesterday and as such, has seen much of the price action continue on from US and Asian hours. Bunds have seen significant upside during European trade, with the June future residing above 162.00 and the German curve showing many of the characteristics as its US counterparts with the curve flattening amid expectations for a shallower rate path going forward.

In tandem with this, European equities saw initial upside at the open in the wake of the dovishly interpreted Fed announcement. However stocks came off their best levels by mid-morning to see Euro Stoxx reside relatively flat as some analysts begin to focus on recent central bank commentary which appears to be relatively downbeat for global growth prospects as highlighted by the Fed statement and UK budget yesterday and the SNB and Norges Bank today.

Top European News

- Lufthansa Says Eurowings Price Cuts to Curb Profit Gains in 2016: Oper. profit will advance only “slightly” in 2016 amid deterioration in yields as Eurowings adds flights in long-haul market, where Lufthansa traditionally makes most of its money, and competition from low-cost rivals intensifies in Europe

- LafargeHolcim Sees Demand Growing After 2015 Profit Falls: Says overall demand to rise 2% to 4% in 2016, co. says it has made progress towards asset sales target; 2015 adj. operating Ebitda fell 10.7% to CHF5.75b vs est. CHF5.73b

- Swiss Keep Franc Intervention Threat Alive as Rates Left on Hold: SNB holds deposit rate at minus 0.75% as forecast by economist, repeats pledge to intervene in FX markets

- Norway Cuts Rates and Signals More Easing Ahead Amid Oil Plunge: Overnight deposit rate was lowered by 25bps to 0.50%

- HeidelbergCement Boosts Dividend Amid Expected 2016 Growth: Raises div. 73% to EU1.30/share, sees “moderate” improvement in 2016 profit

- Gulf Keystone Tumbles to Seven-Year Low as Future in Doubt: Kurdistan-focused oil company faces “material uncertainties”

- Bank of England Has Nowhere to Go With ‘Brexit’ in Limelight: Key rate will be kept at record low 0.5%, economists predict

In FX, early European flow has seen a continuation of the USD fallout from the Fed adjustment in rate hike projections for 2016. Commodities and their related currencies have benefited the most , notably USD/CAD, which is has torn through a series of support levels including 1.3000 to hit 1.2941. WTI is now looking to a move through $40.0, and the CAD seems to have pre-empted this to a degree, but near term stagnation in the Oil price sees some consolidation back around 1.3000 for now. AUD/USD took out .7600 in Asia, having previously contained the upside, but since then we have gone on to hit .7650. EUR/USD has had an easy ride on the upside and has traded to just shy of 1.1300, while EUR/GBP gains stalling at .7900 to allow for a Cable extension through 1.4300 , but lacking momentum here. USD/JPY is the one we are all watching from current levels, having taken out 112.00 to put 111.00 (double bottom) under threat. 111.45 is the low here so far, but now major pullback to note in the current climate.

The Bloomberg Dollar Spot Index, which tracks the U.S. currency against 10 major peers, sank 0.9 percent at 10:18 a.m. in London, after losing 1.1 percent in the last session.

“Currency reaction suggests market expectations for the Fed’s rate outlook were slightly more bullish,” Hiroshi Kurihara, chief U.S. economist at Bank of Tokyo-Mitsubishi UFJ Ltd. in New York. “The dollar’s been sluggish despite some positive signs over growth, hinting that it’s sensitive to negative news and that its advance may not be strong even as a rate hike approaches.”

The yen strengthened 0.8 percent versus the dollar, while the British pound rose 0.3 percent and Switzerland’s franc gained 0.4 percent. The Bank of England is forecast to leave interest rates unchanged on Thursday and maintain current stimulus levels, while the Swiss National Bank stuck with its ultra-loose monetary policy. The Norwegian krone appreciated 1.1 percent after a cut in borrowing costs.

In commodities, WTI and Brent continue to rally after yesterday's FOMC comments with WTI close to testing the USD 40/bbl level. Gold also benefited from the FOMC reaching highs of USD 1267.60/oz while platinum and palladium are also appreciating respectively . In base metals Zinc advanced for the first time this week amid global production fell for a second month, while copper and iron ore prices were bolstered with the latter gaining over 4% amid the heightened risk sentiment. However, analysts at Jinrui futures did highlight that the market is waiting to see signs of Chinese demand given the increase in inventories and slowing physical trade.

Bulletin Headline Summary from RanSquawk and Bloomberg

- European equities fail to sustain opening gains as weakness in financials and the downbeat outlook for global growth prospects grips investor sentiment

- Early European FX flow has seen a continuation of the USD fallout from the Fed adjustment in rate hike projections for 2016

- Looking ahead, highlights include the BoE rate decision, US weekly jobs, Philadelphia Fed Business Outlook, JOLTS, and EIA Nat. Gas Storage Change

Treasuries rally overnight, global equity markets mostly lower and commodities rally after more a dovish FOMC statement and SEP than foreseen; today’s economic data includes jobless claims, JOLTS Job Openings.

Bank of England will announce their latest decision today together with minutes of their discussions. Investors are pricing in 20% chance they will cut benchmark interest rate this year

The Bank of Japan’s negative interest rate policy is making it more expensive for domestic banks to hedge dollar investments, threatening to slow their escape from negative rates into U.S. currency debt

Even with a 25% drop in the yen’s value, Japanese export volumes are basically unchanged from where they were when Prime Minister Shinzo Abe took office

Norway’s central bank cut its benchmark interest rate 25 basis points to a record low 0.50% and signaled it’s prepared to ease policy further to ward off a recession in western Europe’s biggest crude oil producer

Switzerland’s central bank held interest rates at a record low and repeated its pledge to intervene in currency markets, a threat President Thomas Jordan has used to keep the franc from strengthening

As Wall Street leaders warn publicly about this quarter’s plunging revenue from trading and deals, Goldman Sachs has provided no guidance. The mystery isn’t whether it is getting hit too -- it’s how hard

$2.5b IG corporates priced yesterday; WTD $19.61b, MTD $106.03b, YTD $400.28b; $665m HY priced yesterday, MTD 13 deals for $7.315b, YTD 38 deals for $22.165b

Sovereign 10Y bond yields lower; European, Asian equity markets mostly lower; U.S. equity- index futures steady. WTI crude oil, copper, gold rise

US Event Calendar

- 8:30am: Current Account Balance, 4Q, est. -$118b (prior -$124.1b)

- 8:30am: Philadelphia Fed Business Outlook, March, est. -1.5 (prior -2.8)

- 8:30am: Initial Jobless Claims, March 12, est. 268k (prior 259k); Continuing Claims, March 5, est. 2.235m (est. 2.225m)

- 9:45am: Bloomberg Economic Expectations, March (prior 42.5); Bloomberg Consumer Comfort, March 13 (prior 43.8)

- 10:00am: JOLTS Job Openings, Jan., est. 5.5m (prior 5.607m)

- 10:00am: Leading Index, Feb., est. 0.2% (prior -0.2%)

Central Banks

- 8:00am: Bank of England bank rate, est. 0.5% (prior 0.5%)

DB's Jim Reid concludes the overnight wrap

Although we saw the Fed closer align its rates expectations with those of the market, the market pushed Fed Funds expectations back even further with the probability of a June hike taken down to 38% (from 54%). Yellen made mention in her press conference of the April meeting being ‘live’ – which is unlikely to be surprising given her preference for optionality – although the market clearly sees that as an even longer shot now with the probability down to 8% this morning, after being at 25% just 24 hours ago.

Away from the Fed, it’s worth adding that Oil (+5.83%) rebounded hard yesterday (and is up further this morning) and in turn wiped out the heavy losses from Monday and Tuesday. That more than played its part in the price action for risk assets with the surge coming on reports that Saudi Arabia and other oil exporters will limit output levels even if Iran refuses to cooperate. According to the WSJ, Qatar have been reported as saying that they will host a meeting on April 17th for both OPEC and non-OPEC members to discuss such measures, although we highlight that this date has appeared to be pushed back on a number of occasions now.

Looking at the latest in Asia, aside from a drop in the Nikkei (-0.73%) with the stronger Yen weighing on markets there, bourses elsewhere are trading with broad based gains with the Hang Seng (+1.02%), Shanghai Comp (+0.88%), Kospi (+0.70%) and ASX (+0.96%) all up strongly. Credit indices are performing strongly too with the iTraxx Aus and Asia indices 5bps and 4bps tighter respectively. Asia FX is also posting some solid gains, while the Aussie Dollar is up over half a percent following an unexpected fall in the unemployment rate data this morning.

Back to yesterday and a quick recap of the economic data. As noted earlier, core inflation for the US in February was up a slightly better than expected +0.3% mom last month (vs. +0.2% expected) which has helped to nudge the YoY rate up one-tenth to +2.3% and the highest now in five years. Headline inflation was as expected at -0.2% mom last month, with the YoY rate down four-tenths to +1.0%. Elsewhere we saw industrial production disappoint with a -0.5% mom decline in February and more than expected (-0.3% expected) with utilities and mining output both contributing to the slump. Capacity utilization was down four-tenths to 76.7% (vs. 76.9% expected) although there was some better news in the latest manufacturing production data which showed a better than expected +0.2% mom gain last month (vs. +0.1% expected). Elsewhere, last month’s housing starts data showed a robust +5.2% mom increase (vs. +4.6% expected) although permits slipped -3.1% mom (vs. -0.2% expected).

In Europe yesterday price action was pretty benign which was of little surprise ahead of the Fed. The Stoxx 600 (+0.04%) closed barely unchanged while credit indices were flat to slightly wider (iTraxx sub fins being the notable underperformer, closing 10bps wider). Notable during the European session however was the €24bn of primary bonds issuance which priced in Europe which was the biggest volume day in two years and the week-to-date volume so far the second busiest YTD.

Looking at the day ahead now, this morning in Europe the notable data to be released will be the final revision to the February CPI report for the Euro area (no change to -0.2% yoy headline expected) along with the January trade balance. While the dataflow is light, there’s no shortage of central bank meetings however with the BoE, SNB and Norges Bank all due to announce their latest policy decisions – the latter the only one where the market is expecting a change with a 25bps cut to the deposit rate expected (to 0.5%). This afternoon in the US it’s another reasonably busy afternoon of data. The Philly Fed business outlook for March will be closely watched, while we’ll also receive employment data in the form of initial jobless claims and JOLTS job openings for January. The Conference Board’s February leading indicator will also be released.

Full story here

Are you the author?

ZeroHedges' Tyler Durden is the hero of Fight Club, the 1999 movie based on Chuck Palahniuk's novel that reflected Chuck's experience in the Cacophony Society Quote: "Goddamn it, an entire generation pumping gas, waiting tables, slaves with white collars. Advertising has us chasing cars and clothes, working jobs we hate so we can buy shit we don’t need. We’re the middle children of history, man. No purpose or place. We have no Great War. No Great Depression. Our Great War’s a spiritual war… our Great Depression is our lives. We’ve all been raised on television to believe that one day we’d all be millionaires, and movie gods, and rock stars. But we won’t. And we’re slowly learning that fact. And we’re very, very pissed off." --> see more about Tyler on snbchf

Previous post

See more for 1.) Zerohedge on SNB

Next post

Tags:

Bank of England,

Bond yield,

British Pound,

Copper,

Credit Suisse,

Crude Oil,

default,

Equity Markets,

Fail,

Goldman Sachs,

Housing Starts,

India,

Initial Jobless Claims,

Iran,

Jim Reid,

Monetary Policy,

Nikkei,

Norges Bank,

Norway,

OPEC,

Price Action,

recession,

Reuters,

Saudi-Arabia,

Swiss National Bank,

Trade Balance,

U.S. Housing Starts,

U.S. Initial Jobless Claims,

Unemployment,

USD/JPY

This has led the USDJPY slide to just over 111 while the EURUSD was surging over 1.13 as of this moment, and in the process undoing all the recent easing by both the ECB and the ECB; furthermore an expected 25 bps rate cut by the Norway Central Bank, not only did not weaken the NOK but in fact sent it surging against the EUR, indicating that even when central bank decisions are fully priced in, few can actually trade the reaction and the implication of such moves.

Worse, after briefly spiking in the aftermath of the Fed's decision overnight European sovereign and US Treasury yields have tumbled, commodities and especially gold have soared, and as of moments ago, European stocks hit their lows on the day now that the European currency is surging, leading to this:

This has led the USDJPY slide to just over 111 while the EURUSD was surging over 1.13 as of this moment, and in the process undoing all the recent easing by both the ECB and the ECB; furthermore an expected 25 bps rate cut by the Norway Central Bank, not only did not weaken the NOK but in fact sent it surging against the EUR, indicating that even when central bank decisions are fully priced in, few can actually trade the reaction and the implication of such moves.

Worse, after briefly spiking in the aftermath of the Fed's decision overnight European sovereign and US Treasury yields have tumbled, commodities and especially gold have soared, and as of moments ago, European stocks hit their lows on the day now that the European currency is surging, leading to this: