Read More »

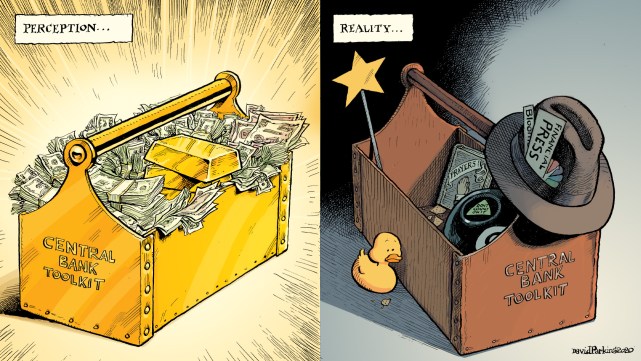

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

Eil: Jetzt Blockiert die USA die Straße von Hormus! Verhandlungen gescheitert! Krieg geht weiter!

Eil: Jetzt Blockiert die USA die Straße von Hormus! Verhandlungen gescheitert! Krieg geht weiter!12 Apr 2026

LEAK: EU-Elite geben Zerstörung Deutschlands offen zu!

LEAK: EU-Elite geben Zerstörung Deutschlands offen zu!12 Apr 2026

Sachsen-Anhalt: Siegmund zerlegt Antifanten! “Bald müssen sie einer ehrlicher Arbeit nachgehen!

Sachsen-Anhalt: Siegmund zerlegt Antifanten! “Bald müssen sie einer ehrlicher Arbeit nachgehen!12 Apr 2026

“Politisches Erdbeben in Irland! Wir haben die Schnauze voll!” TOTAL-Eskalation in Irland!

“Politisches Erdbeben in Irland! Wir haben die Schnauze voll!” TOTAL-Eskalation in Irland!12 Apr 2026

„Schlanke Kinder, die ein bisschen doof sind.“ – Jörg Thadeusz über Daniel Günther

„Schlanke Kinder, die ein bisschen doof sind.“ – Jörg Thadeusz über Daniel Günther12 Apr 2026

Anteil unbesetzter Stellen in EU-Ländern

Anteil unbesetzter Stellen in EU-Ländern12 Apr 2026

MSCI Emerging Markets schlägt MSCI World: Must-have im Portfolio?

MSCI Emerging Markets schlägt MSCI World: Must-have im Portfolio?12 Apr 2026

Saidis Geld-Setup 2026

Saidis Geld-Setup 202612 Apr 2026

Ranking Auslandskonten #thorstenwittmann #auslandskonten #auswandern #finanzstrategien

Ranking Auslandskonten #thorstenwittmann #auslandskonten #auswandern #finanzstrategien12 Apr 2026

Telekom vs. Vodafone vs. O2: So gut ist das Netz in Stadt und Land

Telekom vs. Vodafone vs. O2: So gut ist das Netz in Stadt und Land12 Apr 2026

Achtung: BlackRock wettet GEGEN Deutschen Staat!

Achtung: BlackRock wettet GEGEN Deutschen Staat!11 Apr 2026

The Importance of the Health U.S.-China relations and of Our Oceans

The Importance of the Health U.S.-China relations and of Our Oceans11 Apr 2026

Ich brech weg: Kamala Harris will wieder Präsidentin werden!

Ich brech weg: Kamala Harris will wieder Präsidentin werden!11 Apr 2026

2 Multimillionäre beantworten, wie du reich wirst!

2 Multimillionäre beantworten, wie du reich wirst!11 Apr 2026

Collien Fernandes Medienkampagne ist vorbei aber Carolin Kebekus ist ganz wütend!

Collien Fernandes Medienkampagne ist vorbei aber Carolin Kebekus ist ganz wütend!11 Apr 2026

FILZ-ALARM: SPD-VEREIN pleite – WO ist das ganze Geld hin?!

FILZ-ALARM: SPD-VEREIN pleite – WO ist das ganze Geld hin?!11 Apr 2026

Deine Lebensversicherungs-Fonds gehören dir nicht?! #thorstenwittmann #finanzstrategien #geldpolitik

Deine Lebensversicherungs-Fonds gehören dir nicht?! #thorstenwittmann #finanzstrategien #geldpolitik11 Apr 2026

Total-Eskalation! Das überlebt die Regierung nicht!

Total-Eskalation! Das überlebt die Regierung nicht!11 Apr 2026

„Wir werden von Idioten regiert“ – klare Ansage von Monica Gruber

„Wir werden von Idioten regiert“ – klare Ansage von Monica Gruber11 Apr 2026

Nullsummenglaube ist die Basis von Neid!

Nullsummenglaube ist die Basis von Neid!11 Apr 2026