Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

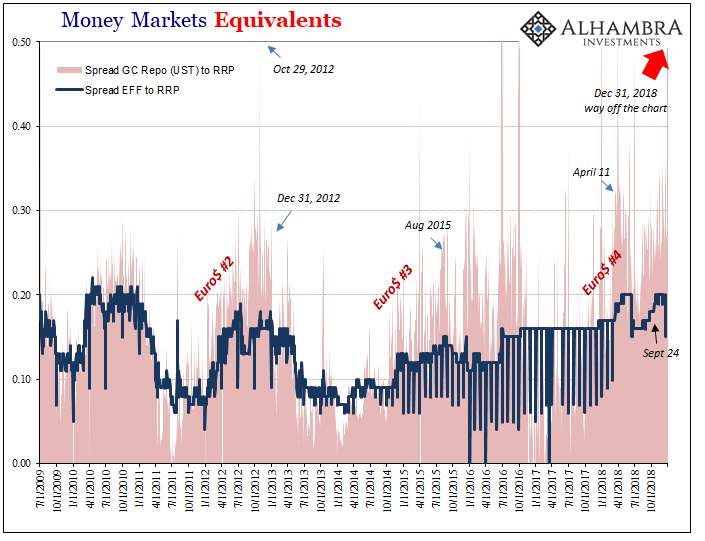

Insane Repo Reminds Us

Insane Repo Reminds Us4 Jan 2019

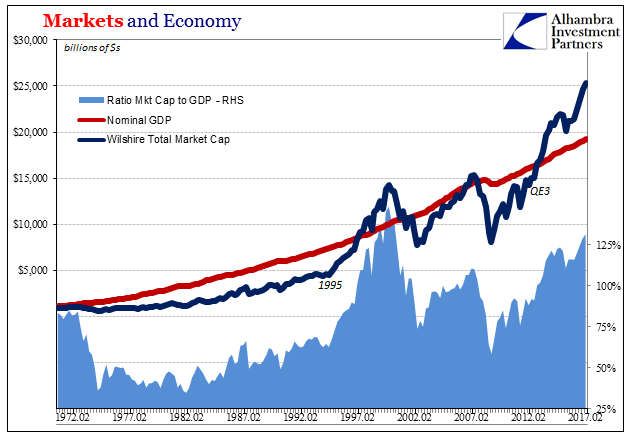

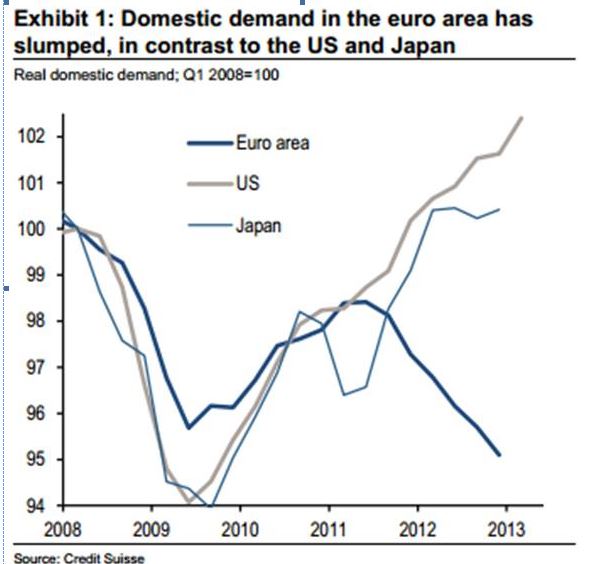

SNB Balance Sheet, Markets and Economy: As Good As It Gets?10 Aug 2017

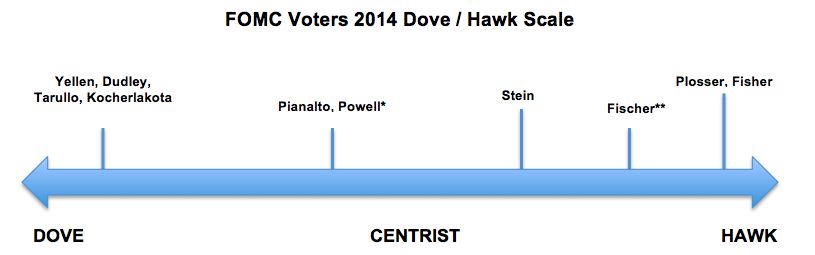

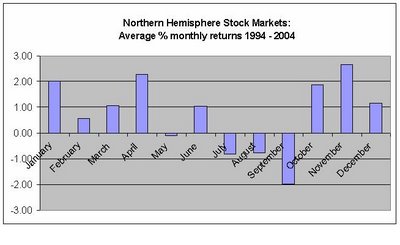

The “Sell in May, Come Back in October” Effect and the 19 Fortune-Tellers of the FOMC3 Apr 2013

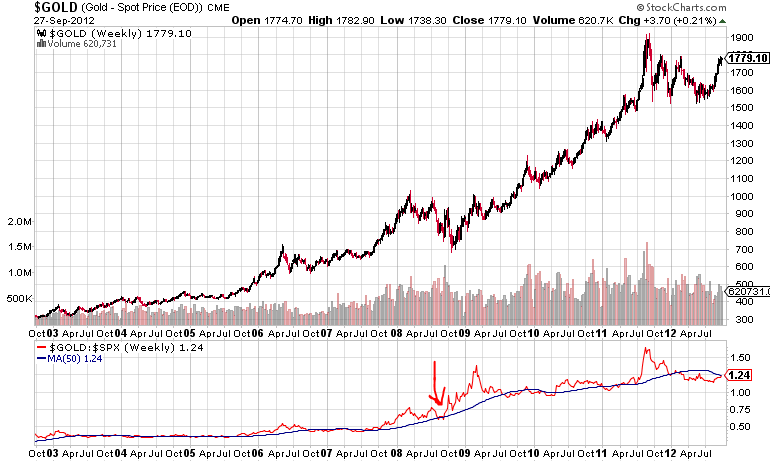

Quantitative Easing, Gold and the Swiss Franc27 Dec 2012

Quantitative Easing: The Fed Wants Americans to Continue Deficit Spending13 Dec 2012

Die Wiederwahl Obamas bedeutet nichts Gutes für die Schweiz7 Nov 2012

Marc Faber: Assets are overpriced, we short metals and Brent now11 Oct 2012

It’s not simply QE3

It’s not simply QE314 Sep 2012

Isn’t it wonderful to trade with a strong central bank behind you?13 Sep 2012

SNB prints nearly 5 billion francs in one week, FX traders poised to get ripped off10 Sep 2012

10 Sep 2012

The Big Swiss Faustian Bargain: Differences between SNB, ECB and Fed Money Printing Explained3 Sep 2012

SNB only major central bank missing at Jackson Hole, are important SNB decisions looming ?27 Aug 2012

FX Technical Outlook, Net Speculative Positions, Global Markets, week August 2727 Aug 2012

Brad DeLong on Jackson Hole and Quantitative Easing

Brad DeLong on Jackson Hole and Quantitative Easing22 Aug 2012

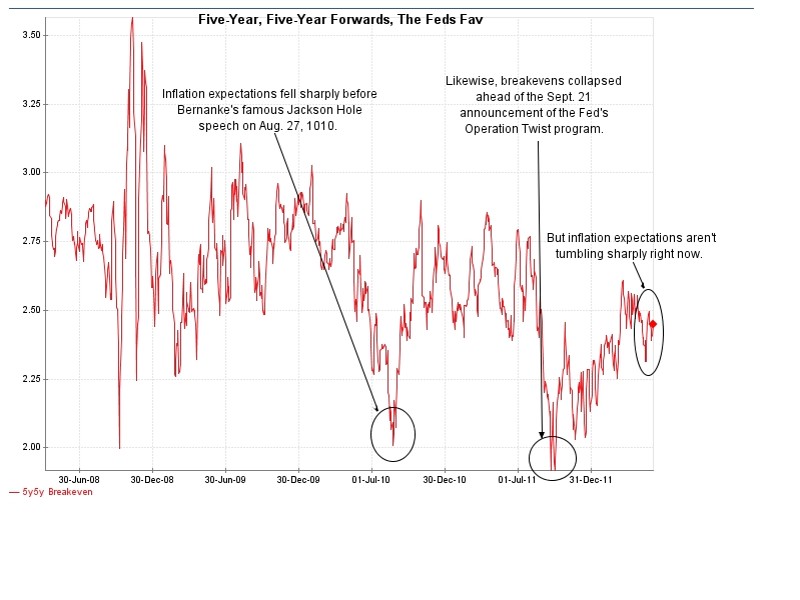

Fed Violates its Own Inflation Targets. Should QE3 Be Postponed?

Fed Violates its Own Inflation Targets. Should QE3 Be Postponed?16 Aug 2012

The win of the pro-bailout parties in the Greek elections was no win for the SNB

The win of the pro-bailout parties in the Greek elections was no win for the SNB25 Jun 2012

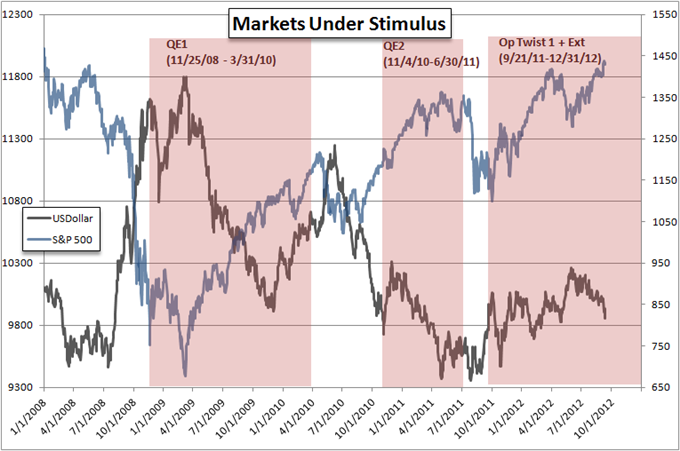

Quantitative Easing Indicators, June 2012

Quantitative Easing Indicators, June 201210 Jun 2012

The “Sell in May, come back in October” effect and its equivalent for the SNB9 Jun 2012

SNB switched from selling euros to buying euros, might sell GBP

SNB switched from selling euros to buying euros, might sell GBP30 May 2012