Read More »

Tag Archive: Articles

EM Preview for the Week Ahead

Read More »

Dollar Remains Soft as Risk-On Sentiment Continues

Read More »

Dollar Soft Despite Heightened Geopolitical Risks

Read More »

Drivers for the Week Ahead

Read More »

Musings on the Repo Market, Fed Policy, and the US Economy

Read More »

Drivers for the Week Ahead

Read More »

Dollar Firm as US Economy Continues to Outperform

Read More »

Dollar Firm Despite Rising US Political Uncertainty

Read More »

Dollar Firm as Risk-Off Impulses Return

Read More »

EM Preview for the Week Ahead

Read More »

Dollar Mixed on Central Bank Thursday

Read More »

Some Thoughts on the Fed and Oil Shocks

Read More »

Dollar Mixed, Oil Spikes as Markets Digest Saudi Attack

Read More »

Dollar Soft as Risk Sentiment Stoked Ahead of US Retail Sales

Read More »

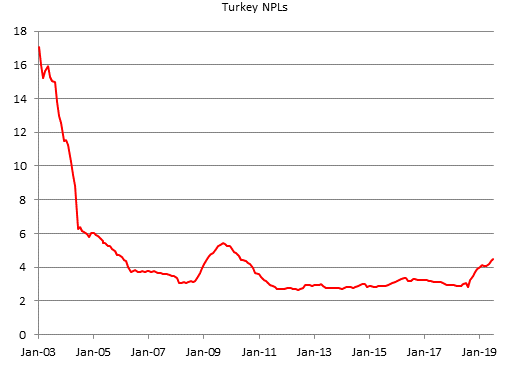

Turkey Monetary Policy Planting Seeds of Future Crisis

Read More »

EM Preview for the Week Ahead

Read More »

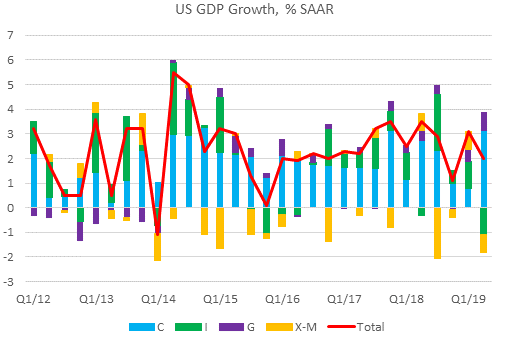

Latest Thoughts on the US Economic Outlook

Read More »

Drivers for the Week Ahead

Read More »

Emerging Markets: FX Model for Q3 2019

Read More »

Dollar Firm as Markets Calm

Read More »

On Swiss National Bank

On Swiss National Bank

-

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

-

Household wealth in 2025

-

Heads up for NZD and CHF traders, RBNZ Gov Breman and SNB Chair Schlegel to speak

-

Swiss franc appreciation has led to tighter monetary conditions – SNB minutes

-

SNB’s Chairman Schlegel: A few months of negative inflation wouldn’t be a problem

Main SNB Background Info

Featured and recent

-

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week

SNB Sight Deposits: decreased by 2.2 billion francs compared to the previous week -

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete -

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert!

-40 Kilo! Ricarda Lang feiert Abnehmerfolg! Das Internet feiert! -

Steuerrecht digitalisieren mit KI – eine gute Idee?

Steuerrecht digitalisieren mit KI – eine gute Idee? -

Why Switzerland is launching a charm offensive in Southeast Asia

Why Switzerland is launching a charm offensive in Southeast Asia -

Ex-Raiffeisen bank CEO fined for tax evasion

Ex-Raiffeisen bank CEO fined for tax evasion -

The price of gold matters, but availability matters more.

The price of gold matters, but availability matters more. -

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich!

FATAL: EU Chefdiplomatin blamiert ganz Europa! China außer sich! -

India’s situation shows why physical gold is different from paper exposure.

India’s situation shows why physical gold is different from paper exposure. -

ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

ZUGRIFF auf dein Vermögen: So schützen sich INSIDER

More from this category

Dollar Consolidates Its Gains Ahead of Jobs Report

Dollar Consolidates Its Gains Ahead of Jobs Report5 Feb 2021

Dollar Remains Firm Despite Dovish Fed Hold

Dollar Remains Firm Despite Dovish Fed Hold28 Jan 2021

Dollar Trading Sideways as FOMC Meeting Begins

Dollar Trading Sideways as FOMC Meeting Begins26 Jan 2021

Dollar Flat as Markets Await Fresh Drivers

Dollar Flat as Markets Await Fresh Drivers25 Jan 2021

Dollar Weakness Continues Ahead of ECB Decision

Dollar Weakness Continues Ahead of ECB Decision22 Jan 2021

Dollar Continues to Soften Ahead of Inauguration

Dollar Continues to Soften Ahead of Inauguration21 Jan 2021

Drivers for the Week Ahead

Drivers for the Week Ahead19 Jan 2021

Dollar Regains Some Traction as Markets Search for Direction

Dollar Regains Some Traction as Markets Search for Direction14 Jan 2021

Dollar Runs Out of Steam as Sterling Leads the Way

Dollar Runs Out of Steam as Sterling Leads the Way12 Jan 2021

- Drivers for the Week Ahead

21 Dec 2020

Dollar Continues to Soften Ahead of FOMC Decision

Dollar Continues to Soften Ahead of FOMC Decision20 Dec 2020

Some Thoughts on the Latest Treasury FX Report

Some Thoughts on the Latest Treasury FX Report18 Dec 2020

FOMC Preview

FOMC Preview15 Dec 2020

- Drivers for the Week Ahead

14 Dec 2020

Dollar Rally Running Out of Steam Ahead of ECB Decision

Dollar Rally Running Out of Steam Ahead of ECB Decision10 Dec 2020

Jittery Markets Keep the Dollar Afloat (For Now)

Jittery Markets Keep the Dollar Afloat (For Now)9 Dec 2020

Dollar Stabilizes but Weakness to Resume

Dollar Stabilizes but Weakness to Resume5 Dec 2020

Dollar Plumbs New Depths With No Relief In Sight

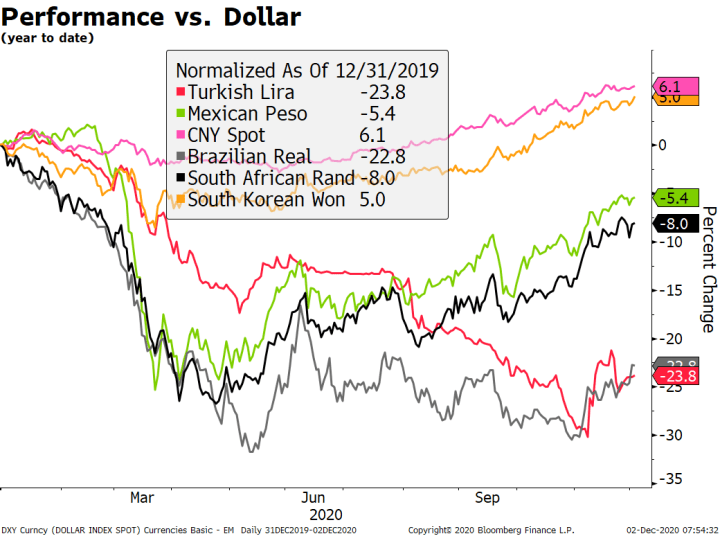

Dollar Plumbs New Depths With No Relief In Sight3 Dec 2020

- Drivers for the Week Ahead

30 Nov 2020

Dollar Consolidates Ahead of Thanksgiving Holiday

Dollar Consolidates Ahead of Thanksgiving Holiday28 Nov 2020