Read More »

On Swiss National Bank

On Swiss National Bank  Main SNB Background Info

Main SNB Background Info

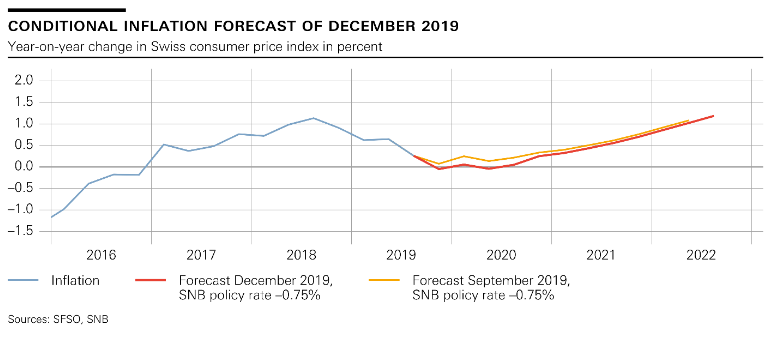

Monetary policy assessment of 12 December 2019

Monetary policy assessment of 12 December 201912 Dec 2019

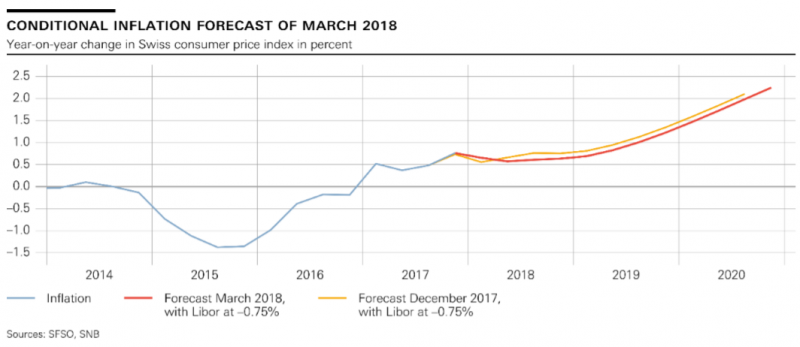

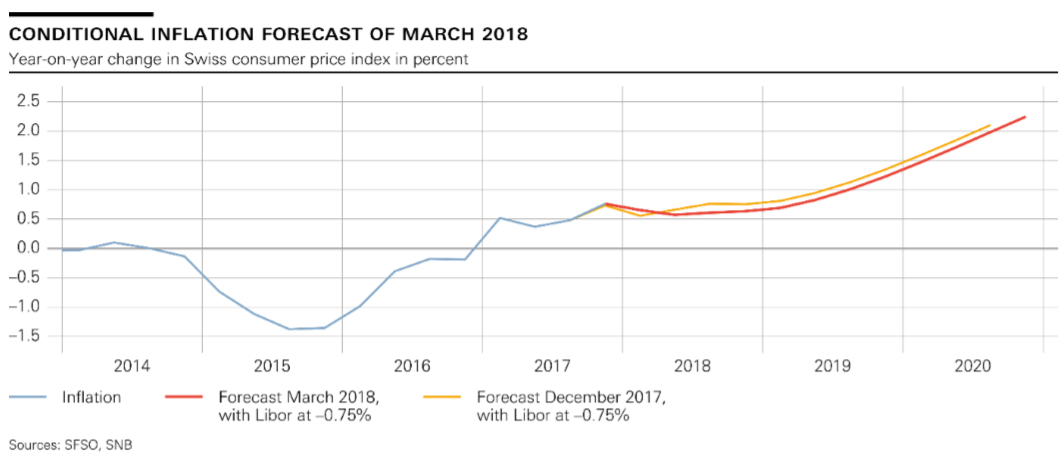

SNB Monetary policy assessment of 15 March 2018

SNB Monetary policy assessment of 15 March 201815 Mar 2018

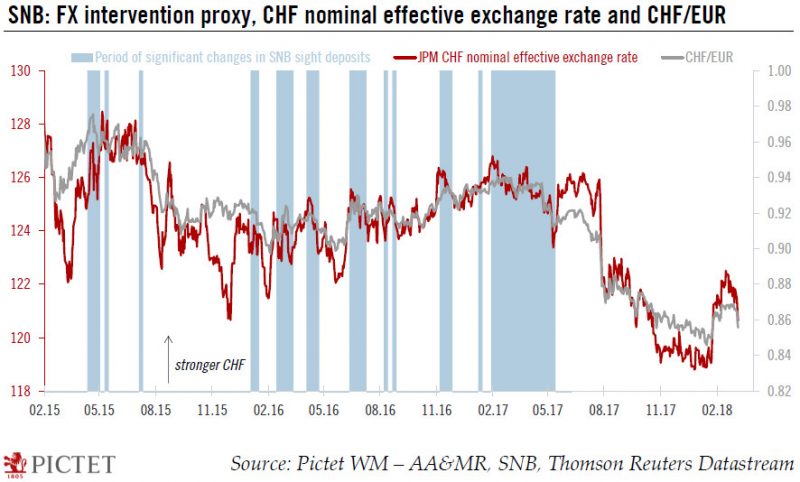

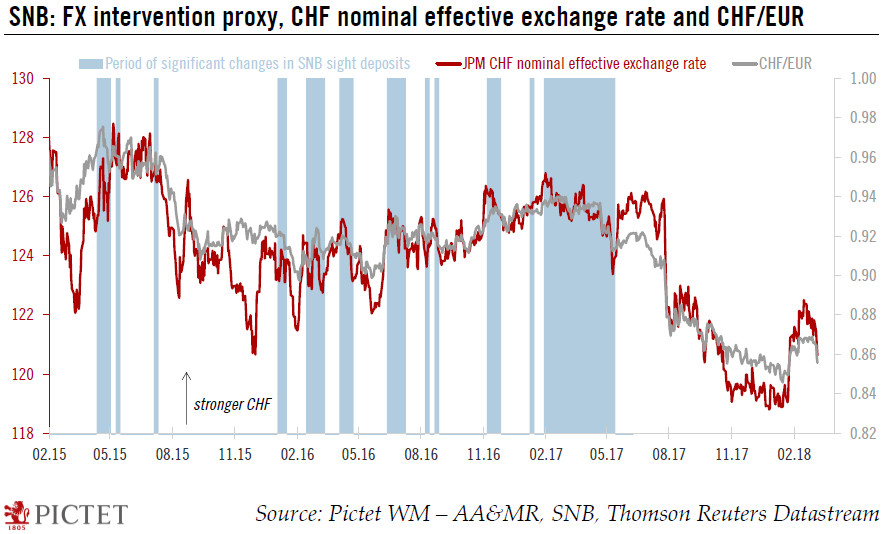

Europe chart of the week – SNB FX intervention

Europe chart of the week – SNB FX intervention10 Mar 2018

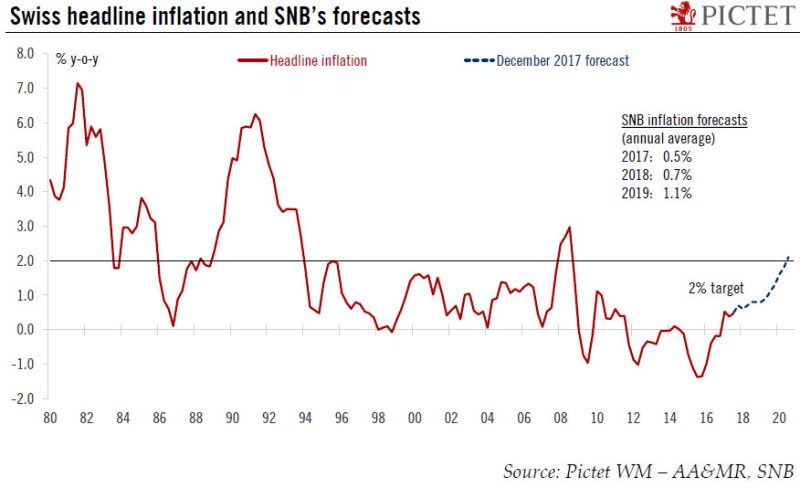

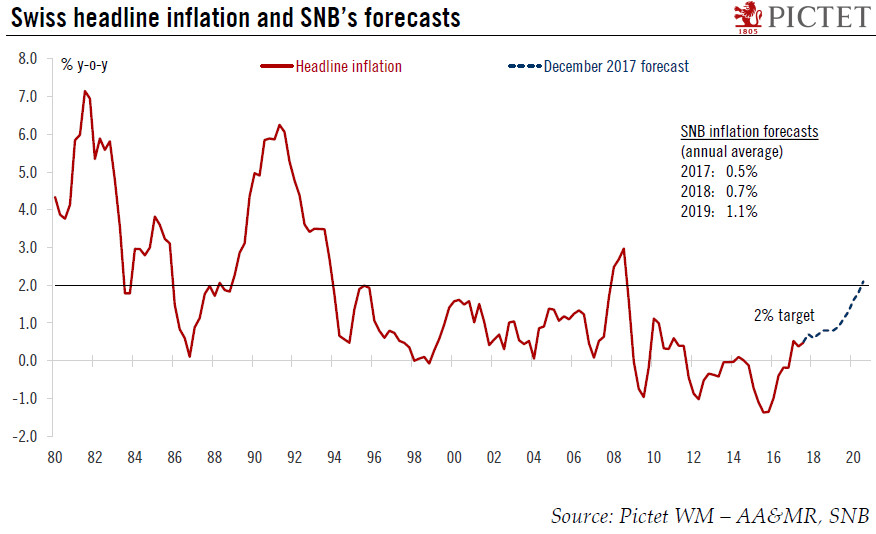

Increasingly optimistic on Swiss outlook

Increasingly optimistic on Swiss outlook22 Dec 2017

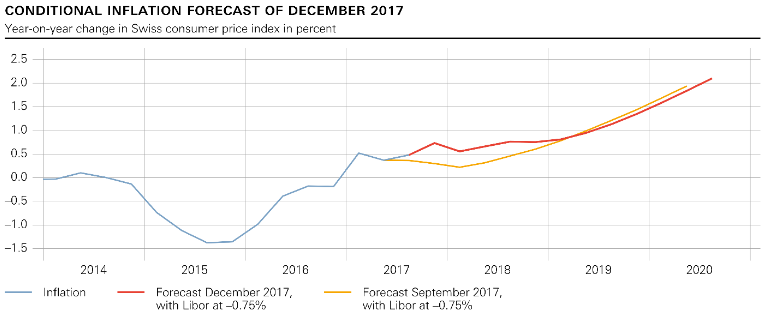

SNB Monetary policy assessment of 14 December 201714 Dec 2017

13 Sep 2016