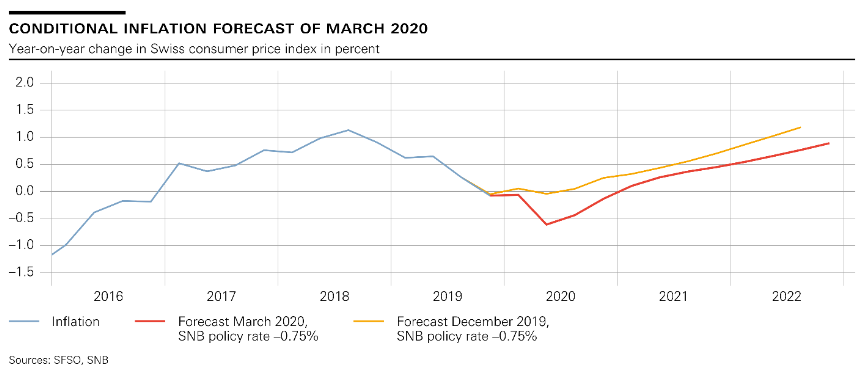

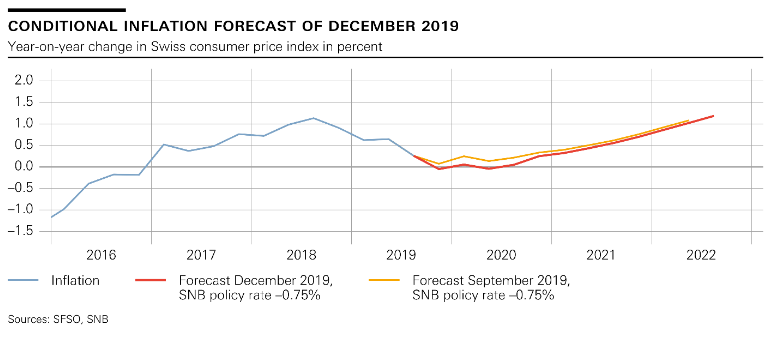

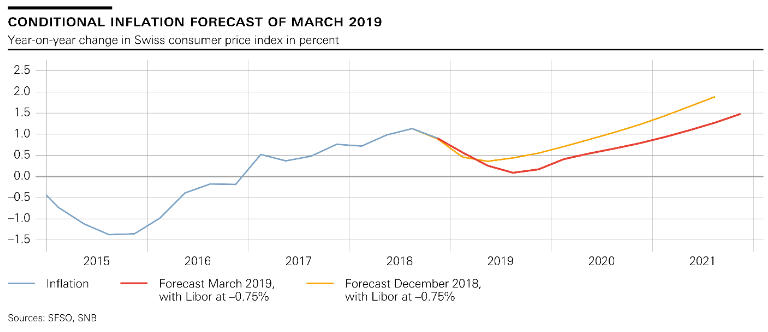

Swiss National Bank leaves expansionary monetary policy unchangedThe Swiss National Bank (SNB) is maintaining its expansionary monetary policy, with the aim of stabilising price developments and supporting economic activity. Interest on sight deposits at the SNB is to remain at –0.75% and the target range for the three-month Libor is unchanged at between –1.25% and –0.25%. The SNB will remain active in the foreign exchange market as necessary, while taking the overall currency situation into consideration. Since the last monetary policy assessment in December, the Swiss franc has appreciated slightly overall on the back of the weaker US dollar. The Swiss franc remains highly valued. The situation in the foreign exchange market is still fragile and monetary conditions may change rapidly. The negative interest rate and the SNB’s willingness to intervene in the foreign exchange market as necessary therefore remain essential. This keeps the attractiveness of Swiss franc investments low and eases pressure on the currency. The SNB’s conditional inflation forecast has shifted slightly downwards as a result of the somewhat stronger Swiss franc. The forecast for the current year has decreased marginally to 0.6%, from 0.7% in the previous quarter. For 2019, the SNB now expects inflation of 0.9%, compared to 1.1% last quarter. For 2020, it anticipates an inflation rate of 1.9%. The conditional inflation forecast is based on the assumption that the three-month Libor remains at –0.75% over the entire forecast horizon. The international economic environment is currently favourable. In the fourth quarter of 2017, the global economy continued to exhibit solid, broad-based growth. International trade remained dynamic. Employment registered a further increase in the advanced economies, which is also bolstering domestic demand. |

SNB Switzerland Conditional Inflation Forecast(see more posts on Switzerland inflation, ) Conditional Inflation Forecast - Click to enlarge |

| The SNB expects global economic growth to remain above potential in the coming quarters. Given the robust economic situation, the US Federal Reserve plans to continue its gradual normalisation of monetary policy. In the euro area and Japan, by contrast, monetary policy is likely to remain highly expansionary.

In Switzerland, GDP grew in the fourth quarter at an annualised 2.4%. This growth was again primarily driven by manufacturing, but most other industries also made a positive contribution. In the wake of this development, capacity utilisation in the economy as a whole improved further. The unemployment rate declined again slightly through to February. The SNB continues to expect GDP growth of around 2% for 2018 and a further gradual decrease in unemployment. Imbalances on the mortgage and real estate markets persist. While growth in mortgage lending remained relatively low in 2017, prices for single-family houses and owner-occupied apartments began to rise more rapidly again. Residential investment property prices also rose, albeit at a somewhat slower pace. Owing to the strong growth in recent years, this segment in particular is subject to the risk of a price correction over the medium term. The SNB will continue to monitor developments on the mortgage and real estate markets closely, and will regularly reassess the need for an adjustment of the countercyclical capital buffer. |

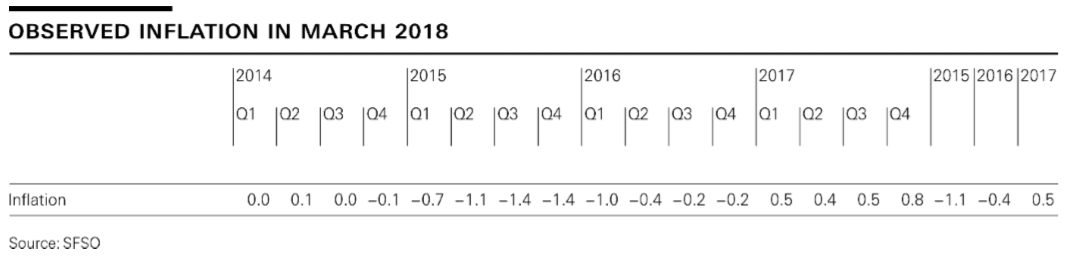

Switzerland Inflation and Inflation Forecast(see more posts on Switzerland inflation, ) Observed/Conditional Inflation - Click to enlarge |

Tags: newslettersent,SNB monetary policy,Switzerland inflation