| Negative interest rates have long since become a reality. But we are not talking about negative real interest rates. This is the case when the return on an investment is lower than the officially stated inflation rate. In today’s context, negative interest rates are rather negative nominal interest rates; that is, the nominal interest rate is below 0 percent.

This type of negative interest rate already existed once in the 1970s. At that time, Switzerland introduced a “commission” of 2 percent per quarter on bank deposits at Swiss banks. This was intended to inhibit the inflow of new capital into Switzerland. The fixed exchange rates of the Bretton Woods system still prevented the Swiss franc from appreciating at that time, but the money supply expanded sharply from 2.1 percent in 1966 to 10.9 percent in 1968. This increased inflationary pressure on Switzerland. Negative interest rates were imposed in 1972, but they were declared ineffective and abolished after 1978. |

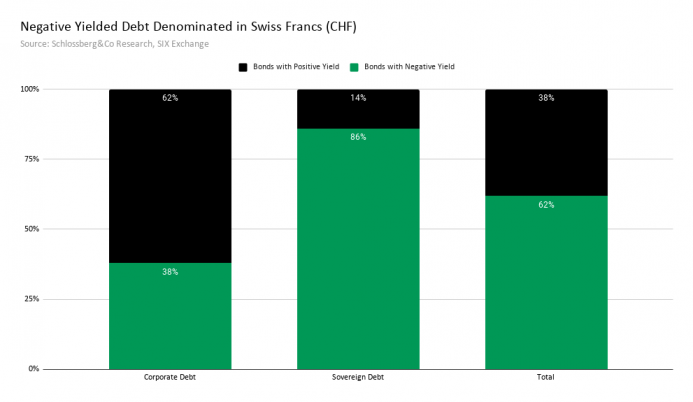

Negative Yielded Debt Denominated in Swiss Francs - Click to enlarge |

| On June 11, 2014, the European Central Bank (ECB) became the first major central bank to set a negative deposit rate of –0.1 percent.

The Swiss National Bank (SNB) went furthest in 2015 and imposed a negative interest rate on deposits of –0.75 percent. At present, the SNB is still at –0.75 percent, while the ECB is close on its heels at –0.5 percent. The Danish central bank has now also caught up with the Swiss national bank, setting its interest rate at –0.75 percent, while Japan’s target rate is –0.1 percent. |

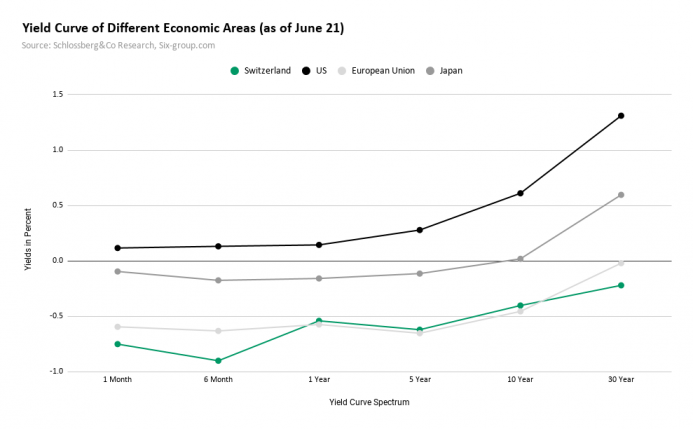

Yield Curve of Different Economic Areas - Click to enlarge |

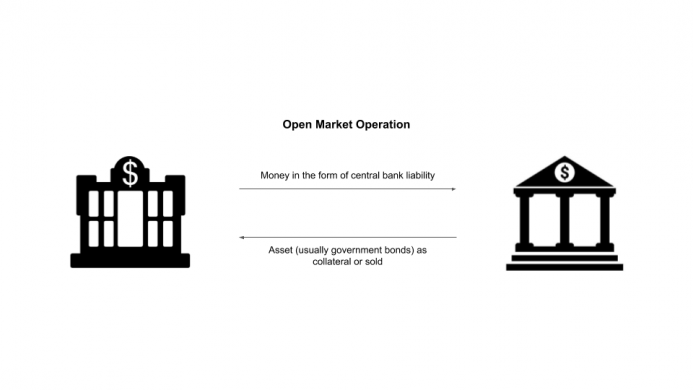

Intervention or Market Forces?The existence of negative interest rates has led to a discussion about their origin. One side sees negative interest rates as an interventionist measure on the part of central banks. By mandate, they artificially lower interest rates. Some opponents even consider this to be an outright manipulation of interest rates. On the other hand, some argue that it is much more likely that the continuous fall in interest rates, even to the point of becoming negative, corresponds to the normal course of economic history. Negative interest rates are no deliberate decision by central banks, but ultimately a natural development. Harvard economist Paul Schmelzing has written of the supersecular decline that is currently unfolding in this context. Some exponents of this side of the spectrum are even absolving the central banks of responsibility for any negative consequences caused by negative interest rates. A popular theory among economists that attributes negative interest rates to a natural development is that of a “savings glut.” Since more and more people in Western countries are saving today, partly due to demographic change, a glut of savings is steadily reducing the marginal utility of additional savings and thus their marginal returns. As a matter of fact, in the Western world we have built up enormous economic capital over the past two centuries. Increasing division of labor and knowledge have played a major role in this. But greater masses of (financial) liquidity are also the deliberate result of central bank action. Through decades of open market policy, they have created ever more liquidity. These open market operations by central banks are ultimately equivalent to the purchase of government bonds. This ongoing demand for government securities from central banks is attracting more and more bond traders, who hope to make a business out of it. After all, they can sell previously purchased bonds to central banks with virtually no risk. If bond prices rise—and this has happened particularly over the past four decades—the interest rates on these bonds fall. |

Open Market Operation - Click to enlarge |

Against Common Sense

But the fact that we have negative interest rates today is difficult to understand from the perspective of human action. Negative interest rates mean that you give up something today and are guaranteed to receive less in return in the future. Intuitively, it should be the other way around: because the present is more certain, it must be more valuable in the face of an uncertain future. So anyone who gives up something today should be rewarded for the risk and uncertainty that this person is willing to venture upon.

A negative interest rate environment, in which the present is worse off economically and materially than the future, appears counterintuitive and can therefore hardly be a natural development. It seems rather likely that negative interest rates should be interpreted as a consequence of interventionist central bank policies.

According to many central bankers, these negative interest rates are an instrument of monetary policy. Representatives at the Swiss National Bank argue that they are intended to counteract the appreciation of the Swiss currency. The ECB argues that commercial banks that have reserve deposits with the central bank should be urged via negative interest on these deposits to pass these reserves on to the economy by giving out loans of all kinds.

Listening to central banks themselves, it pretty much sounds like see negative interest rates as an instrument to steer, guide, and control a currency area. So central bankers themselves implicitly state that negative interest rates are a deliberate tool and not just some unfortunate historical stroke of fate.

Full story here Are you the author?Tags: Featured,newsletter