Read More »

Tag Archive: developed markets

Drivers for the Week Ahead

Read More »

Drivers for the Week Ahead

Read More »

Some Thoughts on the Latest Treasury FX Report

Read More »

FOMC Preview

Read More »

Drivers for the Week Ahead

Read More »

Drivers for the Week Ahead

Read More »

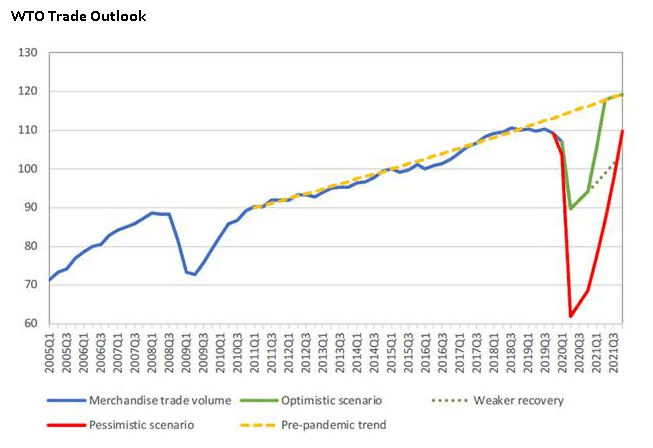

Roadblocks and Opportunities for International Trade in 2021

Read More »

Drivers for the Week Ahead

Read More »

Vaccine and Split Government

Read More »

FOMC Preview: Coronavirus Daily Change

Read More »

ECB Preview

Read More »

Drivers for the Week Ahead

Read More »

Drivers for the Week Ahead

Read More »

Drivers for the Week Ahead

Read More »

ECB Preview

Read More »

Drivers for the Week Ahead

Read More »

Where Has All the Carry Gone?

Read More »

Recent Trade Developments Suggest Some Caution Ahead Warranted

Read More »

Drivers for the Week Ahead

Read More »

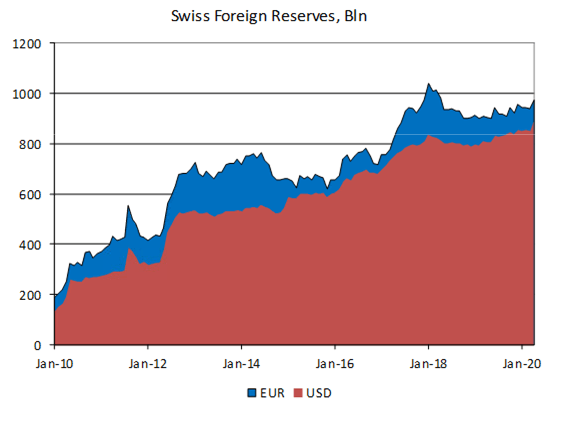

SNB Preview

Read More »

On Swiss National Bank

On Swiss National Bank

-

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

-

Household wealth in 2025

-

Heads up for NZD and CHF traders, RBNZ Gov Breman and SNB Chair Schlegel to speak

-

Swiss franc appreciation has led to tighter monetary conditions – SNB minutes

-

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

Main SNB Background Info

Featured and recent

-

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week -

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete -

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert!

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert! -

Steuerrecht digitalisieren mit KI – eine gute Idee?

Steuerrecht digitalisieren mit KI – eine gute Idee? -

Why Switzerland is launching a charm offensive in Southeast Asia

Why Switzerland is launching a charm offensive in Southeast Asia -

Ex-Raiffeisen bank CEO fined for tax evasion

Ex-Raiffeisen bank CEO fined for tax evasion -

The price of gold matters, but availability matters more.

The price of gold matters, but availability matters more. -

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich!

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich! -

India’s situation shows why physical gold is different from paper exposure.

India’s situation shows why physical gold is different from paper exposure. -

ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

More from this category

Drivers for the Week Ahead

Drivers for the Week Ahead19 Jan 2021

- Drivers for the Week Ahead

21 Dec 2020

- Some Thoughts on the Latest Treasury FX Report

18 Dec 2020

- FOMC Preview

15 Dec 2020

- Drivers for the Week Ahead

14 Dec 2020

- Drivers for the Week Ahead

30 Nov 2020

Roadblocks and Opportunities for International Trade in 2021

Roadblocks and Opportunities for International Trade in 202118 Nov 2020

- Drivers for the Week Ahead

16 Nov 2020

- Vaccine and Split Government

11 Nov 2020

- FOMC Preview: Coronavirus Daily Change

4 Nov 2020

- ECB Preview

28 Oct 2020

- Drivers for the Week Ahead

20 Oct 2020

- Drivers for the Week Ahead

12 Oct 2020

- Drivers for the Week Ahead

5 Oct 2020

- ECB Preview

10 Sep 2020

- Drivers for the Week Ahead

31 Aug 2020

- Where Has All the Carry Gone?

21 Aug 2020

- Recent Trade Developments Suggest Some Caution Ahead Warranted

27 Jun 2020

- Drivers for the Week Ahead

23 Jun 2020

- SNB Preview

18 Jun 2020