Marc Chandler

My articles My offerMy siteAbout meMy videosMy books

Follow on:LinkedINTwitterSeeking AlphaAmazon

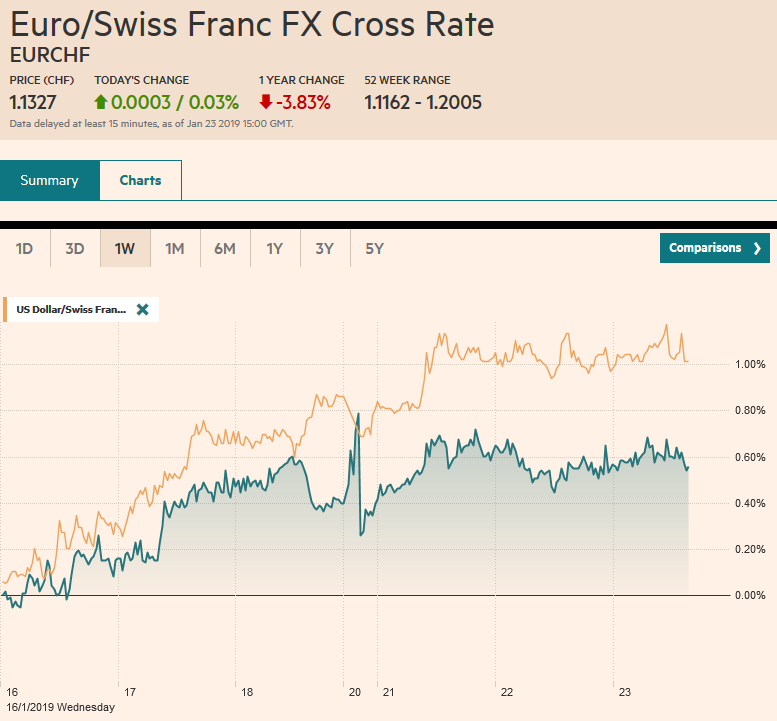

Swiss FrancThe Euro has risen by 0.03% at 1.1327 |

EUR/CHF and USD/CHF, January 23(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Global equities have fared better than the 1.4% slide in the S&P 500 yesterday may have implied. Asian markets were mixed, with China, Korea, Hong Kong, Thailand advancing. The Dow Jones Stoxx 600 from Europe is a little changed after falling for the past two sessions. News after the US close yesterday included better IBM outlook and news of the US Senate vote tomorrow that could mark the beginning of the end of the partial government shutdown is helping US equities stabilize today. Core benchmark bond yields are slightly firmer while the periphery yields are a touch lower. The dollar is little changed against most of the major currencies and is sporting a slightly heavier tone against most of the emerging market currencies. |

FX Performance, January 23 - Click to enlarge |

Asia Pacific

The Bank of Japan pared inflation forecasts for the fourth time at its quarterly outlook report. Core inflation for the current fiscal year was shaved to 0.8% from 0.9%, but more telling was the cut in the next fiscal year’s forecast to 0.9% from 1.4%. This is still above the market (0.7% median in a Reuters survey), and the BOJ hints that additional adjustment may be forthcoming. It noted that is forecasts did not include the cut in mobile phone fees or free school for young children. That latter alone could cut core CPI by 0.3% in FY19 and 0.4% in FY20.

Following news that Japan’s December exports fell 3.8% year-over-year, twice what the market had expected, including a 7% drop in exports to China, the BOJ cut its FY18 GDP forecast to 0.9% from 1.4%. However, it increased FY19 growth to 0.9% from 0.8% and FY20 to 1.0% from 0.8%.

The decline in Japanese exports is a regional development. China, Korea, Thailand, Indonesia, and Singapore also reported declines in December exports. January does not seem to be off to a good start. South Korea report that in the first 20-days in January, its exports were off 14.6% year-over-year and imports were down 9.5%. Of note, its semiconductor exports had fallen almost 29% year-over-year. This appears to reflect falling prices as well as weaker volumes. Note that Texas Instruments, an important US-based chip maker reports earnings today and Intel reports tomorrow. Separately, ASML, the Dutch-headquartered semiconductor equipment maker (largest in Europe), projected lower than expected Q1 sales. A fire at one of its suppliers appeared to account for nearly half miss.

The PBOC used a new facility to inject CNY257.5 bln (~$38 bln) into the banking system. The targeted medium-term lending facility to provide liquidity and incentives to lend to small businesses. This is not enough to make up for funds that expire rest of the week, and an additional provision is likely. There is increased talk of another cut in the required reserve ratio. The yield on China’s 10-year government bond fell for the first time in four sessions.

The US dollar has firmed against the Japanese yen, but it remains with a JPY109-handle for the fourth consecutive session. The technical indicators appear to favor another attempt at JPY110, perhaps encouraged by the better sense that the BOJ is lagging behind the other major central banks. The Australian dollar is holding the previous day’s low for the first time this week, finding support in the $0.7110-$0.7120 band. It may be capped in the $0.7150-$0.7160 area. The New Zealand dollar extended its recovery that began yesterday after testing $0.6700 with the help of a slightly stronger than expected Q4 CPI (1.9% unchanged from Q3 and above the 1.8% median expectation). However, the momentum may stall a little above $0.6800.

Europe

Ahead of tomorrow’s flash PMI for the eurozone and the ECB meeting, the focus remains on Brexit. The risks of a no-deal exit cannot be ruled out, and officials still need to prepare, but the odds seem to be receding, and the likelihood of a delay appears to be growing. This may be clearer over the next week. That said, the EC reportedly is pushing for Ireland to present its border plan in case the UK crashes out (without an agreement). As the market contemplates a delay, sterling has extended its gains against the euro. It is at its best level against the euro since mid-November (~GBP0.8750) and has retested last week’s high of $1.30.

Investors are yield hungry. Spain saw record demand (~47 bln euros) for the 10 bln euros of 10-year bonds it sold. Indications suggest it sold for 65 bp above midswaps, which is about five basis points tighter than initially anticipated. Recall last week, Italy’s sale of 2035 bonds was 3.6x oversubscribed after struggling to sell bonds last year and amid talk that there was no demand for Italian paper outside of the Eurosystem.

The euro has been confined to about a fifth of a cent above $1.1350 so far today. It is within yesterday’s range. Yesterday’s low was near $1.1335, and it was the first session that the single currency did not trade above $1.14 since mid-December. The intraday technicals suggest scope for it to stabilize in the North American session. Recall, that last year, the euro closed higher on ECB meeting days only once. Sellers appeared to be waiting for sterling to test the $1,30 level, last week’s highs against the dollar and managed to push it back to $1.2970. The intraday technical indicators suggest a high may be in place. Initial support is seen near $1.2950.

North America

There are two main US talking points today. The first is trade. The Financial Times report yesterday that a preparatory meeting ahead of next week’s talks were canceled weighed on sentiment yesterday. Economic Adviser Kudlow denied the story insofar as no meetings had been scheduled, there were none to cancel. However, he did acknowledge that China had offered to send to senior officials this week ahead of Vice Premier Liu He next week. Earlier signals that the talks were making progress and that there was some debate within the Trump Administration about tactics has fallen away. The new reports play up the difficulty over forced technology transfers, and US calls for getting rid of state subsidies, which it argues discriminates against foreign companies.

Late yesterday, the majority leader in the US Senate announced that two votes would be held tomorrow. The first vote is essentially on the President’s plan–funding for the wall and a temporary (three years) resolution for DACA. The second vote will be based on the Democrat plan to renew spending through February 8. There would be no extra wall funds, but that is what could be negotiated when the government re-opens. There is speculation that neither bill will be approved, but in the perverse world of politics, the votes are seen as 1) evidence of increasing concern about the impact of the prolonged closure and 2) create space for a new compromise.

Canada will report November retail sales today. The first decline since June is anticipated. Final domestic demand contracted in Q3, and it appears to be off to a poor start in Q4. A weak report will likely feed into expectations for the November monthly GDP report next week. October’s 0.3% pace, the fastest monthly growth since May is unlikely to have been sustained and was payback in part of a 0.1% contraction in September. The US dollar’s recovery against the Canadian dollar stalled yesterday near CAD1.3360, a little ahead of the 20-day moving average (~CAD1.3380). It was sold down to CAD1.3315 in Europe but appears to be finding a base. Separately, the Dollar Index is holding above its five-day moving average (~96.05) and has not closed below it since January 10.

Graphs and additional information on Swiss Franc by the snbchf team.

Full story here Are you the author?Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,EUR/CHF,FX Daily,newsletter,NZD,USD/CHF