Read More »

On Swiss National Bank Main SNB Background Info

On Swiss National Bank Main SNB Background Info

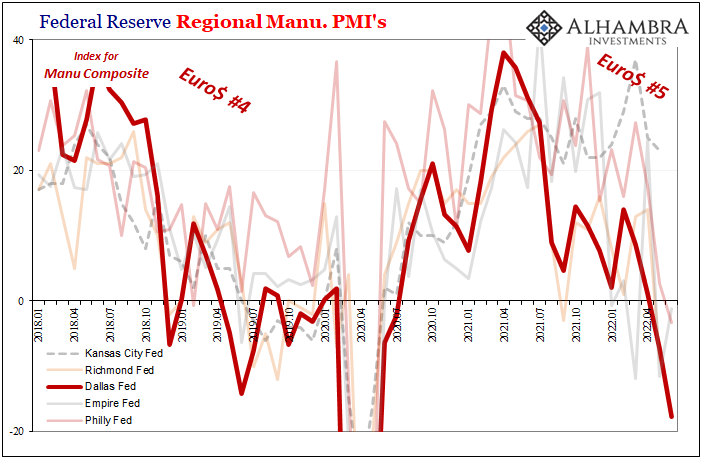

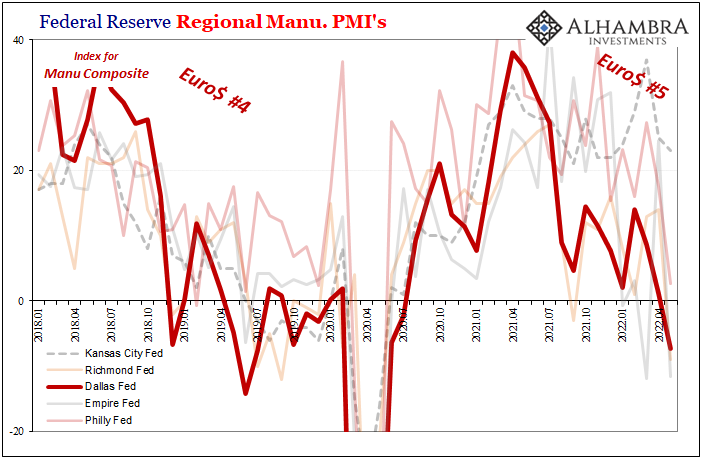

Weekly Market Pulse: A Most Unusual Economy

Weekly Market Pulse: A Most Unusual Economy11 Jul 2022

Demand Down, Supply Down, Ugly Up

Demand Down, Supply Down, Ugly Up3 Jul 2022

It’s Inventory PLUS Demand

It’s Inventory PLUS Demand30 Jun 2022

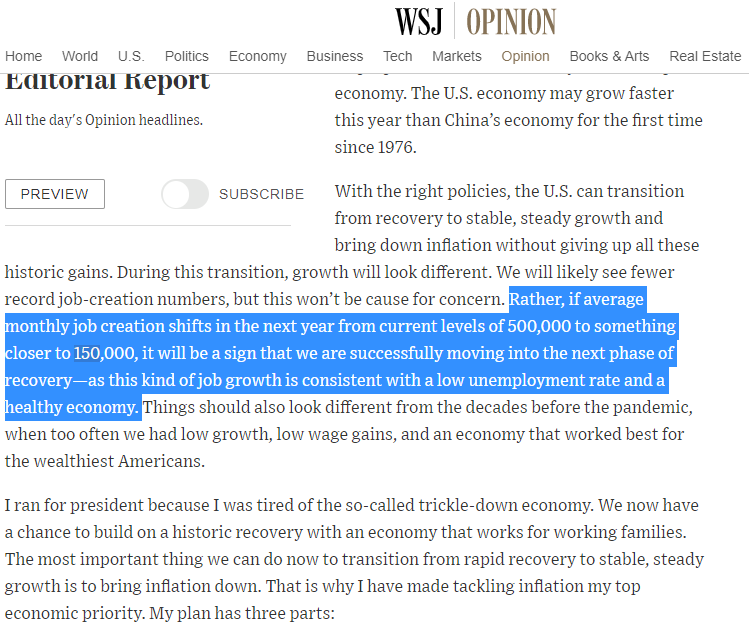

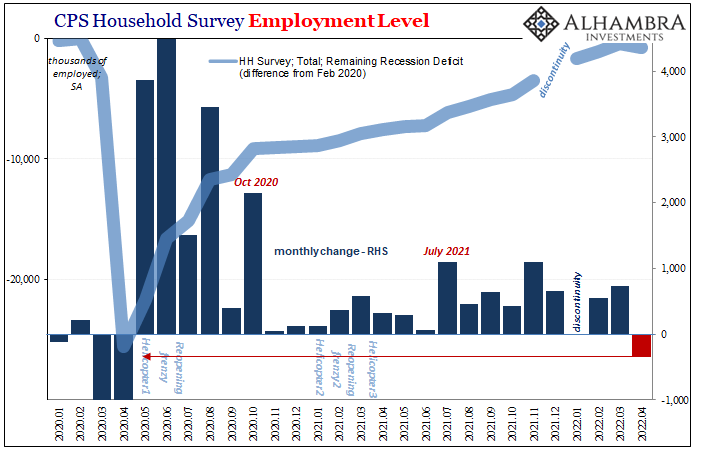

ADP Front-Runs BLS and President Phillips

ADP Front-Runs BLS and President Phillips4 Jun 2022

President Phillips Emerges To Reassure On Growing Slowdown

President Phillips Emerges To Reassure On Growing Slowdown2 Jun 2022

Another Month Closer To Global Recession

Another Month Closer To Global Recession26 May 2022

Worry Walls Don’t Explain Repeated Falls

Worry Walls Don’t Explain Repeated Falls9 Apr 2022

Far Longer And Deeper Than Just The Past Few Months

Far Longer And Deeper Than Just The Past Few Months20 Oct 2021

Surprise: It Isn’t Consumers Keeping American Factories Busy

Surprise: It Isn’t Consumers Keeping American Factories Busy5 Oct 2021

More About Less New Orders

More About Less New Orders3 Oct 2021

All Eyes On Inventory

All Eyes On Inventory24 Sep 2021

ISM’s Nasty Little Surprise Isn’t Actually A Surprise

ISM’s Nasty Little Surprise Isn’t Actually A Surprise7 Jul 2021

Another Round of Transitory: US Retail Sales & (revised) IP

Another Round of Transitory: US Retail Sales & (revised) IP16 Jun 2021

There’s Two Sides To Synchronize

There’s Two Sides To Synchronize3 Mar 2021

What Did Hamper Growth ‘In A Few Months’

What Did Hamper Growth ‘In A Few Months’18 Dec 2020

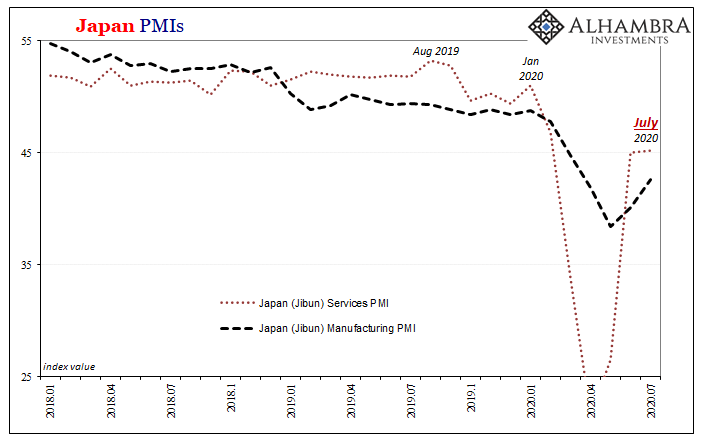

A Japanese Stall?

A Japanese Stall?24 Jul 2020

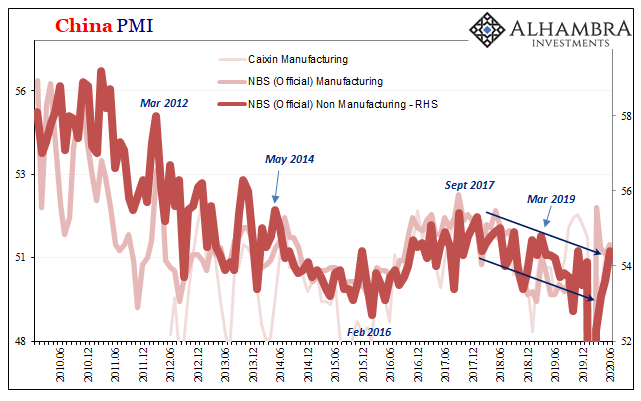

What The PMIs Aren’t Really Saying, In China As Elsewhere

What The PMIs Aren’t Really Saying, In China As Elsewhere1 Jul 2020

FX Daily, May 15: Much Talk but Little Action

FX Daily, May 15: Much Talk but Little Action15 May 2020

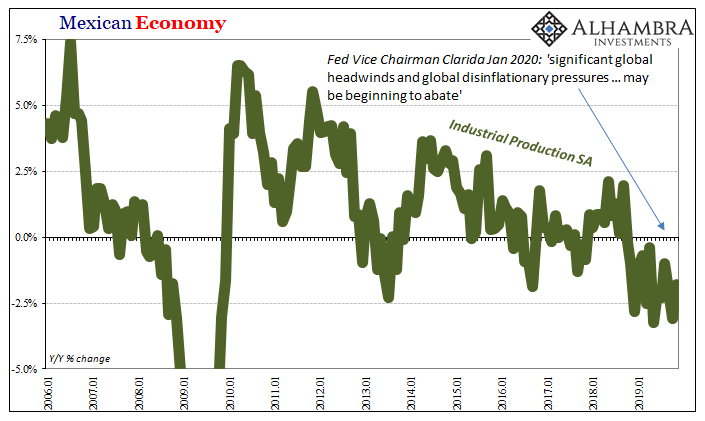

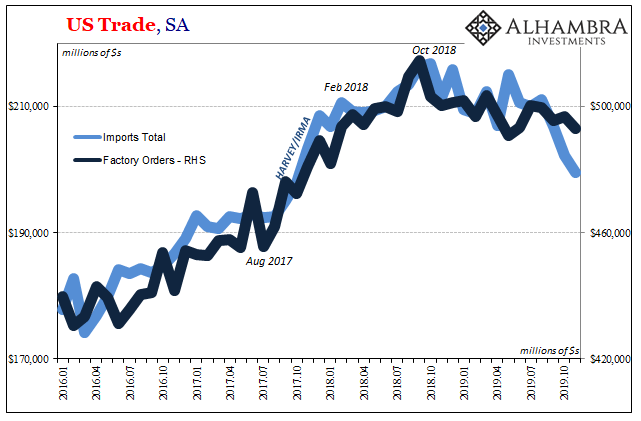

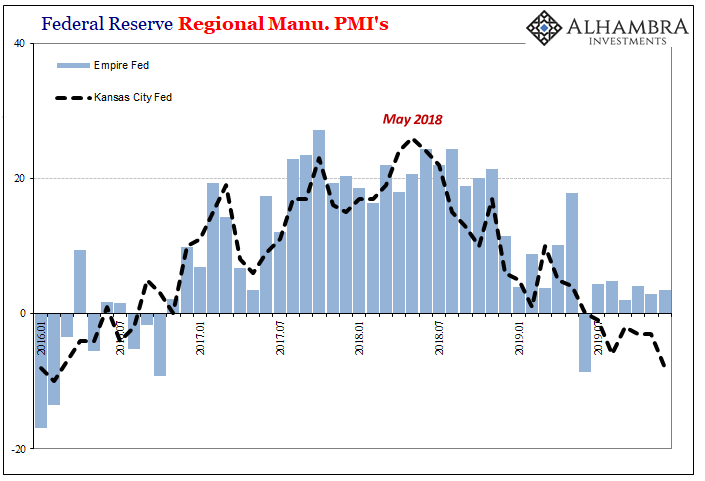

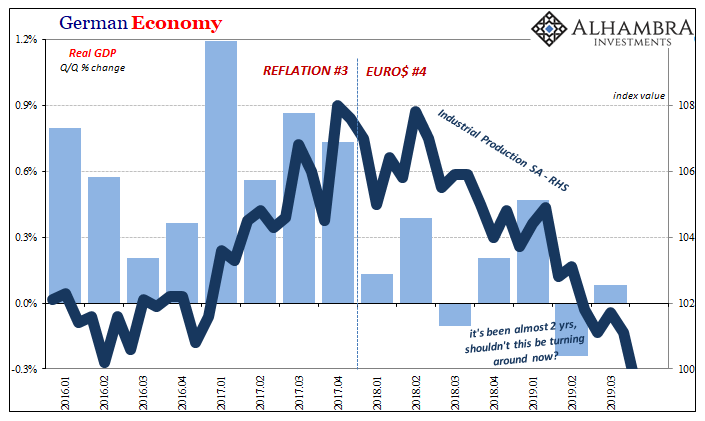

US Sales and Production Remain Virus-Free, But Still Aren’t Headwind-Free

US Sales and Production Remain Virus-Free, But Still Aren’t Headwind-Free18 Feb 2020

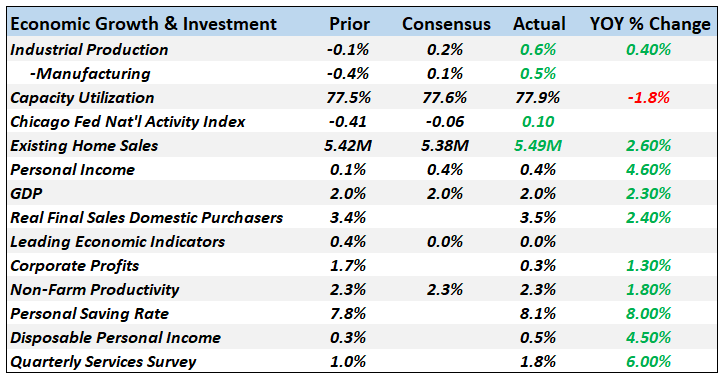

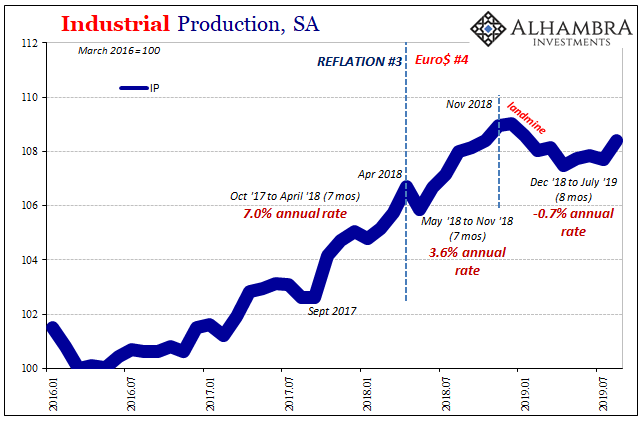

Two Years And Now It’s Getting Serious

Two Years And Now It’s Getting Serious11 Feb 2020