Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

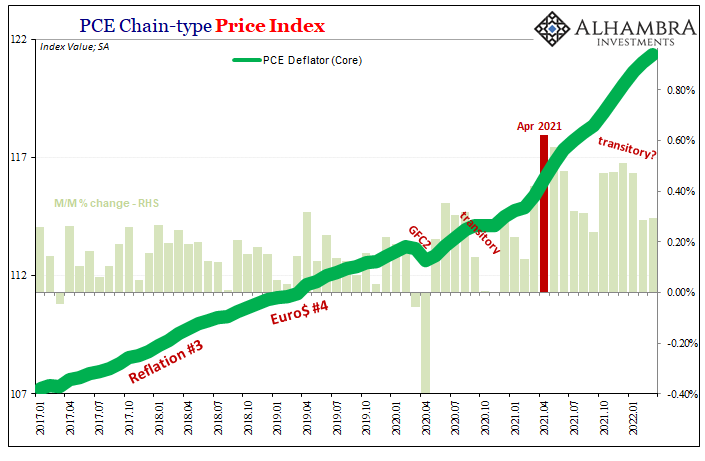

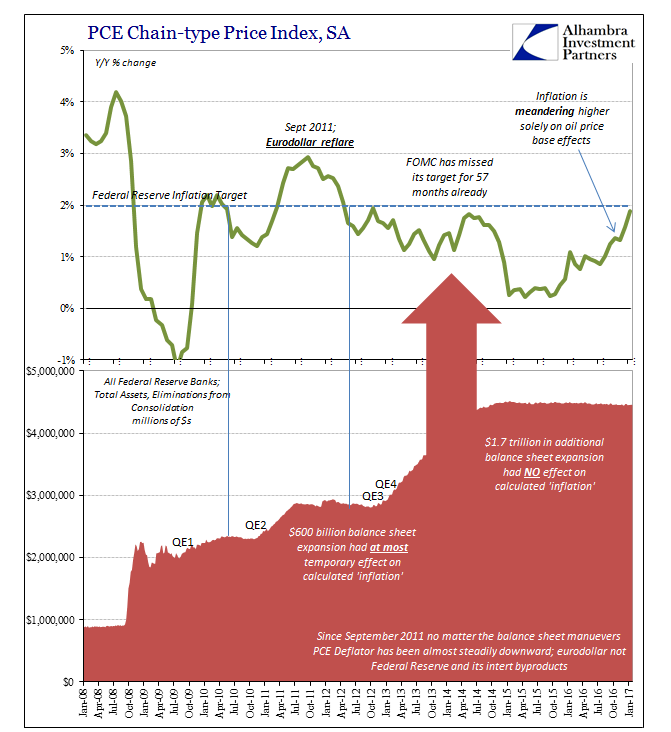

Some ‘Core’ ‘Inflation’ Difference(s)

Some ‘Core’ ‘Inflation’ Difference(s)6 May 2022

Is It Recession?30 Apr 2022

The Short, Sweet Income Case For Ugly Inversion(s), Too4 Apr 2022

White-Hot Cycles of Silence28 Dec 2021

Trying To Project The Goods Trade Cycle17 Dec 2021

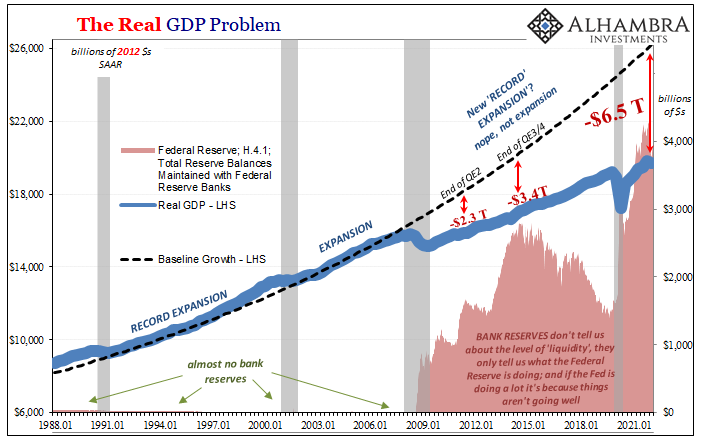

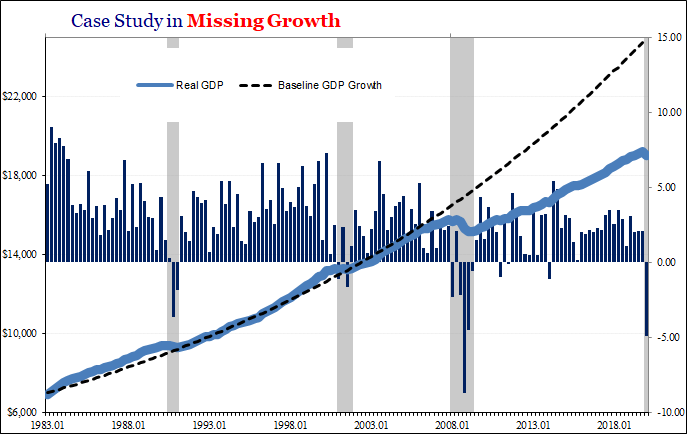

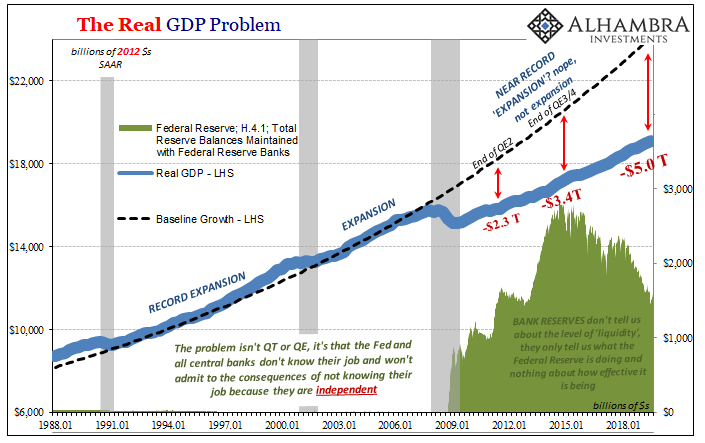

GDP Red Flag31 Oct 2021

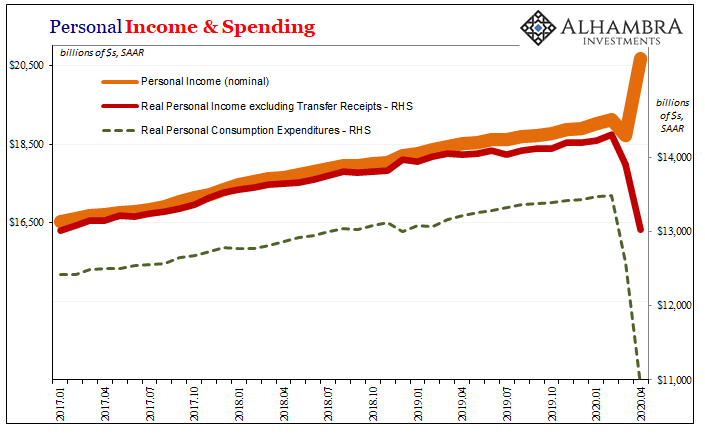

Personal Income and Spending: The Other Side1 Jun 2020

GDP + GFC = Fragile1 May 2020

Three Straight Quarters of 2 percent, And Yet Each One Very Different2 Feb 2020

Three (Rate Cuts) And GDP, Where (How) Does It End?1 Nov 2019

Bi-Weekly Economic Review: Investing Is Not A Game of Perfect11 Apr 2018

Can’t Hide From The CPI19 Nov 2017

The (Economic) Difference Between Stocks and Bonds4 Nov 2017

Incomes Are What Matters, So Bad Month, Bad Year, Bad Decade8 Oct 2017

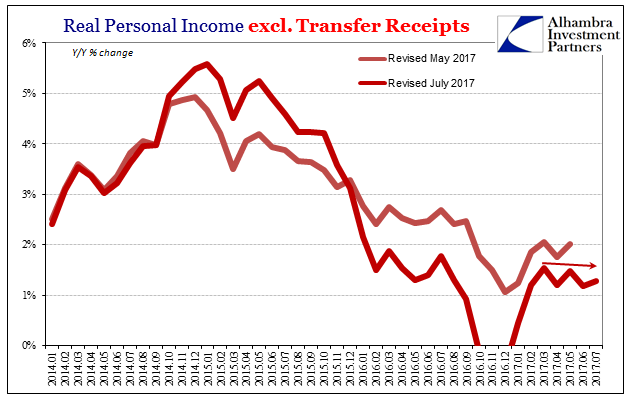

Proving Q2 GDP The Anomaly, Incomes Yet Again Fail To Accelerate5 Sep 2017

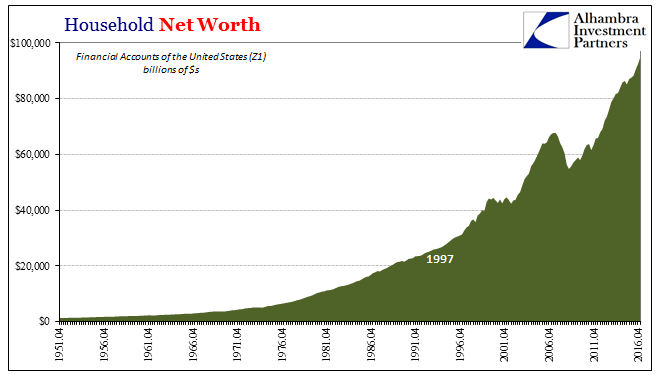

Wealth Paradox Not Effect18 Jun 2017

Real Disposable Income: Headwinds of the Negative3 Mar 2017

Quantitative Easing, Gold and the Swiss Franc27 Dec 2012