Lance Roberts

My articles My offerMy siteAbout meMy videosMy books

Follow on:TwitterSeeking AlphaFacebookAmazon

Previously, we discussed Modern Monetary Theory (MMT) and its one limitation of inflation. However, as is always the case when “theories” collide with “reality,” the tenants of the theory are quickly discarded.

There is no doubt that since 2020 both Republicans and Democrats alike have shunned fiscal responsibility for the short-term gratification of MMT. Ms. Kelton tweeted such earlier this year.

The writing is hilariously on the wall here, but people want to pretend that a bipartisan, multi-trillion dollar climate-infrastructure package can and must be “paid for” with new tax revenue. Wake me when reality sets in.

— Stephanie Kelton (@StephanieKelton) March 15, 2021

From the $2.2 trillion CARES Act to the $900 billion HERO Act, to President Biden’s $1.9 trillion American Rescue Plan, the government has plunged into MMT with both feet.

If you are unfamiliar with MMT, Kelton describes it as a macroeconomic school of thought or paradigm that explains how a sovereign country that controls its currency behaves. To wit:

“MMT starts with a simple observation, and that is that the US dollar is a simple public monopoly. In other words, the United States currency comes from the United States government; it can’t come from anywhere else. So, what that means is that the federal government is nothing like a household.

For households or private businesses to spend they’ve got to come up with the money, right? And the federal government can never run out of money. It cannot face a solvency problem with bills coming due that it can’t afford to pay. So it never has to worry about finding the money to be able to spend.”

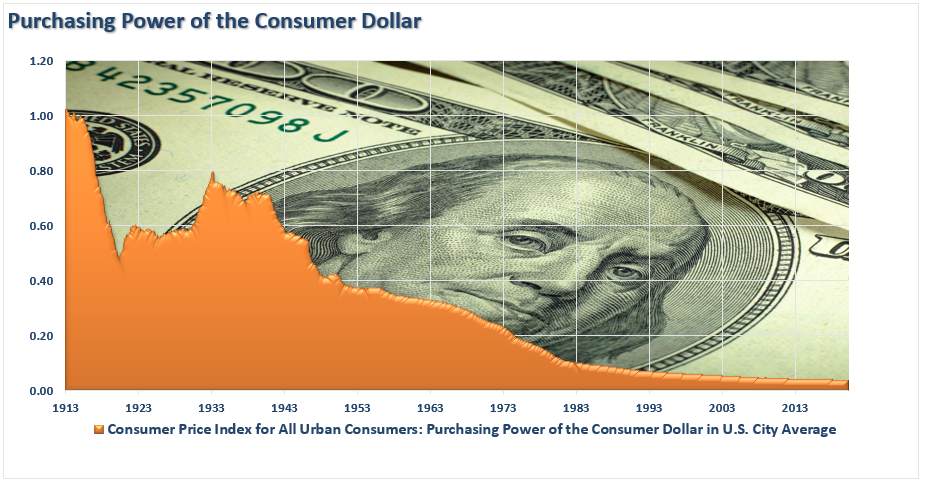

There is nothing untrue about that statement. However, while the Government can indeed “print money to meet all obligations,” it does NOT mean there are no consequences. The chart below really tells you all you need to know.

Always One Part Of The Theory

Throughout history, the purveyors of fiscal and monetary policies always use the one part of the theory that suits them. The spending part. Thus, beginning in the early ’80s, politicians and economists latched onto “Keynesian” economic theory. Why? Because it paved the way to engage into historic levels of deficit spending.

According to Keynes, some microeconomic-level actions, if taken collectively, can lead to inefficient aggregate macroeconomic outcomes. Such leads the economy to operate below its potential output and growth rate (i.e., a recession). As Keynes noted:

“A general glut occurs when aggregate demand for goods is insufficient. Such leads to an economic downturn resulting in losses of potential output. Such creates unnecessarily high unemployment resulting from the producers’ defensive (or reactive) decisions.”

When there is a lack of demand from consumers, producers react defensively to reduce output. In such a situation, Keynes’ theory suggests the Government should intervene.

“In such a situation, government could use policies to increase aggregate demand, thus increasing economic activity and reducing unemployment and deflation. Investment by the government injects income, which results in more spending in the general economy, which in turn stimulates more production and investment involving still more income and spending and so forth. The initial stimulation starts a cascade of events, whose total increase in economic activity is a multiple of the original investment.”

What politicians “heard” was the “spend money” part.

The “Inconvenient” Part

However, politicians always ignore the “other part” of the theory, which states that deficit spending should be cut and surpluses rebuilt when economic activity returns.

As shown, that never happened, and for the last 40-years, economic participants have paid the price of slower growth and prosperity.

However, since Keynes’ model seems to have failed to produce the desired result, economists need a new theory to explain why debts and deficits don’t matter.

The Shiney New Toy – MMT

In reality, there is little difference between Keyne’s and MMT. Both promote the use of government debt to boost economic growth during times of economic hardship. The difference is that Keynes stated the deficit should get reversed following the downturn. MMT proposes that governments can deficit spend regardless of the economic state as long as inflation is not present. To wit:

“First advanced by MMT guru Warren Mosler in the 1990s, is quite simple: federal spending gets unconstrained by revenue. Taxes function only to regulate demand and hence inflation; federal borrowing functions only to regulate interest rates. Sovereign government treasuries can create and spend as much money as they like to stimulate growth, especially when the economy is underperforming. If inflation spikes, the government can impose taxes to take money out of the economy.” – Mises Institute

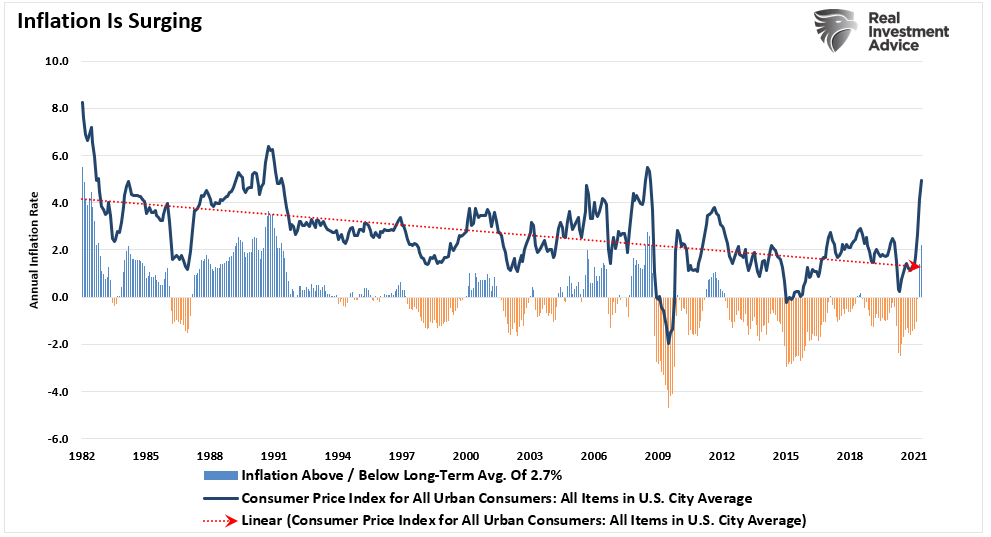

Currently, politicians, Janet Yellen and the Federal Reserve have latched onto this theory as it uncomplicates having to eventually “pay” for the debt. As the first part of the theory goes, “spend as much as you like.” However, once again, they ignore the second part of the theory that limits MMT – inflation.

The flood of money from the Government sent directly to households shifted demand from “services,” which has a very low economic multiplier effect, to the high multiplier of “manufacturing.” That shift, and increase in demand, led to a surge in inflationary pressures.

The Government should be addressing the “limiter” of MMT by raising taxes and cutting spending until inflationary pressures subside.

However, as we suspected, we see no evidence of that currently. Politicians from both sides of the aisle are discussing a $1.2 trillion “infrastructure” plan with no tax increases.

Misdiagnosing The Illness

The desire to use “debt” to cure the “economic illness” seems logical, particularly when viewing it through the MMT lens. However, it is the “cure” that keeps the patient on “life support.”

The policies enacted, be it stimulus, quantitative easing, or bailout programs, fail to create sustainable economic growth because they are debt-based. Using debt to drag forward future consumption only leaves a void that must get filled in the future. Most importantly, the use of debt for non-productive investments, like a stimulus that has a one-time effect, is the debt-service that then absorbs future revenues.

The view that “more money in people’s pockets” will drive up consumer spending, with a sustainable boost to GDP, is wrong. It has not happened in 40-years. What gets missed is that things like temporary tax cuts, or one-time injections, do not create economic growth but merely reschedules it. The average American may fall for a near-term increase in their take-home pay, but any increased consumption today will be matched by a decrease tomorrow when the stimulus ends.

Such is assuming the balance sheet at home is not broken. As we saw during the “Great Depression” period, most economists thought that the simple solution was just more stimulus. Work programs, lower interest rates, and government spending didn’t work to stem the tide of the depression era.

The Ricardian Equivalence

There is also the problem of a shift in psychology as noted by David Rosenberg:

“Another basic law is Ricardian Equivalence, which is all about how economic agents prepare for a future of higher taxation, manifesting in an elevated personal savings rate. Such means that attempts to stimulate an economy by increasing debt-financed government spending will not be effective because investors and consumers understand that the debt will eventually have to get paid for in the form of future taxes.”

The theory argues that people will save based on their expectation of increased future taxes to pay off the debt. Such will offset the increase in aggregate demand from the increased government spending. But, unfortunately, such also implies that Keynesian fiscal policy will not always be effective in providing a lasting boost to economic growth.”

As he notes, individuals base spending upon their future incomes. Thus, if they do not believe that more stimulus is coming, they will save rather than spend, limiting the impact on economic growth.

Furthermore, the issue of higher taxes is settling in with consumers as well. Tax-increase expectations in the January release of the Federal Reserve Bank of New York’s Survey of Consumer Expectations rose for the third month in a row to the highest level in more than seven years. This increase occurred along with a jump in government debt-growth expectations, which are now double normal pre-pandemic levels.

Conclusion

The allure of MMT is strong amid the current economic upheavals. Such is particularly the case since it makes possible every progressive program from unlimited public works, federal jobs, uneconomic green energy schemes, “Medicare for all,” free college, free housing, and a host of others. However, as the Mises Institutes correctly notes:

“The promise of something for nothing will never lose its luster. So MMT should be viewed as a form of political propaganda rather than any real economic or public policy. And like all propaganda, we must fight it with appeals to reality. MMT, where deficits don’t matter, is an unreal place.”

We will likely continue to pay the price of misguided economic policies that only work in the mathematical formulas generated in “Ivory Towers.” Still, in the “real world,” these theories, while well intentioned, always yield a negative result on those it was supposed to help.

The post #MacroView: MMT – When Theories Collide With Reality appeared first on RIA.

Full story here Are you the author?Tags: Economics,Featured,newsletter