Read More »

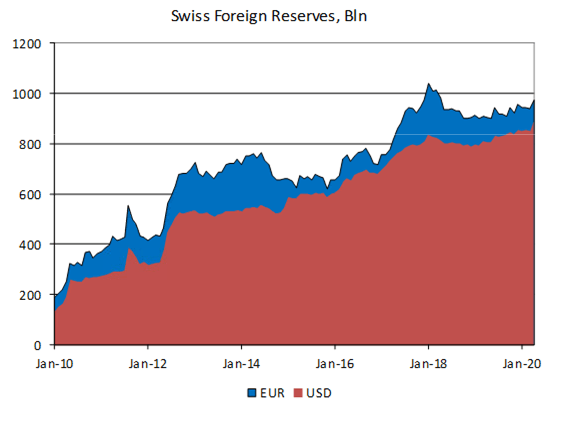

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

19 Jan 2021

21 Dec 2020

Some Thoughts on the Latest Treasury FX Report

Some Thoughts on the Latest Treasury FX Report18 Dec 2020

FOMC Preview

FOMC Preview15 Dec 2020

14 Dec 2020

30 Nov 2020

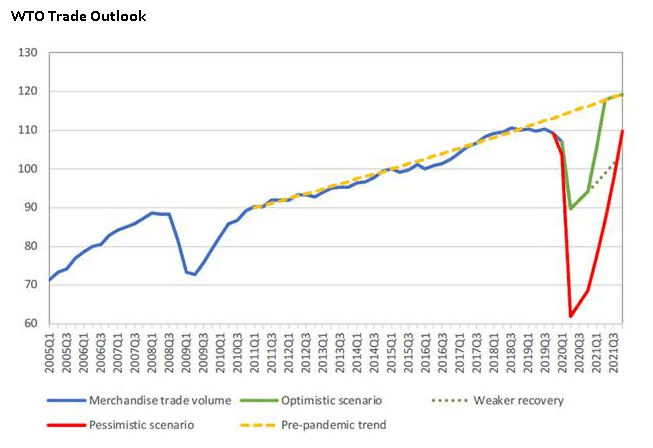

Roadblocks and Opportunities for International Trade in 2021

Roadblocks and Opportunities for International Trade in 202118 Nov 2020

16 Nov 2020

Vaccine and Split Government

Vaccine and Split Government11 Nov 2020

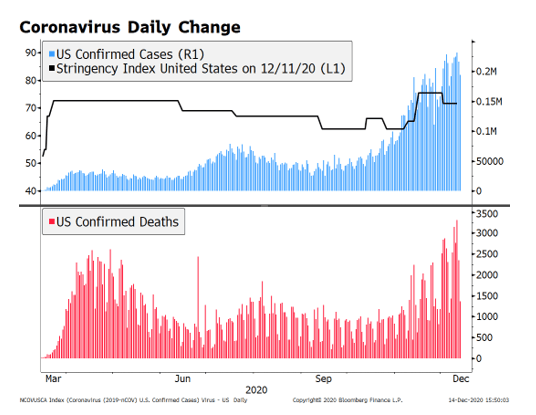

FOMC Preview: Coronavirus Daily Change

FOMC Preview: Coronavirus Daily Change4 Nov 2020

ECB Preview

ECB Preview28 Oct 2020

20 Oct 2020

12 Oct 2020

5 Oct 2020

ECB Preview

ECB Preview10 Sep 2020

31 Aug 2020

Where Has All the Carry Gone?

Where Has All the Carry Gone?21 Aug 2020

Recent Trade Developments Suggest Some Caution Ahead Warranted

Recent Trade Developments Suggest Some Caution Ahead Warranted27 Jun 2020

23 Jun 2020

SNB Preview

SNB Preview18 Jun 2020