Lance Roberts

My articles My offerMy siteAbout meMy videosMy books

Follow on:TwitterSeeking AlphaFacebookAmazon

The fiat currency collapse narrative is one of the most emotionally satisfying arguments in all of financial punditry. It feels intellectually rigorous, draws on genuine history, and speaks to deep and legitimate anxieties about government overreach, monetary recklessness, and the long-term consequences of unlimited debt creation. Monetary analyst John Rubino makes the case as well as anyone, warning that the world's major fiat currencies are entering a "death spiral" driven by insurmountable debt obligations.

But compelling is not the same as correct.

When you stress-test the fiat death spiral thesis against actual evidence, three foundational problems emerge that don't just weaken the argument; they systematically dismantle it. Let's work through each one.

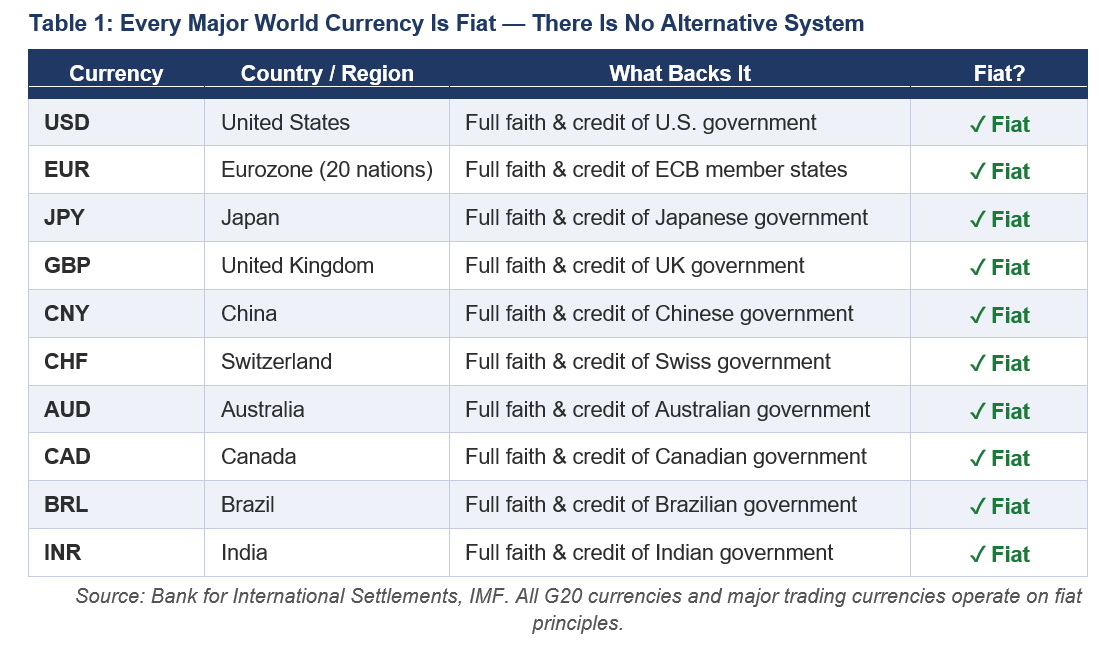

The Foundational Problem: Every Currency in the World Is Already Fiat

Before we can evaluate the collapse thesis, we need to confront its most fundamental flaw: there is no alternative monetary system waiting in the wings. Every currency on earth — the dollar, the euro, the yen, the yuan, the pound, the franc — is a fiat currency. Every one of them.

The entire global trade and financial settlement infrastructure — SWIFT, correspondent banking, sovereign bond markets, FX reserves, derivatives markets — is built on the fiat architecture. Not partially. Entirely. The death spiral argument implicitly assumes there is something to collapse toward. There isn't. Fiat is not a vulnerable feature of the system. It is the system.

"When Rubino warns that fiat currencies are dying, the logical follow-up question — one that almost never gets answered — is: dying relative to what, exactly?"

Gold? We'll address that shortly. Bitcoin? Too volatile and illiquid at scale to anchor global trade. A return to the gold standard? No major economy has shown the slightest political will to impose those rigid monetary constraints to any significant degree. (China has been making some small strides to back Remibi with gold for limited trade, but nothing at significant scale.) The fiat death-spiral argument collapses under its own premise because it has no exit ramp.

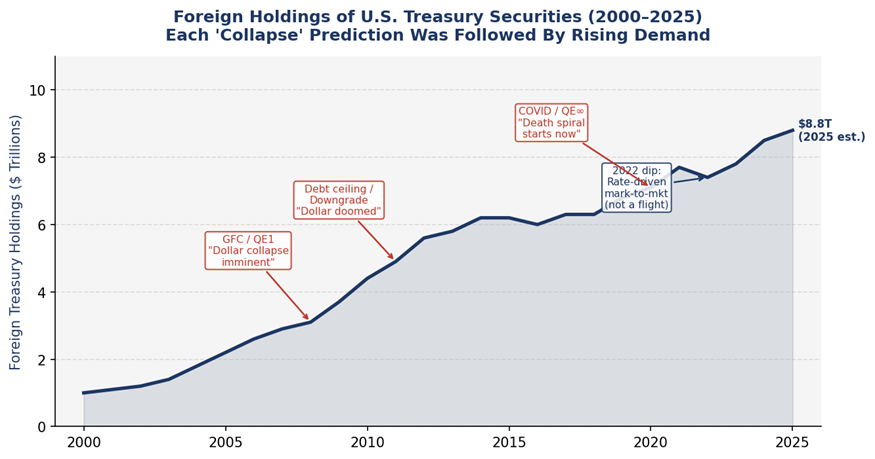

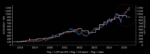

The Market Verdict: Record Demand for U.S. Debt Tells a Different Story

If Rubino was correct, and a fiat currency death spiral were actually underway, and if the markets genuinely believed that dollar-denominated obligations were approaching a confidence crisis, you would expect to see one very specific and unmistakable signal: collapsing demand for U.S. Treasury debt. The opposite is happening.

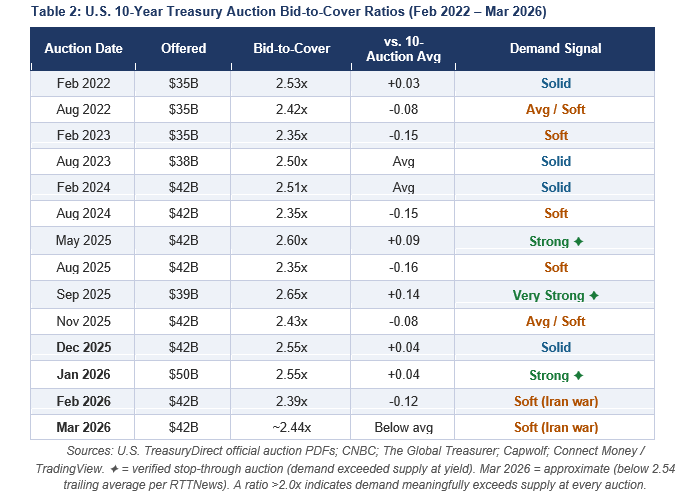

Demand for U.S. Treasuries remains robust at record issuance levels. Foreign central banks, sovereign wealth funds, and institutional investors continue to absorb hundreds of billions in new supply. Treasury auctions routinely clear at bid-to-cover ratios signaling a healthy appetite, consistently above 2.4x, even as issuance volumes have grown materially.

This is the most direct empirical rebuttal to the fiat death spiral thesis, and it matters precisely because it is observable in real time. You don't need a macro model or a historical analogy; you just need to ask: Is global capital fleeing the dollar?

"Markets are often wrong. But they are a better real-time signal than a pundit's priors. And right now, the global capital markets are voting with trillions — in favor of dollar-denominated assets."

Even the softest recent auctions in February and March 2026, which occurred amid a shooting war in the Middle East and elevated oil price volatility, cleared without disruption. Compare this to Argentina in 2001 or Turkey in 2018. In both periods, there was a genuine currency crisis, with unambiguous warning signs: collapsing bond demand, surging yields, capital flight, and currency devaluation. None of those dynamics is present in the U.S. dollar today, and the death spiral narrative asks us to ignore the market and trust the thesis.

That is not an analytical discipline. It is motivated reasoning.

The Gold Contradiction: A Dollar-Denominated Asset Can't Replace the Dollar

Rubino's fiat death spiral argument almost always comes packaged with a companion narrative: gold is surging because smart money is fleeing fiat currency. On the surface, this appears to be supporting evidence. Look deeper, and it reveals a deep internal contradiction.

Gold's price is quoted in dollars. When someone says gold has surged to record highs, they are measuring that appreciation in the very currency they claim is dying. If the dollar were genuinely collapsing toward zero, a rising gold price measured in dollars would be analytically meaningless, like measuring the shrinking size of a room with a rubber ruler. However, since gold is traded in dollars and serves as a global store of value, the inverse correlation between gold and the dollar is logical.

"Gold is not a monetary successor to the dollar. It is a dollar-denominated store of value — a sentiment barometer and an inflation hedge. Those are useful things. But they are not the same as a functioning monetary system."

This is a point that Rubino and many others miss. Gold has no payment rails. It cannot settle international trade, nor fund a government payroll. But there is an even more crucial point to why gold is not a viable substitute for "money." The total above-ground gold stock is approximately $14–15 trillion at current prices, and the total size of global financial assets exceeds $250 trillion. You cannot rotate even a fraction of institutional capital into gold without pushing the price to levels that would themselves destabilize the thesis. The math simply does not work at scale.

Lastly, Central bank gold purchases, often cited as confirmation of the death spiral narrative, are better understood as a form of reserve diversification. Every central bank buying gold is still operating within, reporting in, and settling obligations through the fiat system. They are buying gold with dollars and euros, not abandoning them.

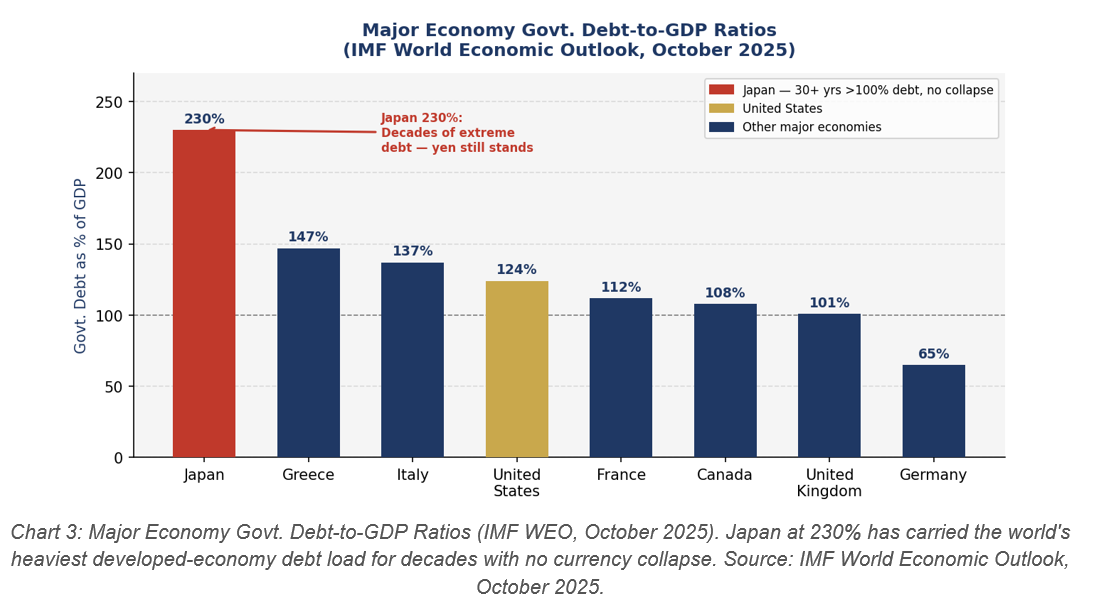

Japan: The 30-Year Natural Experiment That Falsifies the Model

But what about the debt?

If excessive debt relative to GDP were sufficient to trigger a fiat death spiral, Japan should have ceased to function as an economy around 2005. Japan's debt-to-GDP ratio has exceeded 200% for well over a decade — it now sits north of 260%. The Bank of Japan owns a staggering share of its own government bond market. Japanese interest rates were held near zero (or below) for decades. By every metric the death spiral argument invokes, Japan should be Exhibit A in the global currency collapse museum. Instead, the yen remains one of the most traded currencies in the world. Japan's government continues to function, the bond markets haven't revolted, and hyperinflation never materialized

Any serious analytical framework for fiat collapse has to explain Japan first. Most don't, because Japan is a 30-year natural experiment that directly falsifies the simplistic "debt = currency collapse" equation. The mechanism that death spiral theorists rely on simply does not function as they assume it does in a modern monetary context.

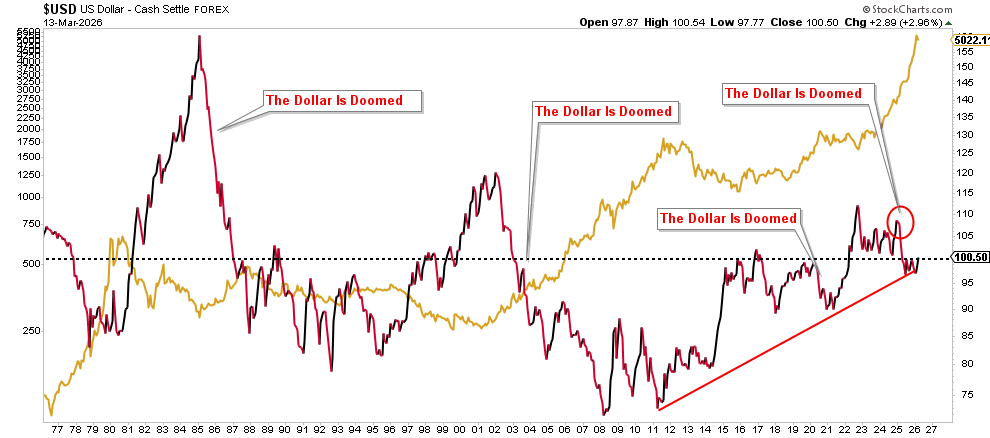

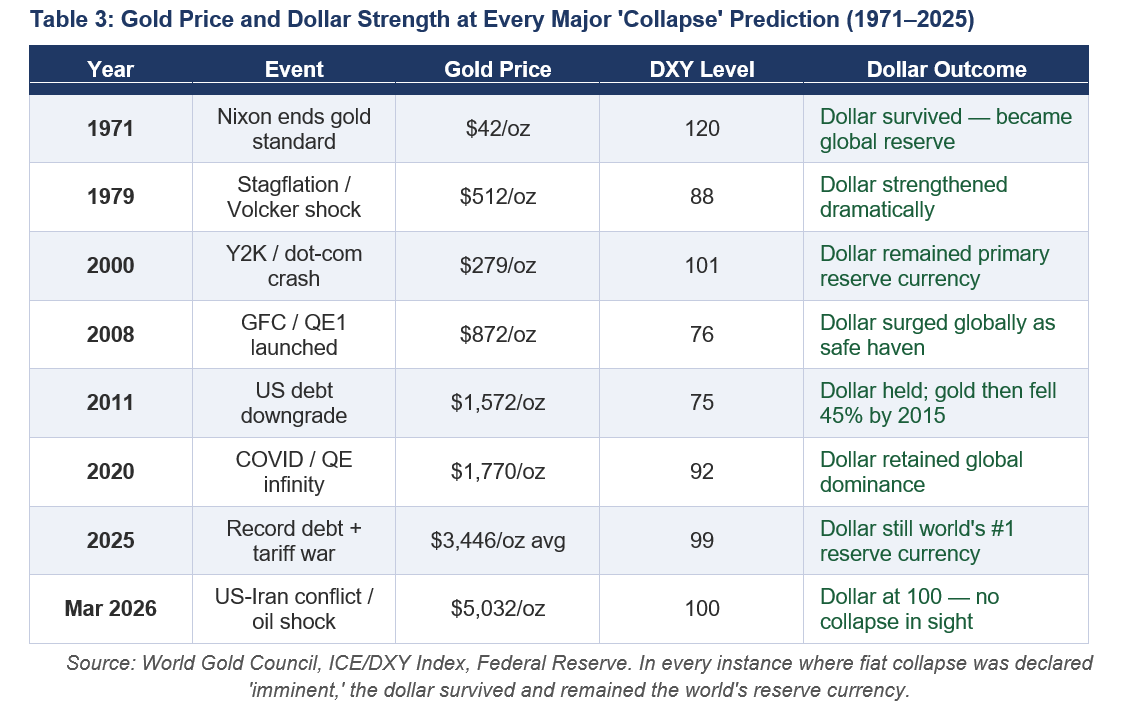

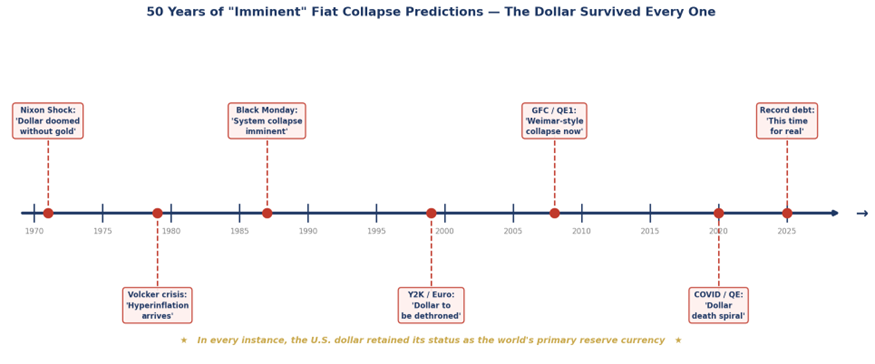

The Prediction Has Been Wrong for Fifty Years

Here is the most damning critique of Rubino's fiat death spiral thesis, and it is one that rarely receives sufficient weight: this argument has been made continuously, with great conviction, since at least the Nixon shock of 1971, when the U.S. severed the dollar's last link to gold.

For over half a century, hard money analysts have issued confident warnings that a dollar collapse was imminent. The 1970s inflation spike seemed to vindicate them — and then Paul Volcker broke inflation's back. In the 1980s, Reagan's deficits were going to destroy the dollar. In the 2000s, the housing bubble and twin deficits. After 2008, the Fed's balance sheet expansion to $4 trillion was going to trigger Weimar-style hyperinflation. After COVID, the expansion to $9 trillion surely would.

At some point, a forecast that has been confidently wrong for five consecutive decades deserves methodological scrutiny, not renewed repetition. The analysts who make this argument, like Rubino, aren't bad people or incompetent thinkers; many are quite sharp. But they are systematically underweighting the adaptive capacity of modern monetary institutions and the structural demand for dollar-denominated assets.

The fiat collapse narrative persists not because the evidence is overwhelming, but because it is emotionally resonant, ideologically satisfying, and, crucially, unfalsifiable in the short run. Every year that the collapse fails to materialize becomes, in the telling, simply more fuel for the fire.

That kind of "heads-I-win, tails-you-haven't-waited-long-enough" logic is not analysis. It is a belief system dressed in a spreadsheet.

Conclusion

John Rubino is a thoughtful analyst raising legitimate concerns about fiscal sustainability. Those concerns deserve serious engagement. But the death spiral framing overstates the case, leading investors to draw the wrong conclusions and make poor portfolio decisions.

The fiat currency system is not collapsing. It is the only monetary system in existence. Global capital continues to flow into dollar-denominated assets at record levels. Gold, whatever its merits as an inflation hedge, is itself a creature of the dollar system. It is not its replacement. And the list of countries that have carried extreme debt loads without triggering currency collapse is long, led most conspicuously by Japan.

"Unsustainable fiscal trajectory requiring painful adjustment" is a real risk worth positioning for.

"Fiat death spiral" is a narrative.

Serious investors know the difference and build their portfolios accordingly.

Sources & References

- U.S. Treasury Department — TreasuryDirect.gov, auction results, and TIC foreign holdings data (2025–2026)

- International Monetary Fund — World Economic Outlook, sovereign debt-to-GDP statistics (October 2025)

- Bank for International Settlements — Triennial Central Bank Survey, FX market data (2024)

- World Gold Council — Central bank gold reserves and demand reports (2025)

- Bank of Japan — Balance sheet and JGB ownership data (2025)

- Federal Reserve — H.4.1 statistical release, balance sheet data (2026)

- ICE Benchmark Administration — U.S. Dollar Index (DXY) historical data

- Reinhart, C. & Rogoff, K. — This Time Is Different: Eight Centuries of Financial Folly (Princeton University Press)

- Rubino, J. — Dollar Collapse thesis, interview transcript (2026)

The post Rubino: Fiat Currencies Are In A Death Spiral appeared first on RIA.

Full story here Are you the author?You Might Also Like

The Dollar’s Plumbing: Conspiracy Vs. Data

The Dollar’s Plumbing: Conspiracy Vs. Data

2026-03-20

Every few months, a headline appears declaring that the U.S. dollar’s reign as the world’s reserve currency is over. China is dumping Treasuries. Central banks are hoarding gold. The BRICS are building a new monetary order. The sanctions that froze $300 billion of Russia’s reserves in 2022 proved, the argument goes, that dollar-denominated assets are …

Economic Sentiment Belies Strong Economic Estimates

Economic Sentiment Belies Strong Economic Estimates

2026-02-27

Economic growth metrics for the United States have recently shown surprising resilience; however, consumers’ economic sentiment has not. According to the Bureau of Economic Analysis’s advance estimate, real Gross Domestic Product expanded at an annualized rate of just 1.4%, well below expectations and a steep drop from the 4.4% pace in the third quarter. However, …

Mainstream Expectations: Hope Vs. Potential Risk

Mainstream Expectations: Hope Vs. Potential Risk

2026-01-30

Mainstream expectations, those from Wall Street, economists, and corporate strategists, have congealed around a bullish economic outlook for 2026. Most forecasts project stronger economic growth, with contained inflation, and continued investment in technology and capital expenditure. As such, many institutional investors interpret this as a year of opportunity for markets and corporate earnings.That was a …

Does AI Capex Spending Lead To Positive Outcomes?

Does AI Capex Spending Lead To Positive Outcomes?

2025-12-12

As someone who views corporate finance through a pragmatic lens, I’ve been closely watching the current surge in capital expenditures (capex) tied to artificial intelligence (AI). The question I’m addressing here is this: when a company spends massive amounts of free cash flow and takes on increasing debt, in this case for AI CapEx, does …

Tags: Economics,Featured,newsletter