Jeffrey P. Snider

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking Alpha

| This will serve mostly as an update to what is going on inside the Chinese monetary system. The PBOC’s balance sheet numbers for February 2019 are exactly what we’ve come to expect, ironically confirmed today on the domestic end by the FOMC’s dreaded dovishness. Therefore, rather than rewrite the same commentary for why this continues to happen I’ll just link to prior discussions (here’s another).

|

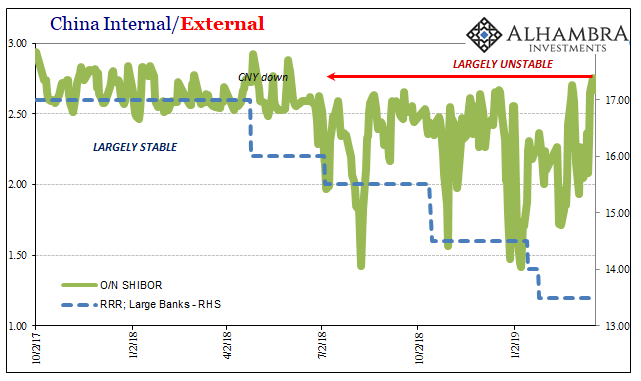

China Internal/External 2017-2019 - Click to enlarge |

| Overnight SHIBOR today was the highest since last May, meaning despite four additional RRR cuts in between they haven’t accomplished much if anything. Rather, RMB money markets (unsecured, pictured below, and secured, not pictured) are more of a mess now than before despite them. RRR adjustments are not stimulus, they are an attempt to fill in a huge hole that’s already been dug. |

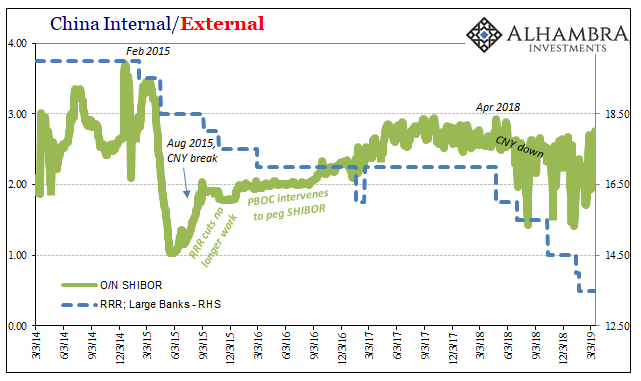

China Internal/External 2014-2019 - Click to enlarge |

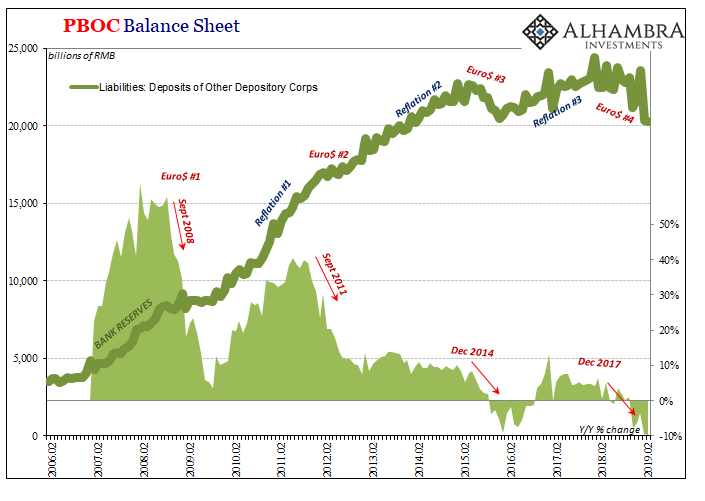

| The reason is simple: an ongoing reduction in the level of bank reserves. The PBOC continues its policy of monetary restriction (not by choice) which for January and February 2019 had meant contractions each month by more than 9% year-over-year. And since that level of decline was consistent for both months it cannot be explained by the Golden Week.

It does, however, begin to explain SHIBOR and repo. |

PBOC Balance Sheet 2006-2019 - Click to enlarge |

| Also on the money side (PBOC liabilities), the level of currency is actually skewed by the holiday. Straight calculation, year-over-year currency issued dropped by more than 4% from February 2018. However, that number means nothing. The pattern here more closely resembles the PBOC’s actions in 2016. |

PBOC Balance Sheet 2007-2019 - Click to enlarge |

| This would suggest a more combined approach to both months in terms of liquidity planning for the holiday. Therefore, we won’t really know the intended non-holiday baseline currency level until the March update next month. I doubt there has been a large shift of intent given how China’s economy continues to perform.

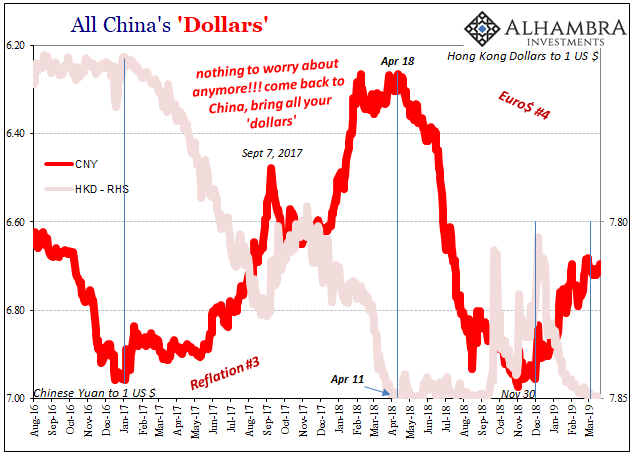

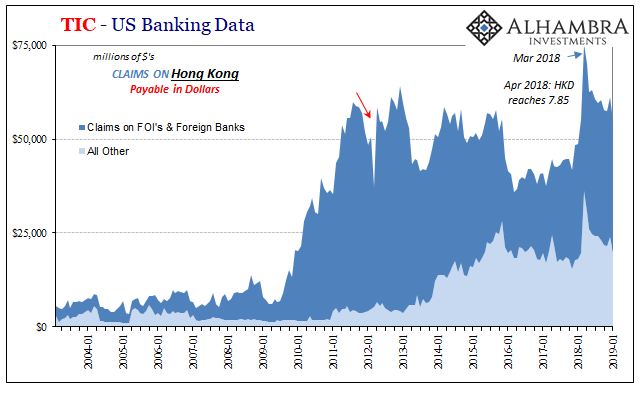

The only wrinkle, and it’s more about this month than last month, is CNY and now HKD right back at the 7.85 (to the dollar) lower bound again. I have to believe that’s why the PBOC continues to allow bank reserves to be scaled back by such huge amounts. The HK eurodollar pipeline is closed once more. I’ll have more to say about this at another time. |

All China's Dollars 2016-2019 - Click to enlarge |

TIC - US Banking Data 2004-2019 - Click to enlarge |

Jeffrey P. Snider is the head of Global Investment Research of Alhambra Investment Partners (AIP). Jeffrey was 12 years at Atlantic Capital Management where he anticipated the financial crisis with critical research. His company is a global investment adviser, hence potential Swiss clients should not hesitate to contact AIP

Tags: $CNY,bank reserves,currencies,Currency,economy,EuroDollar,Federal Reserve/Monetary Policy,Markets,newsletter,PBOC,RMB