The two-day FOMC meeting starts tomorrow and wraps up Wednesday afternoon. While no policy changes are expected, we highlight what the Fed may or may not do. We expect a dovish hold, with Powell underscoring the growing downside risks facing the US economy in the coming months.

| RECENT DEVELOPMENTS

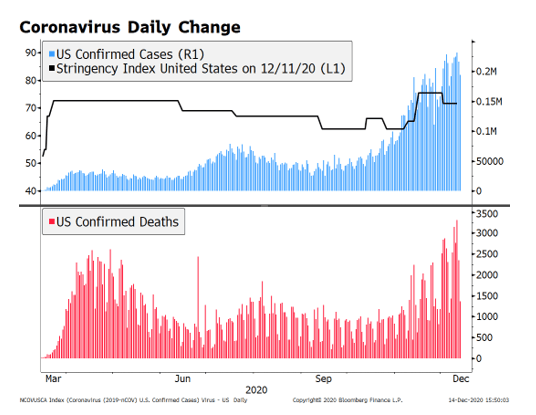

The US outlook has worsened since the November FOMC meeting. Infection numbers are making new highs with no sign of abating. There is no national strategy to contain the virus, so we are getting a hodgepodge of state level responses. With the pandemic stretching on, markets are realizing that the current phase of the recovery is stalling out right now, and that the full recovery will be pushed out further into next year with the likelihood of tighter restrictions ahead. We are already seeing this in the data. The November jobs gain of 245k was the lowest since the recovery began. Initial weekly jobless claims, both regular and PUA, have begun climbing noticeably now that more lockdowns are taking effect. There is no consensus reading yet for December jobs but if the weekly claims continue to rise, we cannot rule out a negative NFP number. Not surprisingly, retail sales data are weakening from a combination of rising job losses coupled with the loss of unemployment benefits. That may get worse at month-end as more emergency benefits expire. So far, the fiscal stimulus proposals fall short of what was put in place earlier this year with the CARES Act. The fiscal stimulus outlook remains uncertain, but the odds of a positive outcome are high, even if modest. The bipartisan group of lawmakers will unveil full details of its $908 bln package today and reports suggest it will be split into two bills. One will just include liability protections and aid to state and local governments while the other will contain everything else. In a sense, this accomplishes what Senate Leader McConnell suggested by peeling off the two problem areas that will now be decided as standalones. It’s unclear whether Democratic leaders will go along with this, though. However, if this strategy works to get the bulk of the stimulus funds passed, we are probably looking at something around $750 bln. That’s not great but it’s definitely better than nothing. |

Coronavirus Daily Change, 2020 - Click to enlarge |

| Chances of more stimulus next year depends in large part on the Georgia special elections. They will both be held January 5 and control of the Senate rests on the outcomes. The Democrats need to win both seats to control the Senate, as the 50-50 tie would lead Vice President-elect Harris to cast any tie-breaking vote. Polls are showing both races as toss-ups, though at this point, no one really trusts the polls. Betting markets currently have 32% odds that the Democrats will control both houses of Congress and so the Blue Wave seems like tail risk, at least for now.

We believe that the outlook for Fed policy in 2021 critically depends on what is done on the fiscal side. Massive US Treasury issuance under a Blue Wave scenario is unlikely to be fully absorbed by the private sector. This will require the Fed to adjust its asset purchases, further blurring the line between fiscal and monetary policy. The dollar tends to come under pressure as markets pricing in a new round of QE, before recovering. This time around, that recovery will be made more difficult by the rise of infections across the nation. As Fed Chair Powell has said countless times, there can be no sustainable economic recovery until the virus is under control. |

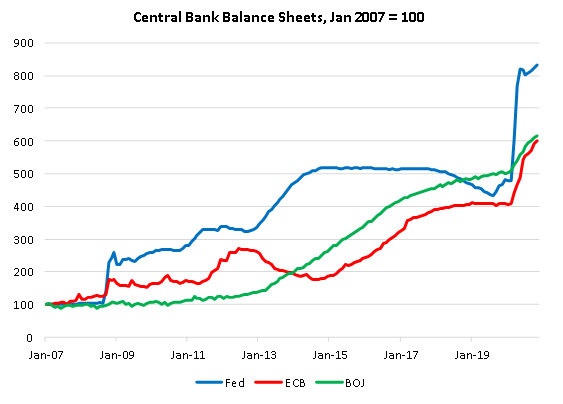

Central Bank Balance Sheet, Jan 2007-2019 - Click to enlarge |

WHAT ELSE CAN THE FED DO?

Despite the aggressive measures taken by the Fed so far, it still has some tools at its disposal. Here, we look at several moves that the Fed could make in the coming months if needed.

- Tweak existing loan and liquidity programs – POSSIBLE AT ANY TIME. Last month, the Fed announced that it was lowering the minimum loan amount for its Main Street Program to $100k from $250k previously. This wasn’t the first time that the Fed has tweaked its lending and liquidity programs just days before an FOMC meeting. The move just underscores that the Fed is not constrained by the calendar and will act whenever it sees a need. That said, the Main Street Lending Program is one of several emergency programs that will now expire at the end of this month, something the Fed is not happy about. It’s likely that the Fed will pledge to work with Congress to restart any and all of those expiring programs if conditions warrant.

- Tweak its macro forecasts – POSSIBLE NOW, POSSIBLE IN 2021. The Fed last updated its Summary of Economic Projections at the September meeting. 2023 was added to the forecast horizon then and the Dot Plots see steady policy for another year. That should not change at this meeting. The median GDP forecasts from September (June) were -3.7% (-6.5%) in 2020, 4.0% (5.0%) in 2021, 3.0% (3.5%) in 2022, and 2.5% in 2023 while the median core PCE forecasts were 1.5% (1.0%) in 2020, 1.7% (1.5%) in 2021, 1.8% (1.7%) in 2022, and 2.0% in 2023. Some of the nearby forecasts may be shaved a bit in light of the rising virus numbers, though some of the longer-term forecasts could be boosted a bit in light of the vaccine rollout. When all is said and done, we suspect Powell will continue to highlight downside risks due to the spread of the virus and lack of fiscal stimulus.

- Tweak its forward guidance – UNLIKELY NOW, LIKELY IN 2021. The Fed just updated its forward guidance at the September meeting to incorporate its new policy framework, and so we think it’s too soon to expect another change. Recall that “The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2% and is on track to moderately exceed 2% for some time.” This is about as explicit as outcome-based forward guidance can get and yet it still leaves the Fed with a lot of wiggle room. The phrases “moderately exceed” for “some time” are suitably vague. There’s really no need to update this forward guidance anytime soon. Only when inflation remains elevated will the Fed be called on to better define “moderately exceed” for “some time” and we are a long way from that. Some analysts are looking for the Fed to set these out more explicitly but quite honestly, we see little to be gained by doing that now.

- Adjust asset purchases – UNLIKELY NOW, POSSIBLE IN 2021 IF AGGRESSIVE FISCAL STIMULUS PASSED. QE was initially ramped up in March to help keep markets functional. However, at the September meeting, the FOMC committed using QE to “maintain an accommodative stance of monetary policy.” It’s a subtle shift but a noteworthy one. For now, the Fed’s asset purchases remain on autopilot with the Fed currently buying $80 bln of US Treasuries and $40 bln of mortgage-backed securities each month. This has led the Fed’s balance sheet to increase to a record-high $7.24 trln in early December, a 74% increase from end-2019. We posit that the Fed’s QE will have to increase if there is a Blue Wave that leads to aggressive fiscal stimulus. Debt issuance would spike and we think the natural tendency would be for long rates to rise. It would fall on the Fed to prevent such a rise by boosting QE. Purchases are currently spread out evenly across the maturity spectrum. Another possibility for the Fed is to shift its purchase more towards the long end but this would fall short of explicit YCC (see below).

- Introduce Yield Curve Control – VERY UNLIKELY NOW, POSSIBLE IN 2021 AND BEYOND IF LONG RATES RISE TOO MUCH. Since the September FOMC decision and the updated forward guidance, there has been nary a mention of YCC in official commentary. Note that the 10-year yield traded at 0.98% earlier this month, the highest since March and possibly on its way to test the March 19 high near 1.27%. We do not think the Fed will be happy with a much steeper yield curve and may offer some verbal pushback. That said, we think the Fed remains far from instituting official YCC. If perceived improvements in the US economy were to push US yields significantly higher, then we think there would first be a series of QE changes highlighted above. We think YCC would only become more likely if these more “traditional” asset purchases fail to halt that rise in yields. The Fed simply does not want tighter financial conditions over the next several years. Period.

- Negative interest rates – VERY UNLIKELY. Not one current FOMC member has advocated negative interest rates yet. Indeed, minutes from recent FOMC meetings show that the concept isn’t even being actively discussed. Uber-dove and former Minneapolis Fe d President Kocherlakota is the only Fed official that we can recall (past or present) that has advocated for negative rates. Simply put, there is no hard evidence that negative rates work and there is of course risks of lower bank profitability and damaging the financial system. WIRP shows no market expectations for negative rates.

| INVESTMENT OUTLOOK

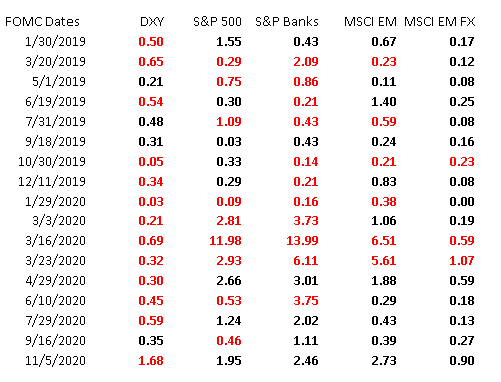

The dollar tends to weaken on recent FOMC decision days. In 2019, DXY weakened on five of the eight FOMC meeting days. Of the nine so far this year, DXY has weakened on eight of them. Stocks are a different matter this year, with the S&P falling six times and rising three times. MSCI EM has a record of six gains and three losses, while MSCI EM FX has fared slightly better with only two losses out of nine. |

. |

| We believe most of the dollar’s recent bounces have been due purely to positioning and sporadic safe haven demand. Fundamentally speaking, the US outlook has gotten worse with the continued rise in viral infections. At this point, the US is more likely than Europe to fall behind the curve in containing the current wave. The inability of Congress to pass another round of stimulus only complicates matters, possibly shifting the burden of adjustment to the Fed. We expect the Fed to deliver a dovish hold this week that underscores why investors should not be counting on a stronger dollar anytime soon.

Here are our currency targets. DXY broke below the December 4 low near 90.476 today and we continue to target the February 2018 low near 88.253 for DXY. The euro is holding above $1.2150 and we continue to target the February 2018 high near $1.2555. Sterling continues to be buffeted by Brexit concerns but a successful deal should see it break above $1.35 and make a run at the April 2018 high near $1.4375. USD/JPY finally made a clean break below 104 and is back on track to test the November low near 103.20. Break below that would set up a test of the March low near 101.20. |

Dollar Spot Performance, 2020 - Click to enlarge |

Why do we remain negative on the dollar? We note that the dollar typically does poorly at the onset of each round of QE before eventually recovering. Looking back to the financial crisis, the Fed first started Quantitative Easing (QE) in November 2008 when it announced plans to purchase $600 bln of agency mortgage-backed securities (MBS). DXY fell around 12% over the next month but then recovered to trade even higher by March 2009. QE1 was extended in March 2009 with another round of agency MBS purchases worth $750 bln as well as $300 bln worth of longer-dated US Treasuries. DXY fell around 17% over the next eight months but then recovered nearly all its losses by June 2010. In addition, we think the global investors are in the process of diversifying away from US assets, especially away from US equities. Moreover, we expect increasing hedging demand by foreign investors holding US assets to accelerate the dollar’s cyclical move lower.

This time around, the Fed announced unlimited QE on Monday March 23. It’s not a coincidence that the dollar peaked the previous Friday, with DXY putting in a cyclical top near 103. Since then, DXY has fallen around 12%. The euro bottomed on March 23 near $1.0635 and has since climbed around 14%. Sterling had done even better, climbing around 17% from its March 20 low near $1.1410, while the yen has been the laggard, rising around 7% since late March.

What usually turns the dollar around after subsequent bouts of QE is the recovery in the US economy. We are not getting that now due to our failure to control the virus that has kept large swathes of the country from fully reopening. If and when the virus is under control, that is when the economy (and the dollar) could stage a sustainable recovery. But we are nowhere near that yet.

Full story here Are you the author?Tags: Articles,developed markets,Featured,newsletter