Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

9 Jun 2023

Weekly Market Pulse: First, Kill All The Speculators

Weekly Market Pulse: First, Kill All The Speculators31 Jan 2023

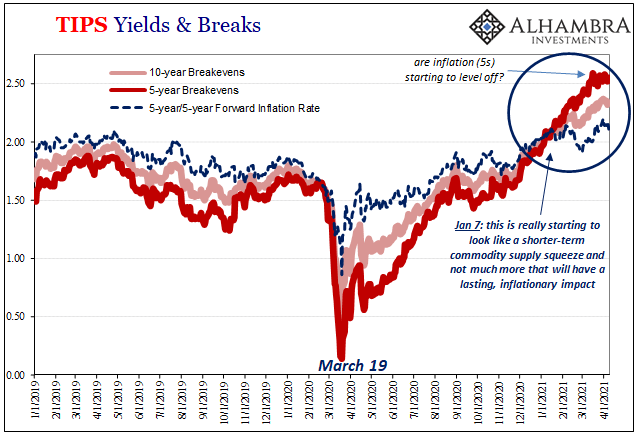

The Everything Data’s (Z1) Verdict: Not Inflation, Only More Of The Same

The Everything Data’s (Z1) Verdict: Not Inflation, Only More Of The Same26 Jun 2022

Collateral Shortage…From *A* Fed Perspective

Collateral Shortage…From *A* Fed Perspective7 May 2022

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’

I Told You It *Wasn’t* Money Printing; How The Fed Helped Cause, But Can’t Solve, Our Current ‘Inflation’21 Apr 2022

Goldilocks And The Three Central Banks

Goldilocks And The Three Central Banks7 Apr 2022

The Hawks Circle Here, The Doves Win There

The Hawks Circle Here, The Doves Win There26 Jan 2022

Start Long With The (long ago) End of Inflation

Start Long With The (long ago) End of Inflation24 Dec 2021

Weekly Market Pulse: Has Inflation Peaked?

Weekly Market Pulse: Has Inflation Peaked?13 Dec 2021

Weekly Market Pulse: Discounting The Future

Weekly Market Pulse: Discounting The Future7 Dec 2021

What Does Taper Look Like From The Inside? Not At All What You’d Think

What Does Taper Look Like From The Inside? Not At All What You’d Think5 Nov 2021

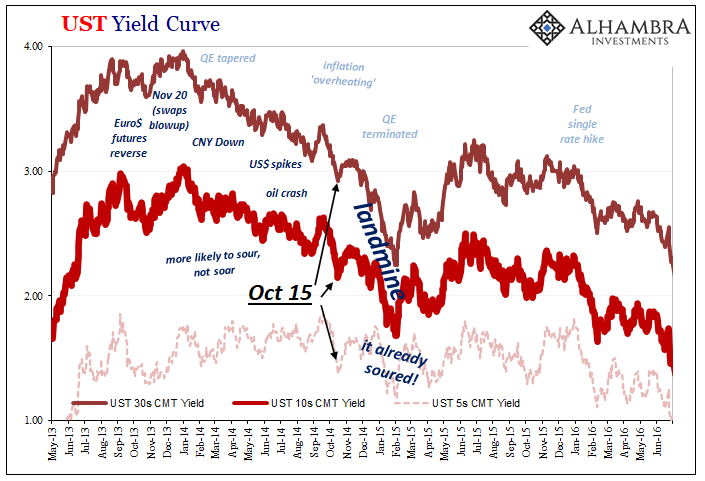

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)

The Real Tantrum Should Be Over The Disturbing Lack of Celebration (higher yields)3 Nov 2021

Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?

Bill Issuance Has Absolutely Surged, So Why *Haven’t* Yields, Reflation, And Other Good Things?2 Nov 2021

The Curve Is Missing Something Big

The Curve Is Missing Something Big21 Oct 2021

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation

The Great Eurodollar Famine: The Pendulum of Money Creation Combined With Intermediation13 Oct 2021

Tapering Or Calibrating, The Lady’s Not Inflating

Tapering Or Calibrating, The Lady’s Not Inflating7 Oct 2021

August Avoids Zero In JGB’s

August Avoids Zero In JGB’s28 Sep 2021

Taper *Without* Tantrum

Taper *Without* Tantrum17 Aug 2021

Rechecking On Bill And His Newfound Followers

Rechecking On Bill And His Newfound Followers9 Apr 2021

The Endangered Inflationary Species: Gazelles

The Endangered Inflationary Species: Gazelles11 Feb 2021