Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

The relentless pounding that investors suffered in the first two weeks of the year has subsided. It is too early to have much confidence that a turn is at hand. By various measures, the sell-off had stretched the technical condition. In any event, the stability of the yuan, gains in the Chinese stocks, and a bounce in oil prices appears to be giving the bears a day off.

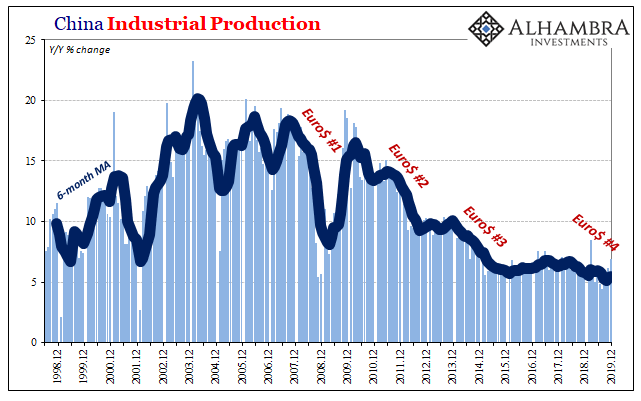

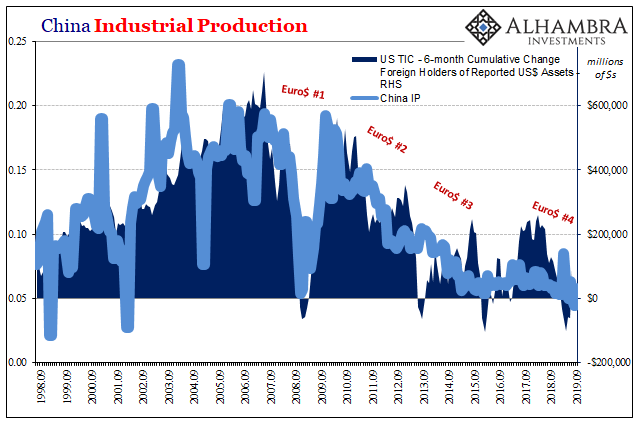

Chinese economic data (Q4 GDP, retail sales, industrial output, and fixed asset investment were a little softer than expected. The data are reported to a tenth of a decimal point, but this gives a misleading impression of the precision. While many are particularly skeptical of the accuracy of the GDP measure (6.8% year-over-year, down from 6.9% in Q3), many other estimates do not put growth that far from the official estimate, though of course there are some who claim China is growing at less than half the reported pace.

Even if we concede the likelihood that Chinese growth is slower than the official estimate, we suggest the overall size of the economy may be larger than reported. There is a range of activity, like in other countries, that may not be including in the calculations. We also note that China has agreed to adopt a more robust data collection procedure of the IMF.

The US offers a contrasting approach. The US will report Q1 GDP later this month. It will then be revised, often to a statistically significant degree, over the next few months, and then revised for several years. It seems that the main difference is that people suspect that the Chinese data is not reliable because of political considerations, while the US, the data is not reliable due to technical competence (the difficulty in measuring GDP of such large and complicated economy).

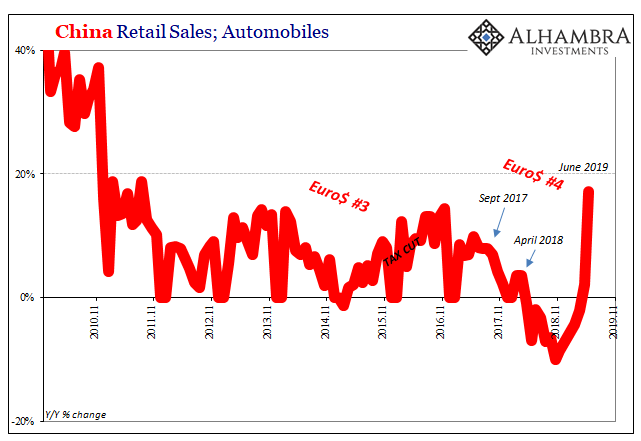

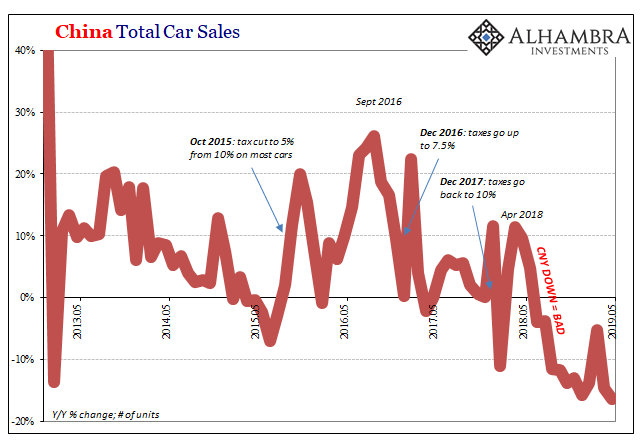

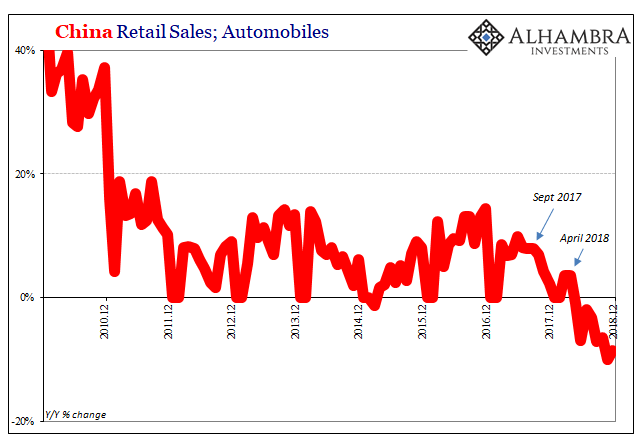

While the slowing of industrial output (5.9% year-over-year vs. 6.2% in November and 8% in December 2014) may be part of the transition toward services, we caution that deflation at the wholesale level (producer prices have been contracting for four years) and inflation in services may be contributing to the apparent shift. Separately, Chinese retail sales slowed to 11.1% (year-over-year) from 11.2% in November, which was the strongest rate in 2015). Still, in a world that suffers from insufficient aggregate demand, such strength is the envy of many.

The Shanghai Composite advanced by 3.2% and Shenzhen by 3.6%. This helped spur the regional advance and carried over to Europe, where the Dow Jones Stoxx 600 is up 1.8% near midday in London. European shares are being led higher by materials, information technology and energy. MSCI Emerging market equity index is up about 1.5%. . It has not closed above its five-day moving average since Christmas. It comes in near 716.1 today. The high thus far is 715.4.

The price of oil fell yesterday, weighed down by the lifting of sanctions on Iran. Reports have indicated that in anticipation, the Iranians were using 18 tankers as floating storage. They contained estimated 12 mln barrels of oil and 24 mln barrels of condensate. However, part of the decline in oil prices in recent weeks may have reflected this being discounted.

Of note, CNOOC, China's largest offshore oil and gas producer, announced that it would reduce output for the first time in more than a decade. A statement issued to the HK stock exchange earlier today indicated it would produce 470-485 mln barrels (oil equivalent) down from 495 mln barrels in 2015.

Although many narratives put the US shale or Canadian tar sands, or Russian output in the cross hairs of the Saudi strategy, in truth, the aim primarily non-OPEC producers, including China. There is the of an OPEC meeting for next month, but the calls seem the loudest from the traditionally high-cost OPEC producers, and those seeking concessions from Saudi Arabia (e.g. Iran).

The news stream for the major currencies has been limited. The main feature includes the UK's December CPI. It rose to 0.2% year-over-year from 0,1%. The core rate ticked up to 1.4% from 1.2% to stand at its highest level in a year. Some of this increase was due to the base effect. For example, motor fuel did not fall as much in December 2015 as it fell in December 2014. Airfares jumped.

BOE Governor Carney speaks later today and tomorrow the UK releases its employment. Earnings growth is expected to slow. Expectations for a BOE rate hike have been pushed into late this year. Between yesterday and today, the implied yield of the December short-sterling futures has risen nine basis points. This helping steady sterling. It also has not managed to settle above its five-day average since late last year. It is found near $1.4325 today. Intraday support is pegged near $1.4260-80.

The eurozone reported November current account figures. The 26.4 bln surplus was in line with the six- and 12-month averages. The December advance CPI was confirmed at 0.2% year-over-year (that same as the UK's) while the core rate is steady at 0.9%. The new news was the ZEW survey of investor confidence that fell to 22.7 from 33.9. It is the lowest since November 2014. The DAX was down over 10% this year coming into today's session. That alone, leave aside the refugee tension and heightened terrorism fears, would have weighed on sentiment.

Still, when everything is said and done, the euro has been confined to a half-cent range (~$1.0860-$1.0905). It shows no propensity to break out of the $1.08-$1.10 trading range that has largely confined the action since the early December ECB meeting. Given the appreciation of the euro on trade-weighted terms, the drop in oil prices and the increase in real rates, the risk is that Draghi's comment at the press conference on Thursday will spur euro selling. He will likely argue that door is open for additional measures should they be needed (and we think they will nearer midyear).

The dollar is poking through the JPY118.00 level in late-morning activity in Europe. The rise in US Treasury yields and gains in equity markets are the main sources of pressure. In addition, the local press has played up the risks that the BOJ eases policy further as early as the end of the month. Last week's highs in the JPY118.25-JPY118.40 is the next immediate obstacle.

He has been covering the global capital markets in one fashion or another for more than 30 years, working at economic consulting firms and global investment banks. After 14 years as the global head of currency strategy for Brown Brothers Harriman, Chandler joined Bannockburn Global Forex, as a managing partner and chief markets strategist as of October 1, 2018.

Tags: China Retail Sales