Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The optics of the US jobs report was better than the details, which is the exact opposite of the January employment report. The US dollar strengthened on the news.

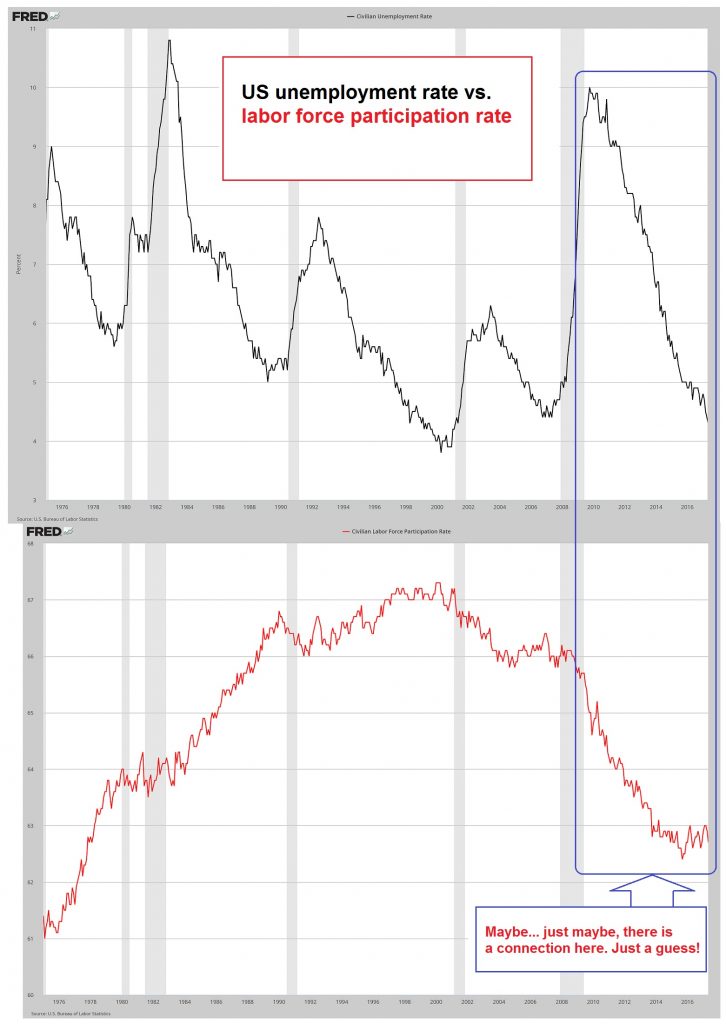

The US created 242k jobs in February. The consensus was for around 195k. The January gain of 151k was revised up to 172k The household survey showed a 530k increase. The market expected a 175k. In January the household survey showed an increase of 615k. Combined the household survey has showed over a million new jobs. This is the most in more than two years. The participation rate rose to 62.9% from 62.7% while the unemployment rate remained steady. Under-employment fell to 9.7% from 9.9% and is a new cyclical low. That is the good news.

The less favorable news is in the hours worked and earnings. The average weekly hours fell back to 34.4 from 34.6. This is a negative for output. Hourly earnings were expected to have risen by 0.2%, but instead fell by 0.1%. It is the first decline in more than a year. This dragged the year-over-year pace down to 2.2% from 2.5%. Manufacturing lost 16k jobs. The consensus expected only a 1k loss, while the January gain was trimmed to 23k from 29k.

Taken as a whole, this is not the kind of report that precedes a recession, which so many have worried about given the tightness of the financial conditions. There are no implications for the FOMC meeting later this month. Just like the Fed thinking that four hikes would be appropriate this year was exaggerated so to was the market's idea that no hikes were appropriate. The market has begun pricing in a greater chance of a hike this year, while the Fed's dot plot is likely to show the earlier optimism has faded and probably show two (possibly three) hikes is still appropriate.

The broad risk on environment continues through the US jobs data. US stocks will initially extended the recent gains. The 10-year bond yield is edging higher, but the two year interest rate differentials are not moving in the US favor today. This warns that the initial dollar gains may not be sustained today.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: U.S. Participation Rate