In Part One, we explored how leverage and derivatives turned subprime mortgages into a crisis that nearly brought down the global financial system. With a better understanding of the derivatives and leverage that led to the Global Financial Crisis (GFC), we now explore private credit, a small “niche” financial sector, such as subprime mortgages, which some are calling the next match to light a financial bonfire.

Private Credit Loan Growth

The graph below, courtesy of Preqin and the Daily Shot, shows the steady growth of private credit funds since the GFC. The “Dry Powder” category represents committed capital for investment that has not yet been deployed. For what it is worth, that amount is almost identical to the amount of subprime mortgages at their peak. The total global private credit market, including all other lenders, is estimated at around $3.4 trillion.

After the GFC, regulators forced banks to hold more capital and to retreat from riskier lending. As a result, an alternative credit ecosystem grew to replace banks. Private credit funds, business development companies (BDCs), and specialty finance vehicles have filled the gap.

Unlike the various subprime mortgage securities and derivatives, which were largely owned by institutional investors, retail investors have gotten involved in private credit funds. They were tempted with high yields and monthly or quarterly redemption windows.

The private credit tremors started with the bankruptcies in the auto sector — Tricolor and First Brands. Then Market Financial Solutions faced allegations of "serious irregularities," including concerns that it was double-pledging collateral. As broad credit and fraud concerns rose, the private credit fund, Blue Owl, was forced to gate withdrawals from a retail credit vehicle in early 2026. Ares Strategic Income Fund, with $10.7 billion under management, followed, capping redemptions at 5% versus withdrawal requests of nearly 12%. Apollo marked down assets in one of its BDCs and cut the payout. The list goes on, and as it grows, so does the level of fear.

Private Credits Structural Flaw

While defaults and collateral pledging irregularities are problematic, the headlines about gated funds seem to be the primary drivers of negative sentiment. Currently, losses and defaults in the underlying loans are not a big problem. Instead, many inexperienced retail investors own the funds and want their money back, but the funds are not in a position to return it promptly.

The fundamental problem in private credit is a mismatch. Private credit funds lend money over four- to five-year periods. But to attract investors, many funds offer investors quarterly or even monthly redemption windows.

When redemptions spike, a fund cannot get its money back from those it lent to. Its only options are to limit investor redemptions or sell the loans in the market, which has few ready buyers for such illiquid paper. Such forced selling drives prices down, which weighs on the fund’s net asset value (NAV) and triggers further redemption requests. Accordingly, more funds are forced to limit withdrawals, leading to worsening sentiment. And in circular fashion, the problem worsens.

Compounding the problem is that over 25% of private credit loans are to software companies. As the software sector gets assaulted by damaging AI narratives, its credit investors get nervous and demand their money back.

This Isn’t Subprime

Private credit today is a fancy term for direct lending. The fund makes a loan, holds it on its balance sheet, and bears the loss if it defaults. There are no synthetic CDOs replicating that exposure, like with subprime mortgages. There are no insurance companies writing unhedged protection on private credit indices. Yes, many funds use leverage, as do some investors, but the degree of leverage pales in comparison to what occurred in the mid-2000s. Moreover, the derivative structure that turned the manageable subprime-loss problem into a global catastrophe does not exist in private credit in a comparable form.

The risk today is macroeconomic in nature. If the negative sentiment surrounding private credit alters the investing and lending behavior of investors, banks, and other direct lenders, liquidity will be squeezed, and credit creation will weaken. Less lending and at higher interest rates can manifest as economic weakness, as it flows downstream to consumers and small and mid-sized businesses. To wit, Fed President Stephen Miran recently stated:

I am concerned by the private credit impact on broad credit growth.

Credit Stress Travels: From Private Credit to Banks

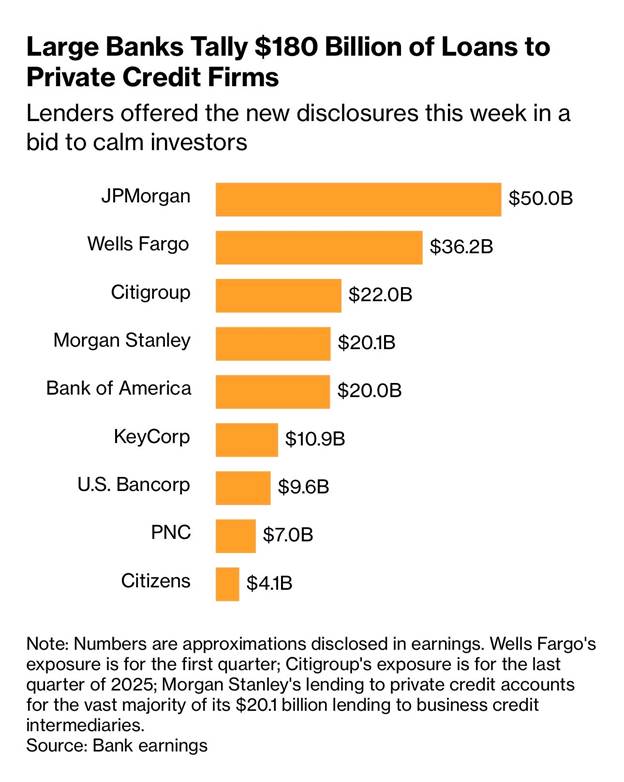

While post-GFC, banks may have retreated from direct and riskier lending, they remain involved. It is estimated that US banks have direct exposure to private credit funds of $300 billion through the leverage they provide. As shown below, courtesy of Bank Earnings, the largest banks account for over half of that exposure.

As we share below, bank loans to non-depository financial institutions are approaching $2 trillion and have grown at a quickened pace since 2025. To wit, JPMorgan and Fifth Third Bank disclosed losses tied to the aforementioned auto-sector bankruptcies. Private credit fund struggles don’t accrue solely to investors; they also appear on the balance sheets of the banks that provided the leverage to build them. However, the exposure to private credit pales in comparison to subprime mortgages.

Summary

This is not a redux of the GFC! The subprime crisis was much more deeply embedded in the core banking system. Private credit, for all its growth, remains a $3-4 trillion market within a global financial system measured in the hundreds of trillions. Default rates, while rising, remain low and manageable. Gated funds are a feature of the investment and not a cause for panic.

Due to faulty marketing targeting inexperienced retail investors, private credit problems are making headlines. With the headlines, broader financial system confidence and sentiment are in play. If private credit concerns spread, liquidity in the traditional and shadow banking systems could tighten, leading to reduced investment, tougher credit conditions, and resulting in subdued economic activity. But a 2008 repeat, shaking the financial system to its core, is highly unlikely.

The post GFC 2.0 Or False Alarm Part 2 appeared first on RIA.

Full story here Are you the author?You Might Also Like

The Berkshire War Chest: A Crisis Hedge?

The Berkshire War Chest: A Crisis Hedge?

2026-04-08

Berkshire Hathaway now sits on $373 billion in Cash. They have enough to buy 480 companies in the S&P 500. For context, this is the largest cash stockpile since 2008. At that time, Berkshire used its cash not to buy stocks on the open market but largely to offer companies private deals that ordinary investors …

Market Sector Review: Extreme Market Bifurcation

Market Sector Review: Extreme Market Bifurcation

2026-02-16

Since the beginning of the year, we have discussed the “reflation trade” and its impact on specific market sectors. This past weekend’s newsletter also showed some of these more extreme returns in various market sectors since the beginning of the year. To wit: “Despite what seemed like a rough week in the market, it really wasn’t as …

Sanae Takaichi And The Yen Carry Trade

Sanae Takaichi And The Yen Carry Trade

2026-02-10

In a blog last week titled Japan Is Normalizing: Risks To The Yen Carry Trade, we discussed Japan’s path to economic normalization and how it might affect a great source of global liquidity, the yen carry trade. A week after publishing the article, Japan had a stunning election. As a result, its new Prime Minister, …

2025-11-05

“Nvidia takes a $1 billion stake in Nokia” reads a recent CNBC headline. As part of the agreement, Nokia commits to purchasing Nvidia’s AI chips and computer platforms. Additionally, the companies will collaborate to develop 6G cellular technology. Deals like this are becoming more common in the AI industry. Some view Nvidia’s recent investment in …

Amazon And OpenAI: Yet Another Massive Investment In AI

Amazon And OpenAI: Yet Another Massive Investment In AI

2025-11-04

Yesterday morning, OpenAI announced a massive $38 billion strategic partnership with Amazon Web Services (AWS). This deal highlights OpenAI’s diversification strategy amid explosive growth and capacity demands for training advanced models like ChatGPT. Before the deal, OpenAI relied 100% on Microsoft for its cloud infrastructure. In addition to diversifying its cloud servers, the deal may …

Hindenburg Strikes: Omen Or False Alarm?

Hindenburg Strikes: Omen Or False Alarm?

2025-11-03

Last Wednesday, for the first time since November 2021, a Hindenburg Omen hit. This gauge is triggered when an upward trend is met with a growing number of stocks hitting both new 52-week highs and lows. Such indicates bad breadth, weakening momentum, and indecision. If all five conditions listed below are met, the indicator gives …

Liquidity Concerns Put An End To QT

Liquidity Concerns Put An End To QT

2025-10-30

Two weeks ago, Jerome Powell stated, “We may be approaching the end of our balance sheet contraction in the coming months.” In simple terms, as we wrote HERE, he is prepping the market for a quicker end to QT than was previously expected. While Powell was cryptic about why, the answer is obvious: liquidity concerns. …

Tags: Featured,newsletter